Email

Email Print

Print

Semiconductor Market Overview:

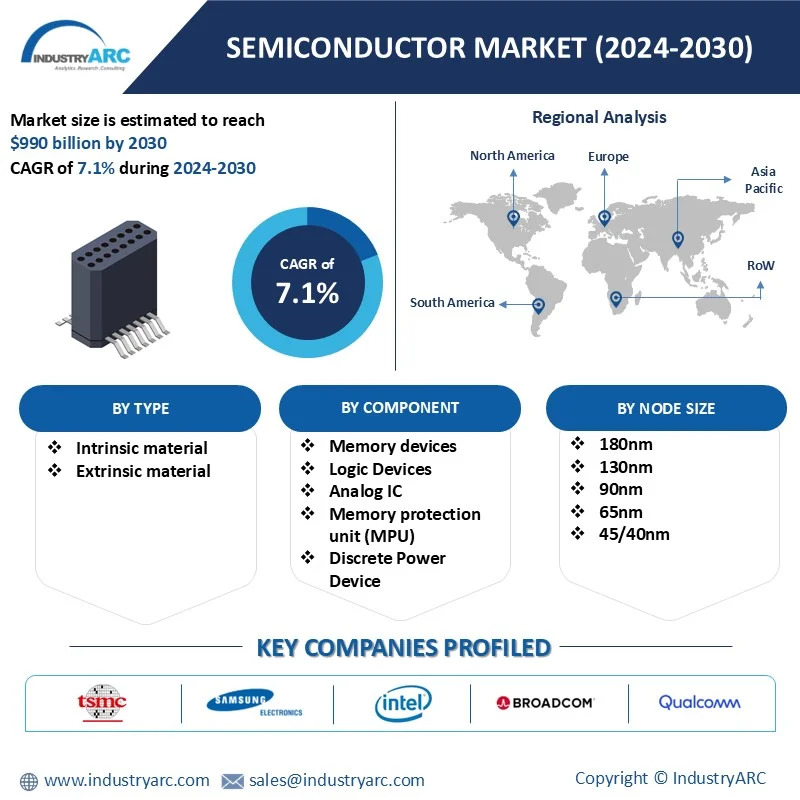

The Semiconductor Market size is estimated to reach $990 Billion by 2030, growing at a CAGR of 7.1% during the forecast period 2024-2030. The market is projected to grow significantly, driven by the surging demand for advanced electronic devices, 5G infrastructure, and the proliferation of the Internet of Things (IoT). Major trends include the rapid development of artificial intelligence (AI) chips, essential for machine learning, data analytics, and autonomous systems. The automotive sector is another key driver, with semiconductors playing a pivotal role in electric vehicles (EVs), advanced driver-assistance systems (ADAS), and vehicle-to-everything (V2X) communication.

The geopolitical landscape continues to shape the market. Countries are ramping up investments in domestic semiconductor manufacturing to reduce reliance on global supply chains, with initiatives like the U.S. CHIPS Act and China’s Made in China 2025 policy. Another significant development is the transition to smaller node technologies (e.g., 3nm and beyond), which improve chip performance and power efficiency. Additionally, heterogeneous integration and chiplet architectures are gaining traction, allowing greater functionality on a single chip. Sustainability is also influencing the sector, with companies focusing on energy-efficient designs and greener production methods. Furthermore, mergers and acquisitions remain prominent as firms seek to expand capabilities and market presence.

In summary, the semiconductor market is evolving rapidly, driven by technological innovation, geopolitical shifts, and sustainability efforts, positioning itself as a critical enabler of global digital transformation.

Market Snapshot:

Semiconductor Market - Report Coverage:

The “Semiconductor Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Semiconductor Market.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

COVID-19 / Ukraine Crisis - Impact Analysis:

• The COVID-19 pandemic disrupted semiconductor supply chains, leading to global shortages and production delays. Increased demand for electronic devices, remote work technologies, and medical equipment further strained the market. However, the crisis accelerated digital transformation, prompting significant investments in semiconductor manufacturing capacity and fostering innovation to address future supply chain resilience.

• The Ukrainian crisis disrupted global semiconductor supply chains, particularly affecting the availability of critical raw materials like neon and palladium, essential for chip manufacturing. Escalating geopolitical tensions led to increased costs and production delays, prompting companies to diversify sourcing, invest in localized manufacturing, and prioritize supply chain resilience to mitigate risks.

