Email

Email Print

Print

Wind Power Market Overview:

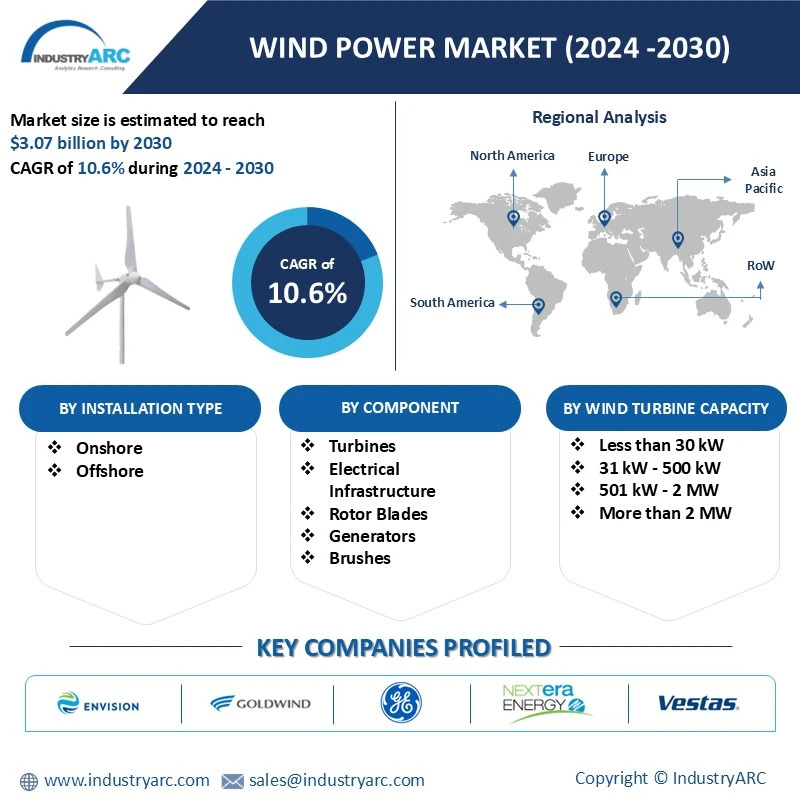

The Wind Power Market size is estimated to reach $3.07 Billion by 2030, growing at a CAGR of 10.6% during the forecast period 2024-2030. The global wind power market has experienced significant growth due to rising environmental concerns, increasing energy demand, and supportive government policies. Wind energy, a renewable and sustainable power source, is harnessed through onshore and offshore wind farms using advanced turbines. Onshore wind farms dominate the market due to lower installation costs and established infrastructure. However, offshore wind farms are gaining traction due to higher efficiency and less land use. Key regions driving market expansion include Europe, North America, and Asia-Pacific, with countries like China, the U.S., and Germany leading in installed capacity.

Technological advancements in turbine design, energy storage, and grid integration have enhanced efficiency and reduced costs, boosting market growth. Additionally, corporate power purchase agreements (PPAs) and investments in wind energy projects by major players such as Vestas, Siemens Gamesa, and General Electric further fuel expansion. Challenges include high initial capital costs, environmental concerns related to wildlife impacts, and grid connectivity issues. Despite these, the wind power market is expected to grow steadily, driven by global decarbonization goals, technological progress, and increasing renewable energy adoption.

Market Snapshot:

Wind Power Market - Report Coverage:

The “Wind Power Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Wind Power Market.

|

Attribute |

Segment |

|

By Installation Type |

|

|

By Component |

|

|

By Wind Turbine Capacity |

|

|

By Technology |

|

|

By Connectivity |

|

|

By End Users |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic disrupted the wind power market through supply chain interruptions, project delays, and labor shortages. However, government stimulus packages and green energy policies accelerated renewable energy investments. Post-pandemic, market recovery was driven by increased demand for sustainable energy, technological advancements, and supportive regulatory frameworks fostering wind power expansion globally.

- The Ukraine crisis intensified energy security concerns, driving global interest in renewable energy, including wind power. Europe accelerated wind project installations to reduce reliance on Russian gas. However, supply chain disruptions, rising raw material costs, and geopolitical uncertainty affected project timelines, prompting governments to boost investments and streamline wind energy development policies.

