Email

Email Print

Print

Smart Infusion Pumps Market- By Product Type, By Application , By End User and By Geography - Opportunity Analysis & Industry Forecast, 2024-2030

Smart Infusion Pumps Market Overview

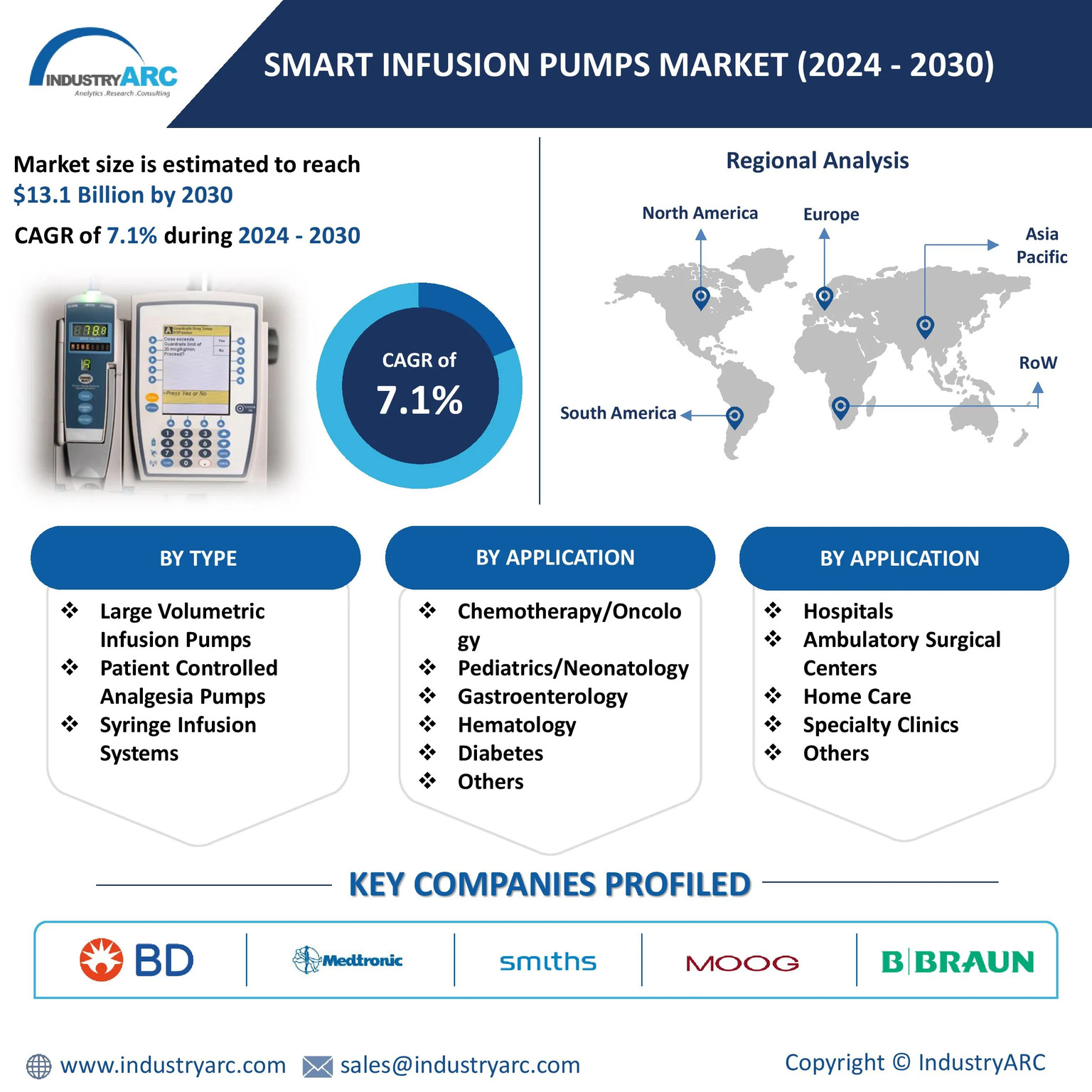

Smart Infusion Pumps Market size is expected to be valued at $13.1 billion by the end of the year 2030 and the Smart Infusion Pumps industry is set to grow at a CAGR of 7.1% during the forecast period from 2024-2030. Smart infusion pumps are advanced medical devices that deliver precise amounts of fluids or medications into a patient's body at a controlled rate. Unlike traditional pumps, these devices incorporate intelligent features to enhance patient safety and medication accuracy. These are revolutionizing the healthcare industry by offering advanced features and improved patient safety. These devices are equipped with intelligent capabilities that enable precise medication delivery, real-time monitoring, and enhanced patient management. The rise of chronic diseases like diabetes and cancer drives the market. An aging population also needs more infusion therapy and user-friendly smart pumps are ideal for both hospitals and home care.