Key Takeaways:

Middle East and Africa Region is Projected as Fastest Growing Region

Middle East and Africa is projected as the fastest growing region in Semiconductor Market with CAGR of 10.8% during the forecast period 2024-2030. Countries like Saudi Arabia, the UAE, and South Africa are rapidly integrating advanced technologies such as IoT, AI, and 5G, fueling demand for semiconductors. The region’s governments are prioritizing digital transformation initiatives, including smart city projects and industrial automation, which require advanced semiconductor components. Additionally, the rise of data centers and renewable energy systems is boosting demand for power management and memory chips. MEA is also witnessing growing interest in localized semiconductor manufacturing, supported by foreign direct investments and partnerships with global technology firms. This growth trajectory is further strengthened by the region's strategic focus on diversifying its economy and becoming a global tech hub. Despite challenges such as limited infrastructure and skilled labor, the region's rapid technological advancement and supportive policies position it as a high-potential market, contributing to its status as the fastest-growing in the semiconductor industry.

Extrinsic material Segment to Register the Fastest Growth

In the semiconductor market, the extrinsic materials segment is currently experiencing the fastest growth. Extrinsic materials are specially doped to enhance the electrical properties of semiconductors, making them essential for the manufacturing of high-performance electronic devices such as processors, memory chips, and power modules. These materials include various alloys and dopants like phosphorus, boron, and arsenic, which are added to semiconductors to control their conductivity and functionality. The rapid growth of extrinsic materials is largely driven by the increasing demand for advanced technologies, including 5G, electric vehicles, AI, and IoT. These technologies require semiconductors with highly tailored properties, and extrinsic materials enable the customization of these properties to meet the specific needs of high-speed, energy-efficient applications. Additionally, the rise of new manufacturing processes, such as 3D chip stacking and advanced node scaling, further fuels the demand for extrinsic materials, positioning this segment as a key growth driver in the semiconductor market.

Memory Devices are Leading the Market

In the semiconductor market, the memory devices segment holds the largest market share. This segment includes components such as DRAM (Dynamic Random-Access Memory), NAND flash, and SRAM (Static RAM), which are essential for data storage and processing in a wide range of electronic devices, including smartphones, computers, servers, and consumer electronics. The demand for memory devices is driven by the growing need for high-speed data processing and storage solutions across industries. As data generation continues to increase exponentially, the need for robust memory solutions to store and process this information efficiently is critical. Innovations in cloud computing, big data analytics, and AI applications further fuel the demand for advanced memory devices with higher capacity and faster access speeds. Additionally, the expansion of mobile and gaming industries, along with the adoption of next-gen technologies like 5G, is contributing to the sustained dominance of memory devices in the semiconductor market, making it a key driver of market growth.

Advancements in Artificial Intelligence and Machine Learning

The integration of artificial intelligence (AI) and machine learning (ML) in various sectors is a significant driver of the semiconductor market. These technologies demand high-performance computing power, which relies on specialized chips like GPUs, TPUs, and AI accelerators. AI applications in industries such as healthcare, automotive, and financial services require processing large volumes of data in real-time, pushing the demand for semiconductors with advanced capabilities. For example, AI-driven diagnostics in healthcare or autonomous vehicle systems require seamless data processing, enhancing the demand for cutting-edge chips. Additionally, the rapid expansion of AI-based personal assistants, chatbots, and recommendation systems further fuels the market. Companies like NVIDIA and Intel have capitalized on this trend, continuously innovating to meet the needs of AI workloads. The growth of AI and ML applications is expected to continue, making this a critical factor in driving semiconductor market growth over the coming years.

Global Supply Chain Disruptions is a Major Challenge

One of the most pressing challenges facing the semiconductor market is global supply chain disruptions. These disruptions stem from a combination of geopolitical tensions, natural disasters, and the COVID-19 pandemic, which highlighted the industry's vulnerability to unexpected events. The semiconductor supply chain is highly complex and geographically dispersed, with raw materials sourced from one region, components manufactured in another, and final assembly occurring elsewhere. For instance, reliance on key regions like Taiwan, South Korea, and China for semiconductor manufacturing creates a bottleneck. Any disruptions in these regions—such as chip shortages, port delays, or export restrictions—can significantly impact production timelines and revenue. Furthermore, the lack of sufficient inventory buffers exacerbates the problem, leaving industries like automotive and consumer electronics struggling to meet demand. While companies and governments are investing in localizing production to reduce reliance on specific regions, establishing new manufacturing facilities is time-consuming and costly. Addressing supply chain vulnerabilities remains a critical challenge to ensuring the long-term stability of the semiconductor market.

