Email

Email Print

Print

Steel Market - Overview

The Steel market is analyzed to be $1,746.35 billion in 2023 and is projected to reach $2,105 billion in 2030. The market is estimated to grow with a CAGR of 4.13% during 2024-2030. Steel is an alloy that is made up of iron ore or scrap steel and carbon. In general, steels have various unique properties including being non-corrosive, rust-resistant and heavier than other metals such as aluminum. Therefore, steel is extensively used in various end-use industry verticals, including the manufacturing various transportation and automobile components, medical equipment, metal surgical implants, structural components and more, which in turn is boosting its market growth. In recent years, the steel market has experienced fluctuations driven by several factors. One significant trend in the steel market is the impact of trade policies and tariffs. Trade tensions between major steel-producing nations, such as the United States, China, and the European Union, have led to shifts in supply chains and pricing dynamics. Tariffs imposed on steel imports have affected the competitiveness of domestic producers and influenced global trade patterns. Additionally, sustainability concerns and environmental regulations have influenced market dynamics. Increasing awareness of carbon emissions and the environmental footprint of steel production has led to a growing demand for greener steel products. This has prompted investments in cleaner production technologies such as electric arc furnaces and the development of recycled steel. Moreover, technological advancements and innovations in steel manufacturing processes have enhanced efficiency and product quality. As a result, the steel market is poised for sustained growth as global economic recovery accelerates, with innovations in technology and sustainability shaping future trends.

Steel Market Report Coverage

The report: “Steel Industry – Forecast (2024-2030)”, by IndustryARC covers an in-depth analysis of the following segments of the Steel Market Report.

By Type: Carbon Steel, (Low Carbon Steel, Medium Carbon Steel, High Carbon Steel), Stainless Steel (Austenitic Stainless Steels, Ferritic Stainless Steels, Martensitic Stainless Steels, Precipitation Hardening Grade Stainless Steels, Duplex Stainless Steels), Alloy Steel (Chromium Molybdenum Steel, Nickel-Chromium-Molybdenum Steel, Chromium Vanadium Steel, HSLA -Nickel-Chromium-Molybdenum Steel), Tool Steel (Water-hardening tool steels, Shock-resisting tool steels, Cold-work tool steels, Hot-work steels, High-speed tool steels, Others), Others

By Form: Bar, Rod, Tube, Pipe, Plate, Sheet, Structural, Others

By Application: Transportation (Road, Bridges, Barriers, Rail, Tracks, Rail Cars), Construction (Cool Metal (infrared reflecting) Roofing, Purlins, Beams, Pipe, Recyclable steel framing (studs), Desks/Furniture), Packaging (Canes, Bottles, Others), Water Projects (Levees/Dams/Locks), Energy (Renewable, Nuclear, Bio-fuels, Fossil, Electric Grid), Others

By Industry: Construction (Steel Skeletons, Concrete Walls, Pillars, Nails, Bolts, Screws, Others), Machinery (Bulldozers, Backhoe Leaders, Pipelayers, Others), Automotive and Transportation (Exhaust, Trim/Decorative, Engine, Chassis, Fasteners, Tubing For Fuel Lines), Kitchenware and Domestic Appliances (Small Household Appliances, Black Home Appliances, White Home Appliances), Electrical and Electronics (Motor Mount Brackets, Adapter Plates, Electronic Frames and Chassis, Brackets, Others), Healthcare (Orthopaedic Implants, Artificial Heart Valves, Bone Fixation, Catheters, Others), Energy (Scrubbers, Heat Exchangers, Others)

By Region: North America, South America, Europe, Asia-Pacific and Rest of the World

Key Takeaways

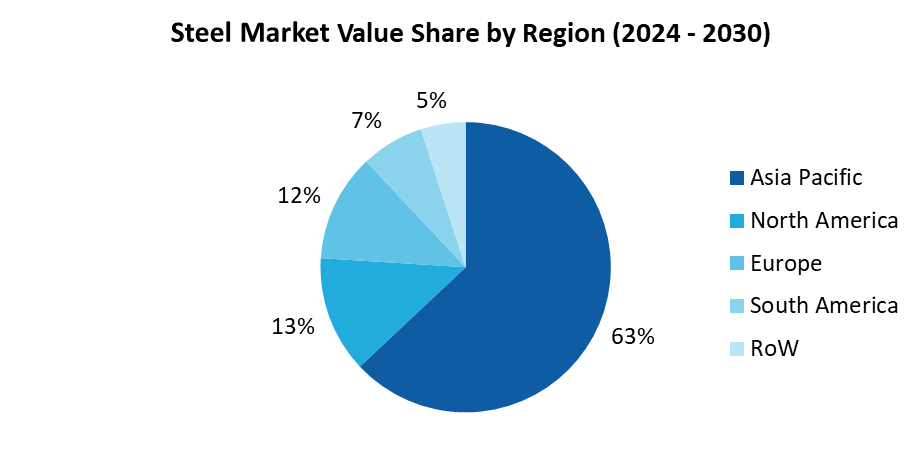

• The Asia-Pacific region, particularly China, has been a dominant force in the global steel market with a share of 63% in 2023, owing to China's rapid industrialization and urbanization have driven substantial demand for steel in the construction, infrastructure, and manufacturing sectors.

