Email

Email Print

Print

Industrial Turbocharger Market - Forecast(2025 - 2031)

Industrial Turbocharger Market Overview

The Industrial Turbocharger market size is estimated to reach $14.5 Billion by 2027, growing at a CAGR of 6.3% during the forecast period 2022-2027. The factors that impact the Industrial Turbocharger market include the growing development of vehicles with twin charging or multiple turbocharging systems, significant demand for gasoline/petrol powered turbocharge engines and so on. Since turbocharger is a kind of forced induction device or a centrifugal compressor, capable of utilizing wasted energy from exhaust gases within an internal combustion engine, they have started gaining wide popularity across varied industry verticals like automotive, power generation, oil & gas and so on. Due to being subjected to continuous vibrational, shock and high-temperature environments, turbocharged engines are prone to overheat, which in turn drives the need for incorporating front mount intercoolers to maintain a cooling temperature. Moreover, high R&D development towards electric or gasoline turbochargers, growing demand for industrial machinery minimal downtime, and significant adoption across marine applications have been catering to its market growth. Integration of turbocharged engines within locomotives, agricultural or farming equipment like tractors, harvesters and so on, along with increasing demand for fuel-efficient power engines for earth-moving applications are some of the major factors set to transform the Industrial Turbocharger industry outlook in the long run.

Industrial Turbocharger Report Coverage

The

“Industrial Turbocharger Market Report –

Forecast (2022-2027)” by IndustryARC, covers an in-depth analysis of the

following segments in the Industrial

Turbocharger Market.

Key Takeaways

- Gasoline/Petrol segment

is analyzed to grow with the highest CAGR in the global Industrial Turbocharger

market during the forecast period 2022-2027, owing to the growing emphasis of

automakers on improved vehicle fuel efficiency standards, rising demand

for petrol-powered turbocharged engines and so on.

- Automotive Industry is analyzed to witness the fastest growth in the global Industrial Turbocharger market during 2022-2027, attributed to government regulations on reducing CO2 vehicular emissions, high demand for automotive with fuel-efficient engines and so on.

- Europe Industrial Turbocharger market held the largest share in 2021, owing to high R&D activities related to electric turbochargers, government stringency over reducing vehicle emissions and so on.

- Governmental regulations or initiatives towards reducing vehicular emissions coupled with increasing demand for fuel-efficient vehicles alongside growing demand for mining equipment with lesser downtime, reliability as well as fuel efficiency benefits for maximized production is analyzed to significantly drive the market growth of the Industrial Turbocharger market during the forecast period 2022-2027.

Industrial Turbocharger Market Segment Analysis - by Fuel Type

Based on fuel type, the Gasoline/Petrol segment is analyzed

to witness the fastest growth with a CAGR of 7.5% in the global Industrial Turbocharger market during

the forecast period 2022-2027. Factors attributing to this market growth

include the growing deployment of petrol turbo engines in vehicles, the increased

emphasis of automakers on improving vehicle fuel efficiency standards and

so on. High R&D activities regarding gasoline or petrol industrial

turbochargers, growing consumer demand for gasoline-powered vehicles and so on

can also help in driving the market growth for centrifugal compressors driven

by gas turbines. In January 2021, Tata Motors announced about the launch of Altroz

iTurbo, equipped with a 1.2-liter three-cylinder turbocharged petrol engine, as

seen in its Nexon compact SUV models. The development of this turbocharged vehicle was

meant to boast an efficiency figure of 18.13kmpl, with

power figures detuned to 110PS@5,500rpm and 140Nm@1,500-5,500rpm, mated to a

5-speed manual gearbox. These factors are

set to influence the growth of the global

Gasoline/Petrol Industrial Turbocharger industry in the long run.

Industrial Turbocharger Market Segment Analysis - by End-use

Industry

Automotive

Industry is analyzed to grow with the

highest CAGR of 8.1% in the global Industrial Turbocharger market during

2022-2027, attributed to varied factors including government regulations on

reducing CO2 emissions from vehicles, growing demand for fuel-efficient engines

and so on. Turbocharging eventually gained wide popularity within

automotive industries due to the growing emphasis of automakers to provide better fuel economy and

performance standards, alongside enabling higher engine output with smaller

displacement engines as well as lesser cylinders. According

to the U.S. Department of Energy, about 34% of new light-duty vehicles produced were

already equipped with a turbocharger as in 2019. This highlighted the

significant growth towards the utilization of turbocharging technology within

vehicles, which in turn is positively impacting its market adoption. Moreover, the rapid

rise in R&D activities from global automakers like Toyota, Tata Motors, Renault

and so on, towards manufacturing SUVs with turbocharged engines, the growing integration of hybrid vehicles with twin charging or multiple turbocharging systems and so on can help in propelling

further market demands. In April 2022, Toyota revealed its plans the launch a flagship SUV, Land Cruiser LC300, equipped with a 3.3 liter

twin-turbo diesel engine in the Indian market by August 2022. Paired with a

10-speed automatic gearbox, these turbochargers will be capable of producing 305bhp and 700Nm of

torque, in order to reduce fuel consumption as well as vehicle emissions. These

factors will help in expanding the global Industrial Turbocharger market size for the automotive

industry in the coming time.