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Semiconductor Market. The top 10 companies in this industry are listed below:

1. Qualcomm Technologies, Inc.

2. Broadcom, Inc.

3. Intel Corporation

4. Samsung Electronics

5. Taiwan Semiconductors

6. NXP Semiconductors

7. SK Hynix

8. Texas Instruments

9. Micron Technology

10. Maxim Integrated Products, Inc.

Scope of the Report:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For more Electronics Market reports, please click here

1. Semiconductor Market - Overview

1.1. Definitions and Scope

2. Semiconductor Market - Executive Summary

3. Semiconductor Market - Comparative Analysis

3.1. Company Benchmarking - Key Companies

3.2. Financial Analysis - Key Companies

3.3. Market Share Analysis - Key Companies

3.4. Patent Analysis - Major Companies

3.5. Pricing Analysis (ASPs will be provided)

4. Semiconductor Market - Start-up Companies Scenario

4.1. Key Start-up Company Analysis:

4.1.1. Investment

4.1.2. Revenue

4.1.3. Product portfolio

4.1.4. Venture Capital and Funding Scenario

5. Semiconductor Market – Industry Market Entry Scenario Premium

5.1. Regulatory Framework Overview

5.2. New Business and Ease of Doing Business Index

5.3. Successful Venture Profiles

5.4. Customer Analysis – Major companies

5.5. Customer Landscape Analysis

5.5.1. Adoption Rate

5.5.2. Purchasing Criteria

6. Semiconductor Market - Forces

6.1. Market Drivers

6.2. Market Constraints

6.3. Porter's Five Force Model

6.3.1. Bargaining Power of Suppliers

6.3.2. Bargaining Powers of Customers

6.3.3. Threat of New Entrants

6.3.4. Rivalry Among Existing Players

6.3.5. Threat of Substitutes

7. Semiconductor Market – Strategic Analysis

7.1. Value Chain Analysis

7.2. Opportunities Analysis

7.3. Product Life Cycle/Market Life Cycle

7.4. Distributor Analysis – Major Companies

8. Semiconductor Market – By Type (Market Size – $Million/$Billion)

8.1. Intrinsic material

8.2. Extrinsic material

8.2.1. N-Type

8.2.2. P-Type

9. Semiconductor Market– By Component (Market Size – $Million/$Billion)

9.1. Memory devices

9.2. Logic Devices

9.3. Analog IC

9.4. Memory protection unit (MPU)

9.5. Discrete Power Device

9.6. Multipoint control unit (MCU)

9.7. Sensors

9.8. Others

10. Semiconductor Market– By Node Size (Market Size – $Million/$Billion)

10.1. 180nm

10.2. 130nm

10.3. 90nm

10.4. 65nm

10.5. 45/40nm

10.6. 32/28nm

10.7. 22/20nm

10.8. 16/14nm

10.9. 10/7nm

10.10 .7/5nm

10.11 .5nm

11. Semiconductor Market– By Material Type (Market Size – $Million/$Billion)

11.1. Silicon

11.2. Germanium

11.3. Gallium arsenide

11.4. Silicon carbide

11.5. Gallium Nitride

11.6. Others

12. Semiconductor Market– By Application (Market Size – $Million/$Billion)

12.1. Networking and Communication

12.2. Data Processing

12.3. Consumer Electronics

12.4. Power Generation

12.5. Electronic Components

12.5.1. Printed Circuit Board (PCB)

12.5.2. Semiconductor Packaging and Assembly

12.5.3. Power Electronics Packaging and Assembly

12.6. Others

13. Semiconductor Market– By End-user (Market Size – $Million/$Billion)

13.1. Telecommunication

13.2. Energy

13.2.1. Oil & Gas

13.2.2. Wind Energy

13.2.3. Solar Energy

13.2.4. Others

13.3. Electrical and Electronics

13.4. Medical and Healthcare

13.5. Automotive

13.6. Defence & Aerospace

13.7. Others

14. Semiconductor Market – by Geography (Market Size – $Million/$Billion)

14.1. North America

14.1.1. U.S

14.1.2. Canada

14.1.3. Mexico

14.2. Europe

14.2.1. Germany

14.2.2. France

14.2.3. UK

14.2.4. Italy

14.2.5. Spain

14.2.6. Russia

14.2.7. Netherlands

14.2.8. Rest of Europe

14.3. Asia-Pacific

14.3.1. China

14.3.2. Japan

14.3.3. South Korea

14.3.4. India

14.3.5. Australia

14.3.6. Indonesia

14.3.7. Malaysia

14.3.8. Rest of Asia-Pacific

14.4. South America

14.4.1. Brazil

14.4.2. Argentina