• Government infrastructure spending, particularly in major economies, plays a significant role in driving steel demand. Large-scale infrastructure projects, such as bridges, railways, and urban development initiatives, can create substantial demand for steel products.

• The automotive sector is a significant consumer of steel, particularly in the production of vehicles. Changes in consumer demand for automobiles, as well as shifts towards electric vehicles which may use different materials, can impact steel demand in this sector.

For More Details on This Report - Request for Sample

Steel Market Segment Analysis – By Type

In terms of type, the Steel Market is segmented into carbon steel, stainless steel, alloy steel, tool steel and others. In 2023, the Stainless-steel segment generated the greatest revenue of $361.94 billion and is projected to reach a revenue of $482.28 billion by 2030. Owing to the various benefits posed by stainless steel such as corrosion resistance, high and low temperature resistance, the ease of fabrication, strength, aesthetic appeal is one of the key factors for its adoption among various end-use industries, which in turn is boosting its market growth. The stainless-steel segment can be further classified as Austenitic stainless steels, Ferritic stainless steels, Martensitic stainless steels, Precipitation hardening grade stainless steel and Duplex stainless steels.

Steel Market Segment Analysis – By Form

By form, the steel market is segmented into bar, rod, tube, pipe, plate, sheet, structural and others. The bar segment accounted for the major market share in 2023, with a revenue of $554.58 billion, and is forecast to grow at a CAGR of 4.68% by 2030. The increasing demand for steel bar from various end-user industries such as building and construction, bridges, and many others, are driving the growth of the segment during the forecast period of 2024-2030.

Steel Market Segment Analysis – By Application

Steel Market is segmented by its application that includes transportation, construction, packaging, water projects, energy and others. The energy segment held the dominant market share, 31% of the whole market, in 2023, and is expected to maintain its dominance by 2030 with a CAGR of 4.69%. One of the major factors for the segment growth is the increasing awareness and focus towards renewable energy sources. Steel plays a crucial role in producing and distributing energy as well as improving energy efficiency. Renewable energy is further classified as Wind Towers and Foundation, Wind Turbines and Solar Parabolic Mirror Supports & Collectors.

Steel Market Segment Analysis – By Industry

The Steel finds its application across the industries such as construction, machinery, automotive and transportation, kitchenware and domestic appliance, electrical and electronics, healthcare, energy and others. Among them, the construction segment is the largest consumer of steel, as bearable structures can be manufactured easily at a low cost. The property of steel in its various forms and alloys makes it more flexible to cater the exclusive projects integrated with infrastructure. Moreover, the rapid industrialization and urbanization in various developing countries are fueling the segment growth in strengthening its dominant market position during the forecast period.

Steel Market Segment Analysis - By Geography/Country

The report comprises of the region wise study of the global market including North America, South America, Europe, Asia-Pacific and Rest of the World. Above all, Asia-Pacific region held the biggest share in 2023, up to 63% of the whole steel market owing to the rapidly expanding defense, machinery, automotive, and shipbuilding industries in the countries such as India, China, South Korea, and Japan. Foreign direct investment in energy and infrastructure is likely to provide opportunities for the market vendors. Coupled with favorable government regulations, growing infrastructure and construction activities in developing economies of the Asia-Pacific region are boosting the demand for the market.

Steel Market - Drivers

Growing Demand for Steel Across the Various Regions

Several factors have a significant impact on the overall development of the steel market. The major growth factor driving the Steel Market is the growing demand for steel across a variety of developing regions. For instance, Global crude steel production in January-November 2023 reached 1715.12 million metric tons, marking a marginal 0.5% year-on-year growth, per provisional data from the World Steel Association. November 2023 saw a production of 145.5 million metric tons, up by 3.3% from the previous year. China led the production with 952.14 million metric tons, followed by India and Japan, USA, Russia, South Korea, and Germany.