Industrial Turbocharger Market Segment Analysis - by

Geography

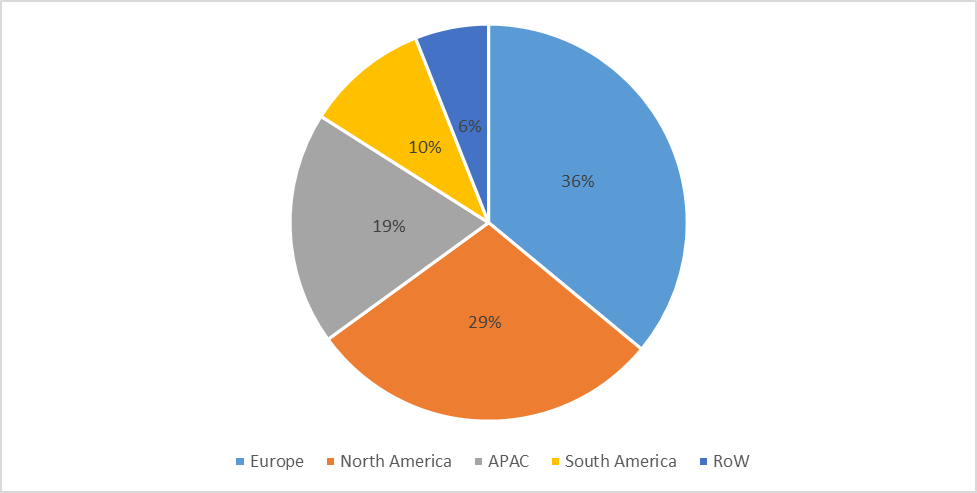

Europe dominated the global Industrial Turbocharger market with a share of 36% in 2021, attributed to stringent governmental regulations or mandates for reducing vehicle emissions, growing R&D activities related to electric turbochargers, and so on. According to the preliminary figures from Citepa, greenhouse gas (GHG) emissions except for LULUCF in France increased to 418 MtCO2eq in 2021, a rise of 6.4% after a decline of 9.6% in 2020. This rise was driven by higher GHG emissions within the transport sector (+11.5%, i.e. +13 MtCO2eq, including +12% for road transport), in manufacturing and construction (+7.2%, i.e. +5.2 MtCO2eq, including +21% for ferrous metallurgy), followed by energy sector (+7.4%, i.e. +3 MtCO2eq, including 10% for power generation), and agriculture (+5.5%, i.e. +3.9 MtCO2eq).

In June 2020, a German automotive giant, Mercedes-AMG revealed its plans for the development of a new generation electric turbocharger for its future models. In partnership with Garrett Motion, the company announced that the electric exhaust gas turbocharger had already reached its final stage of development, and was capable of resolving the low-peak performance of a small fast-charging turbocharger as well as high peak performance of a large turbocharger. This was a part of the company’s initiative towards supporting the electrification of its fleet vehicles while extending the electric turbocharge technology for passenger vehicles. Moreover, an upsurge in GHG emissions from the transportation sector, manufacturing, construction, power generation and so on, alongside rising in mining activities is set to transform the European Industrial Turbocharger industry outlook in the long run.

Industrial Turbocharger Market Drivers

Governmental Regulations or Initiatives towards Reducing Vehicular Emissions Coupled with Increasing Demand for Fuel-efficient Vehicles is Driving the Market Growth of Industrial Turbocharger:

Growing emphasis of automakers on developing fuel-efficient vehicles, increasing adoption of twin charging or multiple turbocharged engines and so on, in order to comply with governmental mandates have been attributed to the market growth. As automakers are constantly being challenged to meet stringent emission as well as fuel efficiency requirements, utilizing a turbocharged engine helps in offering improved fuel economy, lesser CO2 emissions and better performance, due to recycling wasted energy from the exhaust gas. The European government passed a regulation (EU)2019/631, effective from January 2020, which highlighted the new CO2 emission performance standards for new passenger cars & vans. Under this, EU fleet-wide CO2 emission targets applying for the years 2020, 2025 and 2030 were set, alongside offering incentives on the uptake of zero or low-emission vehicles. After the legislation became effective, European Commission revealed that the average CO2 emissions from new passenger cars registered in Europe faced a decline of 12% in 2020, compared to the previous year. Such factors can be considered vital in boosting the growth of the Industrial Turbocharger industry over time. In August 2020, Renault India announced about the launch of its compact SUV model, Duster equipped with a 1.3-liter turbocharged petrol engine. This model also had an ARAI-rated fuel efficiency of 16.5 kmpl for a manual transmission as well as 16.42 kmpl in the CVT version, making it a fuel-efficient vehicle. Moreover, high R&D activities related to automobiles equipped with petrol turbocharging petrol engines, along with a governmental emphasis on meeting CO2 emission targets for new passenger vars or vehicles can also drive the market forward.

Growing Demand for Mining Equipment with Lesser Downtime, Reliability and Fuel Efficient Benefits for Maximizing Production Output is Accelerating the Growth of Industrial Turbocharger Market:

Increasing demand for mining equipment with lesser downtime, reliability and reduced fuel consumption benefits while maximizing production output can be considered a major driver influencing the market growth of Industrial Turbochargers. This market growth is attributed to varied factors including increasing electricity demands, a rise in the number of mining projects and growing production of iron, coal and related minerals. According to Enerdata, global coal output expanded by 5.7% in 2021, compared to the pre-pandemic level during 2019. In addition, the total coal production in Europe increased by 11.9% in 2021, due to high electricity demands as well as steep gas prices, with a 17.7% rise in Germany, followed by a 6.9% and 15% increase in Poland and Turkey. This, in turn, highlighted the surge in demand for mining equipment like trucks, loaders, diggers and others, capable of ensuring optimized operational standards. In June 2021, Cummins had launched QSK95 95-litre engine specifically for mining, making it one of the most powerful engines developed for ultra-class trucks. These factors are set to help in the expansion of the global Industrial Turbocharger market size in the coming time.

Industrial Turbocharger Market Challenges

High Costs associated with Operation, Maintenance & Repair are Restraining the Growth of the Industrial Turbocharger Market:

High costs related to the operation, maintenance, repair or overhaul act as one of the major factors impeding the growth of the Industrial Turbocharger industry. Since a turbocharger comprises of casings, blades, rotors, bearings, gaskets, assemblies and related components, which can lead to wear and tear over time, due to continuous operation under high-temperature environments. On average, replacement costs for Mazda CX7 turbo range between $1,579 to $1,719, followed by labor costs of around $502 to $633 alongside replacement parts running between $1,077 and $1,719. Moreover, maintenance, repair & overhaul services require skilled professionals, alongside a pricing differentiation from OEM, aftermarket suppliers or third-party service providers, thus adding up the operational costs for the end users. These factors eventually contribute toward lesser adaptability from small-scale industries, thus creating an adverse impact on the market growth of industrial turbochargers.

Industrial Turbocharger Industry Outlook

Product launches,

acquisitions and R&D activities are key strategies adopted by players in

the Industrial Turbocharger Market. The top 10

companies in the Industrial Turbocharger market are:

- Honeywell International Inc.

- MAN Energy Solutions

- BorgWarner Inc.

- Mitsubishi Heavy Industries

- Cummins Inc.

- IHI Corporation

- Garett Motion Inc.

- ABB

- Eaton Corporation

- Precision Turbo Engine

Recent Developments

- In August 2020, Cummins Turbo Technologies launched its 7th generation 400 series Variable Geometry Turbocharger (VGT), in order to help engine manufacturers meet emission standards and offer best-in-class fuel economy. This development was focused on the on-highway heavy-duty market with engines having a range of 10 to 15 liters, alongside a variety of applications like transit buses, fire trucks and so on.

- In January 2020, Mitsubishi Heavy Industries (MHI) and Imperial jointly launched a research center, focused on improving turbocharger designs as well as developing cleaner engines. Development of the MHIET-imperial Future Boosting Innovation Centre was intended to carry out detailed research on state-of-the-art turbochargers as well as exhaust energy technologies, capable of improving engine performance and operation while enabling low carbon engine technology.

- In February 2019, MAN Energy Solutions launched the Axial TCT series, as a part of its addition to the TCT turbocharger series, optimized for Tier-III operation. These models offered suitability for both conventional as well as dual-fuelled engines within marine and power applications, ranging between 6MW to 24MW output per turbocharger.

Relevant Report Titles:

Report Code: AM 38811

Report Code: ATR 0101

Report Code: CMR 0291

For more Electronics Market reports, please click here