14.4.3. Chile

14.4.4. Colombia

14.4.5. Rest of South America

14.5. Rest of The World

14.5.1. Middle East

14.5.2. Africa

15. Semiconductor Market – Entropy

15.1. New product launches

15.2. M&A's, collaborations, JVs and partnerships

16. Semiconductor Market – Industry/Segment Competition Landscape

16.1. Market Share at Global Level - Major companies

16.2. Market Share by Key Region - Major companies

16.3. Market Share by Key Country - Major companies

17. Semiconductor Market – Key Company List by Country Premium

18. Semiconductor Market – Company Analysis

18.1. Qualcomm Technologies, Inc.

18.2. Broadcom, Inc.

18.3. Intel Corporation

18.4. Samsung Electronics

18.5. Taiwan Semiconductors

18.6. NXP Semiconductors

18.7. SK Hynix

18.8. Texas Instruments

18.9. Micron Technology

18.10 . Maxim Integrated Products, Inc.

List of Tables

Table1: Semiconductor Market Overview 2023-2030

Table2: Semiconductor Market Leader Analysis 2023-2030 (US$)

Table3: Semiconductor Market Product Analysis 2023-2030 (US$)

Table4: Semiconductor Market End User Analysis 2023-2030 (US$)

Table5: Semiconductor Market Patent Analysis 2013-2023* (US$)

Table6: Semiconductor Market Financial Analysis 2023-2030 (US$)

Table7: Semiconductor Market Driver Analysis 2023-2030 (US$)

Table8: Semiconductor Market Challenges Analysis 2023-2030 (US$)

Table9: Semiconductor Market Constraint Analysis 2023-2030 (US$)

Table10: Semiconductor Market Supplier Bargaining Power Analysis 2023-2030 (US$)

Table11: Semiconductor Market Buyer Bargaining Power Analysis 2023-2030 (US$)

Table12: Semiconductor Market Threat of Substitutes Analysis 2023-2030 (US$)

Table13: Semiconductor Market Threat of New Entrants Analysis 2023-2030 (US$)

Table14: Semiconductor Market Degree of Competition Analysis 2023-2030 (US$)

Table15: Semiconductor Market Value Chain Analysis 2023-2030 (US$)

Table16: Semiconductor Market Pricing Analysis 2023-2030 (US$)

Table17: Semiconductor Market Opportunities Analysis 2023-2030 (US$)

Table18: Semiconductor Market Product Life Cycle Analysis 2023-2030 (US$)

Table19: Semiconductor Market Supplier Analysis 2023-2030 (US$)

Table20: Semiconductor Market Distributor Analysis 2023-2030 (US$)

Table21: Semiconductor Market Trend Analysis 2023-2030 (US$)

Table22: Semiconductor Market Size 2023 (US$)

Table23: Semiconductor Market Forecast Analysis 2023-2030 (US$)

Table24: Semiconductor Market Sales Forecast Analysis 2023-2030 (Units)

Table25: Semiconductor Market, Revenue & Volume, By Material Types, 2023-2030 ($)

Table26: Semiconductor Market By Material Types, Revenue & Volume, By Germanium, 2023-2030 ($)

Table27: Semiconductor Market By Material Types, Revenue & Volume, By Silicon, 2023-2030 ($)

Table28: Semiconductor Market By Material Types, Revenue & Volume, By Gallium Arsenide, 2023-2030 ($)

Table29: Semiconductor Market By Material Types, Revenue & Volume, By Silicon Carbide, 2023-2030 ($)

Table30: Semiconductor Market By Material Types, Revenue & Volume, By Gallium Nitride, 2023-2030 ($)

Table31: Semiconductor Market, Revenue & Volume, By Components, 2023-2030 ($)

Table32: Semiconductor Market By Components, Revenue & Volume, By Processors, 2023-2030 ($)

Table33: Semiconductor Market By Components, Revenue & Volume, By Analog ICS, 2023-2030 ($)

Table34: Semiconductor Market By Components, Revenue & Volume, By Sensors, 2023-2030 ($)

Table35: Semiconductor Market By Components, Revenue & Volume, By Memory devices, 2023-2030 ($)

Table36: Semiconductor Market By Components, Revenue & Volume, By Lighting devices, 2023-2030 ($)

Table37: Semiconductor Market, Revenue & Volume, By Process, 2023-2030 ($)

Table38: Semiconductor Market By Process, Revenue & Volume, By Wafer Production, 2023-2030 ($)

Table39: Semiconductor Market By Process, Revenue & Volume, By Wafer Fabrication, 2023-2030 ($)