Software-defined infusion management has become a breakthrough in smart infusion pumps, allowing customizable, real-time adjustments to infusion therapy. Advanced software systems enable healthcare providers to set precise infusion parameters, detect errors and manage medications with greater accuracy. Another trend in the market is the growing preference for portable and wearable infusion pumps. The demand for portable and wearable infusion pumps is increasing as patients seek more flexibility and independence during treatment. These devices allow for continuous, convenient infusion therapy without being tethered to stationary equipment, making it ideal for home healthcare and outpatient services. In May 2024, Serina Therapeutics partnered with Enable Injections to advance SER-252 (POZ-apomorphine), Serina’s lead treatment candidate for advanced Parkinson’s disease, in combination with the enFuse wearable delivery system. EnFuse is designed to allow patients to self-administer SER-252 subcutaneously. With enFuse, patients can self-administer SER-252 in the convenience of their home with wearable technology and with a rapid treatment time.

Market Snapshot:

Report Coverage

The report: “Smart Infusion Pumps Market – Forecast (2024-2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the Smart Infusion Pumps.

| Attribute | Segment |

|---|---|

|

By Type |

|

|

By Application |

|

|

By Application |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic significantly impacted the smart infusion pump market. Increased hospitalizations and the need for precise medication delivery led to a surge in demand for these devices. However, supply chain disruptions and manufacturing challenges caused by the pandemic hindered production and distribution leading to temporary shortages and price fluctuations.

- The Russia-Ukraine war indirectly impacted the smart infusion pump market primarily through supply chain disruptions and increased costs of raw materials. Both Russia and Ukraine are significant suppliers of critical components used in the manufacturing of these devices. The conflict led to disruptions in the supply of these components.

Key Takeaways

Large Volume Parenteral (LVP) pumps are the Largest Segment

Large Volume Parenteral (LVP) pumps represent the largest product segment within the smart infusion pumps market. These pumps are designed to deliver fluids, medications, blood and blood products in larger volumes, making them essential for various medical procedures. They are used in a wide range of medical settings including hospitals, clinics and ambulatory care centers. LVP pumps incorporate advanced features like drug libraries, safety alerts and connectivity. In April 2024, Baxter announced that the FDA granted 510(k) clearance for its Novum IQ large-volume infusion pump (LVP) with Dose IQ safety software. The system’s Dose IQ safety software features a web-based, customizable drug library and dose error reduction system. It supports clinicians and hospitals by ensuring that pumps remain up-to-date with the latest facility-specific drug and dosage parameters and information through centralized access to drug library files.

Chemotherapy/Oncology is the Largest Application

Chemotherapy/Oncology is the largest application of smart infusion pumps. Chemotherapy drugs often require extremely precise dosing, which smart pumps excel at. These drugs can be highly toxic so accurate administration is crucial to prevent adverse effects. Chemotherapy regimens are often complex, involving multiple drugs and infusion rates, making smart pumps invaluable for managing treatment plans. The rising incidence of cancer has led to a higher demand for chemotherapy, driving the need for smart infusion pumps. According to the World Health Organisation, globally over 35 million new cancer cases are predicted in 2050, an increase from the estimated 20 million in 2022. With millions of new cancer cases diagnosed annually the demand for effective treatment options continues to escalate. A report by Cancer Research UK states that by 2040 there are projected to be 500,000 new cancer cases diagnosed each year in the UK attributed to a growing and ageing population.