Key Takeaways:

Asia-Pacific Region is Projected as Fastest Growing Region

Asia-Pacific is projected as the fastest growing region in Wind Power Market with CAGR of 10.8% during the forecast period 2024-2030. Major economies like China, India, and Australia are at the forefront, benefiting from large-scale wind energy projects and favorable regulatory frameworks promoting renewable energy adoption. China, the global leader in wind power capacity, continues to dominate with aggressive onshore and offshore wind installations. India's renewable energy targets have accelerated wind power investments, supported by government incentives such as feed-in tariffs and renewable energy certificates. Australia also plays a key role, with significant wind farm developments contributing to its renewable energy transition. Technological improvements, such as advanced turbine designs and more efficient grid integration, further propel the region's growth. Additionally, international collaborations and private sector investments strengthen the wind energy ecosystem. By 2030, Asia-Pacific is expected to achieve the highest compound annual growth rate (CAGR) in the global wind power market, reflecting its strong commitment to a sustainable energy future.

Rotor blades Segment to Register the Fastest Growth

Rotor blades have emerged as the highest-growing component with a CAGR of 11.2% during the forecast period 2024-2030. This growth is driven by technological advancements aimed at enhancing efficiency and energy output. Rotor blades play a crucial role in converting wind energy into mechanical power, and manufacturers are continuously innovating by using lightweight composite materials, optimizing aerodynamic designs, and increasing blade lengths to capture more wind energy. The global shift toward renewable energy and supportive government policies further fuel demand for rotor blades. Key market players are investing in research and development to produce durable blades with reduced maintenance needs. Additionally, the offshore wind sector's expansion, where longer blades are essential for maximizing energy capture, contributes significantly to this segment’s growth. Asia-Pacific leads the rotor blade market, driven by large-scale wind projects in China and India, supported by favorable policies and increased investments in renewable energy infrastructure. This trend is expected to continue, making rotor blades the fastest-growing segment within the wind power market’s component landscape.

Onshore are Leading the Market

Onshore held the largest market share of 77.1% in the Wind Power market in 2023. This leadership is driven by the lower installation and maintenance costs associated with onshore wind farms compared to offshore setups. Onshore wind turbines are typically installed in rural and remote areas where large expanses of land are available, making large-scale projects more feasible. The onshore segment benefits from established technology and ease of access for construction and maintenance. Additionally, governments worldwide continue to support onshore wind projects through incentives and favourable policies, boosting the segment’s growth. While offshore wind farms are growing due to higher wind speeds at sea, the logistical and financial challenges they present have kept the onshore segment in the lead for now.

Rising Energy Demand and Grid Integration Needs

The increasing global energy demand is a major driver of the wind power market. As economies grow, particularly in developing regions, the need for sustainable and scalable energy sources becomes critical. Wind power, being renewable and eco-friendly, meets this demand while addressing climate concerns. Additionally, advancements in grid integration technologies have facilitated the seamless incorporation of wind-generated electricity into national grids. Modern grid systems equipped with smart inverters and energy storage solutions ensure stable power supply even during wind intermittency. Energy diversification strategies pursued by governments and utilities further bolster wind power adoption, ensuring long-term market growth.

Corporate Sustainability Initiatives

Corporate commitment to sustainability goals is significantly driving the wind power market. Businesses across industries are investing in wind power to meet carbon neutrality targets and reduce operational emissions. Many corporations have signed power purchase agreements (PPAs) with wind farm operators, ensuring long-term renewable energy supply at fixed rates. Companies such as Google, Amazon, and Microsoft have made substantial wind energy investments to align with global sustainability standards and improve brand reputation. This trend is expected to accelerate as environmental, social, and governance (ESG) standards become central to business strategies globally.

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Wind Power Market. The top 10 companies in this industry are listed below:

- Vestas Wind Systems A/S

- NextEra Energy

- GE Renewable Energy

- Goldwind

- Envision Energy

- Nordex Group

- Enercon GmbH

- MingYang Smart Energy Group

- Suzlon Energy Limited

- Siemens Energy

Scope of the Report:

|

Report Metric |

Details |

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

10.6% |

|

Market Size in 2030 |

$3.07 Billion |

|

Segments Covered |

By Installation Type, By Component, By Wind Turbine Capacity, By Technology, By Connectivity, By End-Users, By Geography |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Indonesia, Malaysia and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|