Table40: Semiconductor Market By Process, Revenue & Volume, By Thermal Oxidation/ Deposition, 2023-2030 ($)

Table41: Semiconductor Market By Process, Revenue & Volume, By Masking, 2023-2030 ($)

Table42: Semiconductor Market, Revenue & Volume, By End Users, 2023-2030 ($)

Table43: Semiconductor Market By End Users, Revenue & Volume, By Telecommunication, 2023-2030 ($)

Table44: Semiconductor Market By End Users, Revenue & Volume, By Energy, 2023-2030 ($)

Table45: Semiconductor Market By End Users, Revenue & Volume, By Automotive, 2023-2030 ($)

Table46: Semiconductor Market By End Users, Revenue & Volume, By Computing, 2023-2030 ($)

Table47: Semiconductor Market By End Users, Revenue & Volume, By Consumer electronics, 2023-2030 ($)

Table48: North America Semiconductor Market, Revenue & Volume, By Material Types, 2023-2030 ($)

Table49: North America Semiconductor Market, Revenue & Volume, By Components, 2023-2030 ($)

Table50: North America Semiconductor Market, Revenue & Volume, By Process, 2023-2030 ($)

Table51: North America Semiconductor Market, Revenue & Volume, By End Users, 2023-2030 ($)

Table52: South america Semiconductor Market, Revenue & Volume, By Material Types, 2023-2030 ($)

Table53: South america Semiconductor Market, Revenue & Volume, By Components, 2023-2030 ($)

Table54: South america Semiconductor Market, Revenue & Volume, By Process, 2023-2030 ($)

Table55: South america Semiconductor Market, Revenue & Volume, By End Users, 2023-2030 ($)

Table56: Europe Semiconductor Market, Revenue & Volume, By Material Types, 2023-2030 ($)

Table57: Europe Semiconductor Market, Revenue & Volume, By Components, 2023-2030 ($)

Table58: Europe Semiconductor Market, Revenue & Volume, By Process, 2023-2030 ($)

Table59: Europe Semiconductor Market, Revenue & Volume, By End Users, 2023-2030 ($)

Table60: APAC Semiconductor Market, Revenue & Volume, By Material Types, 2023-2030 ($)

Table61: APAC Semiconductor Market, Revenue & Volume, By Components, 2023-2030 ($)

Table62: APAC Semiconductor Market, Revenue & Volume, By Process, 2023-2030 ($)

Table63: APAC Semiconductor Market, Revenue & Volume, By End Users, 2023-2030 ($)

Table64: Middle East & Africa Semiconductor Market, Revenue & Volume, By Material Types, 2023-2030 ($)

Table65: Middle East & Africa Semiconductor Market, Revenue & Volume, By Components, 2023-2030 ($)

Table66: Middle East & Africa Semiconductor Market, Revenue & Volume, By Process, 2023-2030 ($)

Table67: Middle East & Africa Semiconductor Market, Revenue & Volume, By End Users, 2023-2030 ($)

Table68: Russia Semiconductor Market, Revenue & Volume, By Material Types, 2023-2030 ($)

Table69: Russia Semiconductor Market, Revenue & Volume, By Components, 2023-2030 ($)

Table70: Russia Semiconductor Market, Revenue & Volume, By Process, 2023-2030 ($)

Table71: Russia Semiconductor Market, Revenue & Volume, By End Users, 2023-2030 ($)

Table72: Israel Semiconductor Market, Revenue & Volume, By Material Types, 2023-2030 ($)

Table73: Israel Semiconductor Market, Revenue & Volume, By Components, 2023-2030 ($)

Table74: Israel Semiconductor Market, Revenue & Volume, By Process, 2023-2030 ($)

Table75: Israel Semiconductor Market, Revenue & Volume, By End Users, 2023-2030 ($)

Table76: Top Companies 2023 (US$) Semiconductor Market, Revenue & Volume

Table77: Product Launch 2023-2030 Semiconductor Market, Revenue & Volume

Table78: Mergers & Acquistions 2023-2030 Semiconductor Market, Revenue & Volume

List of Figures

Figure 1: Overview of Semiconductor Market 2023-2030

Figure 2: Market Share Analysis for Semiconductor Market 2023 (US$)

Figure 3: Product Comparison in Semiconductor Market 2023-2030 (US$)

Figure 4: End User Profile for Semiconductor Market 2023-2030 (US$)

Figure 5: Patent Application and Grant in Semiconductor Market 2013-2023* (US$)

Figure 6: Top 5 Companies Financial Analysis in Semiconductor Market 2023-2030 (US$)