Construction and Infrastructure Development:

Construction activities, including residential, commercial, and infrastructure projects such as roads, bridges, and railways, are major drivers of steel demand. Urbanization and industrialization also contribute to the growth of the construction sector, thereby increasing the demand for steel products. For instance, as per Green Finance & Development Center, China Belt and Road Initiative (BRI) Investment Report 2023, engagement totalled about USD88.3 billion, with USD44.6 billion from investment and USD43.7 billion from construction contracts. Also, The US Department of Transportation allocates $3.2 billion in extra funding, alongside $4.3 billion from the Bipartisan Infrastructure Law for 2023. The Budget prioritizes $4.5 billion for the Capital Investment Grant program, aiming to bolster transit infrastructure for economic growth. As a result, the steel market is anticipated to thrive, propelled by heightened construction activities and the need for durable materials, reflecting a promising outlook for the industry.

Steel Market -Challenges

Environmental Regulations and Sustainability

The steel industry is facing mounting pressure to tackle environmental issues by cutting carbon emissions and enhancing sustainability efforts. Meeting stringent environmental regulations demands substantial investments in technology and infrastructure, presenting a formidable challenge for many companies. Despite the financial hurdles, embracing these changes can pave the way for a more sustainable and eco-friendly future for the industry.

Steel Market - Competitive Landscape

The companies referred in the study include Baosteel Co., Ltd., Posco Holding Inc, Nippon Steel Corporation, JFE Holdings, Tata Steel Limited, United States Steel Corporation, Anshan Iron and Steel Group Corporation, Hyundai Steel Co., Ltd., ThyssenKrupp AG, ArcelorMittal S.A., among others. Technology launches, acquisitions, and R&D activities are key strategies adopted by the key players in the Steel Market.

Steel Market - Recent Developments

November 2022, Tata Steel launched the fourth edition of MaterialNEXT, focusing on 'Materials to Wonder.' This open innovation event aims to gather ideas on emerging materials and their applications. The program spans five months across Idea Selection, Development, and Evaluation stages, fostering collaboration among scientists, researchers, and startups.

May 2022, Kobe Steel introduced "Kobenable Steel," Japan's pioneering low CO2 blast furnace steel, aiming to curtail emissions during ironmaking. Utilizing innovative CO2 Reduction Solution technology, it plans to roll out the product this fiscal year, marking a milestone in sustainable steel production.

In June 2023, Nippon Steel introduces ZEXEED™ Checkered Sheet, a new addition to its high corrosion resistant coated steel series