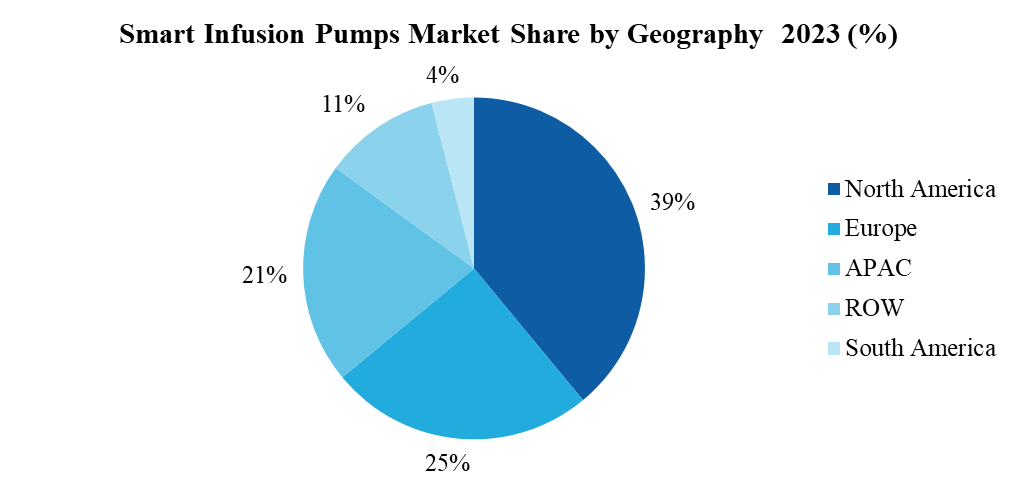

North America Dominates the Market

North America held the largest share of around 40% in the Smart Infusion Pumps market in the year 2023. North America has been at the forefront of adopting medical technology including smart infusion pumps, leading to higher penetration rates. The region has a significant healthcare expenditure allowing for investments in advanced medical technologies. According to the Centers for Medicare & Medicaid Services (CMS), the U.S. spent approximately $4.3 trillion on healthcare, representing about 18.3% of the country's GDP in 2023and anticipates reaching approximately $4.5 trillion in 2024. This high level of spending is a testament to the nation's commitment to advanced medical technologies Along with that, substantial investments in research and development in the healthcare sector foster innovation in infusion pump technology. Several leading manufacturers of smart infusion pumps are headquartered in North America contributing to the region's market dominance.

Growing Geriatric Population to Drive Market Growth

The geriatric population is predicted to reach 16% by 2050. US, Canada, Europe, India and China are some countries where the geriatric population's growth is anticipated to witness rapid surges during the forecast period. For instance, with the decadal growth rate of the elderly population of India currently estimated to be at 41%, and the percentage of elderly population in the country projected to double to over 20% of total population by 2050. As per the United Nations Population Fund, India (UNFPA) 2023 India Ageing Report, by 2046 it is likely that elderly population will have surpassed the population of children (aged 0 to 15 years) in the country. The risk of diseases and disorders such as diabetes and cancer increase with age. Thus, the increase in the geriatric population is set to drive the smart infusion pumps market.

Product Recalls to Hamper the Market

Product recalls significantly impact the smart infusion pump market. Recalls can occur due to various reasons including manufacturing defects, software glitches or safety concerns. These recalls can damage the reputation of manufacturers, lead to financial losses and erode consumer trust. Additionally, recalls can disrupt supply chains causing temporary shortages and delaying patient access to critical medications. In January 2024, Fresenius Kabi earned a Class I rating from the FDA for a recall of the Ivenix medication delivery technology. The latest recall concerns the large-volume pump component of the Ivenix infusion system, which also comprises a pump management software platform and a digital clinician dashboard.

For more details on this report - Request for Sample

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

7.1% |

|

Market Size in 2030 |

$13.1 billion |

|

Segments Covered |

By Product Type, By Application, By End User and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

For more Lifesciences and Healthcare Market reports, please click here

The Smart Infusion Pumps Market is projected to grow at 7.1% CAGR during the forecast period 2024-2030.

The Smart Infusion Pumps Market size is estimated to be $8.7 billion in 2023 and is projected to reach $13.1 billion by 2030

The leading players in the Smart Infusion Pumps Market are BD, Medtronic Plc, Smiths Medical, MOOG Inc., B. Braun Melsungen AG and Others.

The demand for portable and wearable infusion pumps and software-defined infusion management are some of the major Smart Infusion Pumps Market trends in the industry which will create growth opportunities for the market during the forecast period.

Rising demand for precision in medication delivery, increasing incidence of chronic diseases and demand for continuous infusion therapy due to geriatric population are the driving factors of the Smart Infusion Pumps market.