Figure 7: Market Entry Strategy in Semiconductor Market 2023-2030

Figure 8: Ecosystem Analysis in Semiconductor Market 2023

Figure 9: Average Selling Price in Semiconductor Market 2023-2030

Figure 10: Top Opportunites in Semiconductor Market 2023-2030

Figure 11: Market Life Cycle Analysis in Semiconductor Market

Figure 12: GlobalBy Material Types Semiconductor Market Revenue, 2023-2030 ($)

Figure 13: GlobalBy Components Semiconductor Market Revenue, 2023-2030 ($)

Figure 14: GlobalBy Process Semiconductor Market Revenue, 2023-2030 ($)

Figure 15: GlobalBy End Users Semiconductor Market Revenue, 2023-2030 ($)

Figure 16: Global Semiconductor Market - By Geography

Figure 17: Global Semiconductor Market Value & Volume, By Geography, 2023-2030 ($)

Figure 18: Global Semiconductor Market CAGR, By Geography, 2023-2030 (%)

Figure 19: North America Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 20: US Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 21: US GDP and Population, 2023-2030 ($)

Figure 22: US GDP – Composition of 2023, By Sector of Origin

Figure 23: US Export and Import Value & Volume, 2023-2030 ($)

Figure 24: Canada Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 25: Canada GDP and Population, 2023-2030 ($)

Figure 26: Canada GDP – Composition of 2023, By Sector of Origin

Figure 27: Canada Export and Import Value & Volume, 2023-2030 ($)

Figure 28: Mexico Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 29: Mexico GDP and Population, 2023-2030 ($)

Figure 30: Mexico GDP – Composition of 2023, By Sector of Origin

Figure 31: Mexico Export and Import Value & Volume, 2023-2030 ($)

Figure 32: South America Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 33: Brazil Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 34: Brazil GDP and Population, 2023-2030 ($)

Figure 35: Brazil GDP – Composition of 2023, By Sector of Origin

Figure 36: Brazil Export and Import Value & Volume, 2023-2030 ($)

Figure 37: Venezuela Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 38: Venezuela GDP and Population, 2023-2030 ($)

Figure 39: Venezuela GDP – Composition of 2023, By Sector of Origin

Figure 40: Venezuela Export and Import Value & Volume, 2023-2030 ($)

Figure 41: Argentina Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 42: Argentina GDP and Population, 2023-2030 ($)

Figure 43: Argentina GDP – Composition of 2023, By Sector of Origin

Figure 44: Argentina Export and Import Value & Volume, 2023-2030 ($)

Figure 45: Ecuador Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 46: Ecuador GDP and Population, 2023-2030 ($)

Figure 47: Ecuador GDP – Composition of 2023, By Sector of Origin

Figure 48: Ecuador Export and Import Value & Volume, 2023-2030 ($)

Figure 49: Peru Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 50: Peru GDP and Population, 2023-2030 ($)

Figure 51: Peru GDP – Composition of 2023, By Sector of Origin

Figure 52: Peru Export and Import Value & Volume, 2023-2030 ($)

Figure 53: Colombia Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 54: Colombia GDP and Population, 2023-2030 ($)

Figure 55: Colombia GDP – Composition of 2023, By Sector of Origin

Figure 56: Colombia Export and Import Value & Volume, 2023-2030 ($)

Figure 57: Costa Rica Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 58: Costa Rica GDP and Population, 2023-2030 ($)

Figure 59: Costa Rica GDP – Composition of 2023, By Sector of Origin

Figure 60: Costa Rica Export and Import Value & Volume, 2023-2030 ($)

Figure 61: Europe Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 62: U.K Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 63: U.K GDP and Population, 2023-2030 ($)

Figure 64: U.K GDP – Composition of 2023, By Sector of Origin

Figure 65: U.K Export and Import Value & Volume, 2023-2030 ($)

Figure 66: Germany Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 67: Germany GDP and Population, 2023-2030 ($)

Figure 68: Germany GDP – Composition of 2023, By Sector of Origin

Figure 69: Germany Export and Import Value & Volume, 2023-2030 ($)

Figure 70: Italy Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 71: Italy GDP and Population, 2023-2030 ($)

Figure 72: Italy GDP – Composition of 2023, By Sector of Origin

Figure 73: Italy Export and Import Value & Volume, 2023-2030 ($)

Figure 74: France Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 75: France GDP and Population, 2023-2030 ($)

Figure 76: France GDP – Composition of 2023, By Sector of Origin

Figure 77: France Export and Import Value & Volume, 2023-2030 ($)

Figure 78: Netherlands Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 79: Netherlands GDP and Population, 2023-2030 ($)