1. Steel Market - Overview

1.1 Definitions and Scope

2. Steel Market - Executive Summary

2.1 Key Trends by Type

2.2 Key Trends by Form

2.3 Key Trends by Application

2.4 Key Trends by Industry

2.5 Key Trends by Geography

3. Steel Market - Comparative Analysis

3.1 Company Benchmarking

3.2 Global Financial Analysis

3.3 Market Share Analysis

3.4 Patent Analysis

3.5 Pricing Analysis

4. Steel Market - Start-up Companies Scenario (Premium)

4.1 Key Start-up Company Analysis by

4.1.1 Investment

4.1.2 Revenue

4.1.3 Venture Capital and Funding Scenario

5. Steel Market – Market Entry Scenario Premium (Premium)

5.1 Regulatory Framework Overview

5.2 New Business and Ease of Doing Business Index

5.3 Case Studies of Successful Ventures

6. Steel Market - Forces

6.1 Market Drivers

6.2 Market Constraints/Challenges

6.3 Porter’s Five Force Model

6.3.1 Bargaining power of suppliers

6.3.2 Bargaining powers of customers

6.3.3 Threat of new entrants

6.3.4 Rivalry among existing players

6.3.5 Threat of substitutes

7. Steel Market – Strategic Analysis

7.1 Value Chain Analysis

7.2 Opportunities Analysis

7.3 Market Life Cycle

8. Steel Market– By Type (Market Size -$Million/Billion)

8.1 Carbon Steel

8.1.1 Low Carbon Steel

8.1.2 Medium Carbon Steel

8.1.3 High Carbon Steel

8.2 Stainless Steel

8.2.1 Austenitic Stainless Steel

8.2.2 Ferritic Stainless Steel

8.2.3 Martensitic Stainless Steel

8.2.4 Precipitation Hardening Grade Stainless Steel

8.2.5 Duplex Stainless Steel

8.3 Alloy Steel

8.3.1 Chromium Molybdenum Steel

8.3.2 Nickel Chromium Molybdenum Steel

8.3.3 Chromium Vanadium Steel

8.3.4 HSLA-Nickel-Chromium-molybdenum Steel

8.4 Tool Steel

8.4.1 Water Hardening Tool Steel

8.4.2 Shock-Resisting Tool Steel

8.4.3 Cold-Work Tool Steel

8.4.4 Hot Work Steel

8.4.5 High-Speed Tool Steel

8.4.6 Others

8.5 Others

9. Steel Market– By Form (Market Size -$Million/Billion)

9.1 Bar

9.2 Rod

9.3 Tube

9.4 Pipe

9.5 Plate

9.6 Sheet

9.7 Structural

9.8 Others

10. Steel Market– By Application (Market Size -$Million/Billion)

10.1 Transportation

10.1.1 Road

10.1.2 Bridges

10.1.3 Barriers

10.1.4 Rail

10.1.5 Tracks

10.1.6 Rail Cars

10.2 Construction

10.2.1 Cool Metal (infrared reflecting) Roofing

10.2.2 Purlins

10.2.3 Beams

10.2.4 Pipe

10.2.5 Recyclable steel framing (studs)

10.2.6 Desks/Furniture

10.3 Packaging

10.3.1 Canes

10.3.2 Bottles

10.3.3 Others

10.4 Water Projects

10.5 Energy

10.5.1 Renewable

10.5.2 Nuclear

10.5.3 Bio-fuels

10.5.4 Fossil

10.5.5 Electric Grid

10.6 Others

11. Steel Market – By Industry (Market Size -$Million/Billion)

11.1 Construction

11.1.1 Steel Skeletons

11.1.2 Concrete Walls

11.1.3 Pillars

11.1.4 Nails

11.1.5 Bolts

11.1.6 Screws

11.1.7 Others

11.2 Machinery

11.2.1 Bulldozers

11.2.2 Backhoe Leaders

11.2.3 Pipelayers

11.2.4 Others

11.3 Automotive and Transportation

11.3.1 Exhaust

11.3.2 Trim/Decorative

11.3.3 Engine

11.3.4 Chassis

11.3.5 Fasteners

11.3.6 Tubing For Fuel Lines

11.4 Kitchenware and Domestic Appliances

11.4.1 Small Household Appliances

11.4.2 Black Home Appliances

11.4.3 White Home Appliances

11.5 Electrical and Electronics

11.5.1 Motor Mount Brackets

11.5.2 Adapter Plates

11.5.3 Electronic Frames and Chassis

11.5.4 Brackets

11.5.5 Others

11.6 Healthcare

11.6.1 Orthopaedic Implants

11.6.2 Artificial Heart Valves

11.6.3 Bone Fixation

11.6.4 Catheters

11.6.5 Others

11.7 Energy

11.7.1 Scrubbers

11.7.2 Heat Exchangers

11.8 Others

12. Steel Market – By Geography (Market Size - $Million/$Billion)

12.1 North America

12.1.1 U.S.

12.1.2 Canada

12.1.3 Mexico

12.2 Europe

12.2.1 U.K

12.2.2 Germany

12.2.3 Italy

12.2.4 France

12.2.5 Netherlands

12.2.6 Belgium

12.2.7 Spain

12.2.8 Denmark

12.2.9 Rest of Europe

12.3 Asia-Pacific

12.3.1 China

12.3.2 Australia

12.3.3 Japan

12.3.4 South Korea

12.3.5 India

12.3.6 Taiwan

12.3.7 Malaysia

12.3.8 Rest of Asia-Pacific

12.4 South America

12.4.1 Brazil

12.4.2 Colombia

12.4.3 Argentina

12.4.4 Chile

12.4.5 Rest of South America

12.5 Rest of The World

12.5.1 Middle East

12.5.2 Africa

13. Steel Market - Entropy

14. Steel Market – Industry/Segment Competition Landscape (Premium)

14.1 Market Share Analysis

14.1.1 Global Market Share – Key Companies

14.1.2 Market Share by Region – Key Companies

14.1.3 Market Share by Countries – Key Companies

14.2 Competition Matrix

14.3 Best Practices for Companies

15. Steel Market – Key Company List by Country Premium (Premium)

16. Steel Market- Company Analysis

16.1 Baosteel Co., Ltd.

16.2 Posco Holding Inc

16.3 Nippon Steel Corporation

16.4 JFE Holdings

16.5 Tata Steel Limited

16.6 United States Steel Corporation

16.7 Anshan Iron and Steel Group Corporation

16.8 Hyundai Steel Co., Ltd.

16.9 ThyssenKrupp AG

16.10 ArcelorMittal S.A.

* "Financials would be provided to private companies on best-efforts basis." Connect with our experts to get customized reports that best suit your requirements. Our reports include global-level data, niche markets and competitive landscape.