Figure 80: Netherlands GDP – Composition of 2023, By Sector of Origin

Figure 81: Netherlands Export and Import Value & Volume, 2023-2030 ($)

Figure 82: Belgium Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 83: Belgium GDP and Population, 2023-2030 ($)

Figure 84: Belgium GDP – Composition of 2023, By Sector of Origin

Figure 85: Belgium Export and Import Value & Volume, 2023-2030 ($)

Figure 86: Spain Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 87: Spain GDP and Population, 2023-2030 ($)

Figure 88: Spain GDP – Composition of 2023, By Sector of Origin

Figure 89: Spain Export and Import Value & Volume, 2023-2030 ($)

Figure 90: Denmark Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 91: Denmark GDP and Population, 2023-2030 ($)

Figure 92: Denmark GDP – Composition of 2023, By Sector of Origin

Figure 93: Denmark Export and Import Value & Volume, 2023-2030 ($)

Figure 94: APAC Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 95: China Semiconductor Market Value & Volume, 2023-2030

Figure 96: China GDP and Population, 2023-2030 ($)

Figure 97: China GDP – Composition of 2023, By Sector of Origin

Figure 98: China Export and Import Value & Volume, 2023-2030 ($) Semiconductor Market China Export and Import Value & Volume, 2023-2030 ($)

Figure 99: Australia Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 100: Australia GDP and Population, 2023-2030 ($)

Figure 101: Australia GDP – Composition of 2023, By Sector of Origin

Figure 102: Australia Export and Import Value & Volume, 2023-2030 ($)

Figure 103: South Korea Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 104: South Korea GDP and Population, 2023-2030 ($)

Figure 105: South Korea GDP – Composition of 2023, By Sector of Origin

Figure 106: South Korea Export and Import Value & Volume, 2023-2030 ($)

Figure 107: India Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 108: India GDP and Population, 2023-2030 ($)

Figure 109: India GDP – Composition of 2023, By Sector of Origin

Figure 110: India Export and Import Value & Volume, 2023-2030 ($)

Figure 111: Taiwan Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 112: Taiwan GDP and Population, 2023-2030 ($)

Figure 113: Taiwan GDP – Composition of 2023, By Sector of Origin

Figure 114: Taiwan Export and Import Value & Volume, 2023-2030 ($)

Figure 115: Malaysia Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 116: Malaysia GDP and Population, 2023-2030 ($)

Figure 117: Malaysia GDP – Composition of 2023, By Sector of Origin

Figure 118: Malaysia Export and Import Value & Volume, 2023-2030 ($)

Figure 119: Hong Kong Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 120: Hong Kong GDP and Population, 2023-2030 ($)

Figure 121: Hong Kong GDP – Composition of 2023, By Sector of Origin

Figure 122: Hong Kong Export and Import Value & Volume, 2023-2030 ($)

Figure 123: Middle East & Africa Semiconductor Market Middle East & Africa 3D Printing Market Value & Volume, 2023-2030 ($)

Figure 124: Russia Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 125: Russia GDP and Population, 2023-2030 ($)

Figure 126: Russia GDP – Composition of 2023, By Sector of Origin

Figure 127: Russia Export and Import Value & Volume, 2023-2030 ($)

Figure 128: Israel Semiconductor Market Value & Volume, 2023-2030 ($)

Figure 129: Israel GDP and Population, 2023-2030 ($)

Figure 130: Israel GDP – Composition of 2023, By Sector of Origin

Figure 131: Israel Export and Import Value & Volume, 2023-2030 ($)

Figure 132: Entropy Share, By Strategies, 2023-2030* (%) Semiconductor Market

Figure 133: Developments, 2023-2030* Semiconductor Market

Figure 134: Company 1 Semiconductor Market Net Revenue, By Years, 2023-2030* ($)

Figure 135: Company 1 Semiconductor Market Net Revenue Share, By Business segments, 2023 (%)

Figure 136: Company 1 Semiconductor Market Net Sales Share, By Geography, 2023 (%)

Figure 137: Company 2 Semiconductor Market Net Revenue, By Years, 2023-2030* ($)

Figure 138: Company 2 Semiconductor Market Net Revenue Share, By Business segments, 2023 (%)

Figure 139: Company 2 Semiconductor Market Net Sales Share, By Geography, 2023 (%)

Figure 140: Company 3 Semiconductor Market Net Revenue, By Years, 2023-2030* ($)

Figure 141: Company 3 Semiconductor Market Net Revenue Share, By Business segments, 2023 (%)

Figure 142: Company 3 Semiconductor Market Net Sales Share, By Geography, 2023 (%)

Figure 143: Company 4 Semiconductor Market Net Revenue, By Years, 2023-2030* ($)

Figure 144: Company 4 Semiconductor Market Net Revenue Share, By Business segments, 2023 (%)

Figure 145: Company 4 Semiconductor Market Net Sales Share, By Geography, 2023 (%)

Figure 146: Company 5 Semiconductor Market Net Revenue, By Years, 2023-2030* ($)

Figure 147: Company 5 Semiconductor Market Net Revenue Share, By Business segments, 2023 (%)

Figure 148: Company 5 Semiconductor Market Net Sales Share, By Geography, 2023 (%)

Figure 149: Company 6 Semiconductor Market Net Revenue, By Years, 2023-2030* ($)

Figure 150: Company 6 Semiconductor Market Net Revenue Share, By Business segments, 2023 (%)

Figure 151: Company 6 Semiconductor Market Net Sales Share, By Geography, 2023 (%)

Figure 152: Company 7 Semiconductor Market Net Revenue, By Years, 2023-2030* ($)

Figure 153: Company 7 Semiconductor Market Net Revenue Share, By Business segments, 2023 (%)

Figure 154: Company 7 Semiconductor Market Net Sales Share, By Geography, 2023 (%)

Figure 155: Company 8 Semiconductor Market Net Revenue, By Years, 2023-2030* ($)

Figure 156: Company 8 Semiconductor Market Net Revenue Share, By Business segments, 2023 (%)

Figure 157: Company 8 Semiconductor Market Net Sales Share, By Geography, 2023 (%)

Figure 158: Company 9 Semiconductor Market Net Revenue, By Years, 2023-2030* ($)

Figure 159: Company 9 Semiconductor Market Net Revenue Share, By Business segments, 2023 (%)

Figure 160: Company 9 Semiconductor Market Net Sales Share, By Geography, 2023 (%)

Figure 161: Company 10 Semiconductor Market Net Revenue, By Years, 2023-2030* ($)

Figure 162: Company 10 Semiconductor Market Net Revenue Share, By Business segments, 2023 (%)

Figure 163: Company 10 Semiconductor Market Net Sales Share, By Geography, 2023 (%)

Figure 164: Company 11 Semiconductor Market Net Revenue, By Years, 2023-2030* ($)

Figure 165: Company 11 Semiconductor Market Net Revenue Share, By Business segments, 2023 (%)

Figure 166: Company 11 Semiconductor Market Net Sales Share, By Geography, 2023 (%)

Figure 167: Company 12 Semiconductor Market Net Revenue, By Years, 2023-2030* ($)

Figure 168: Company 12 Semiconductor Market Net Revenue Share, By Business segments, 2023 (%)

Figure 169: Company 12 Semiconductor Market Net Sales Share, By Geography, 2023 (%)

Figure 170: Company 13 Semiconductor Market Net Revenue, By Years, 2023-2030* ($)

Figure 171: Company 13 Semiconductor Market Net Revenue Share, By Business segments, 2023 (%)

Figure 172: Company 13 Semiconductor Market Net Sales Share, By Geography, 2023 (%)

Figure 173: Company 14 Semiconductor Market Net Revenue, By Years, 2023-2030* ($)

Figure 174: Company 14 Semiconductor Market Net Revenue Share, By Business segments, 2023 (%)

Figure 175: Company 14 Semiconductor Market Net Sales Share, By Geography, 2023 (%)

Figure 176: Company 15 Semiconductor Market Net Revenue, By Years, 2023-2030* ($)

Figure 177: Company 15 Semiconductor Market Net Revenue Share, By Business segments, 2023 (%)

Figure 178: Company 15 Semiconductor Market Net Sales Share, By Geography, 2023 (%)

The Semiconductor market is estimated to grow at a CAGR of 7.1% during the forecast period 2023-2030.

The Global Semiconductor Market size is estimated at US$578 billion in 2022. It is projected to reach US$990 Billion by 2030.

The leading players in the Semiconductor market are Qualcomm Technologies, Inc, Broadcom, Inc, Intel Corporation, Samsung Electronics and Taiwan Semiconductors.

Growth in the work-from-home trend across the globe has significantly increased the demand for PCs and laptops, thus resulting in the growth of the semiconductor market. Technological developments in end-use industries are other key trends impacting the market.

The increasing demand for semiconductors in the industrial equipment and automotive sectors and the growing demand for integrated circuits in developing nations are driving the Semiconductor Market growth. The rapid growth in AI, machine learning, IoT and wireless communications devices is creating new opportunities for the market.