Email

Email Print

Print

Merchant Hydrogen Market- By Process , By Type , By End Use Industry , By Distribution , By Geography - Global Opportunity Analysis & Industry Forecast, 2024-2030

Merchant Hydrogen Market Overview:

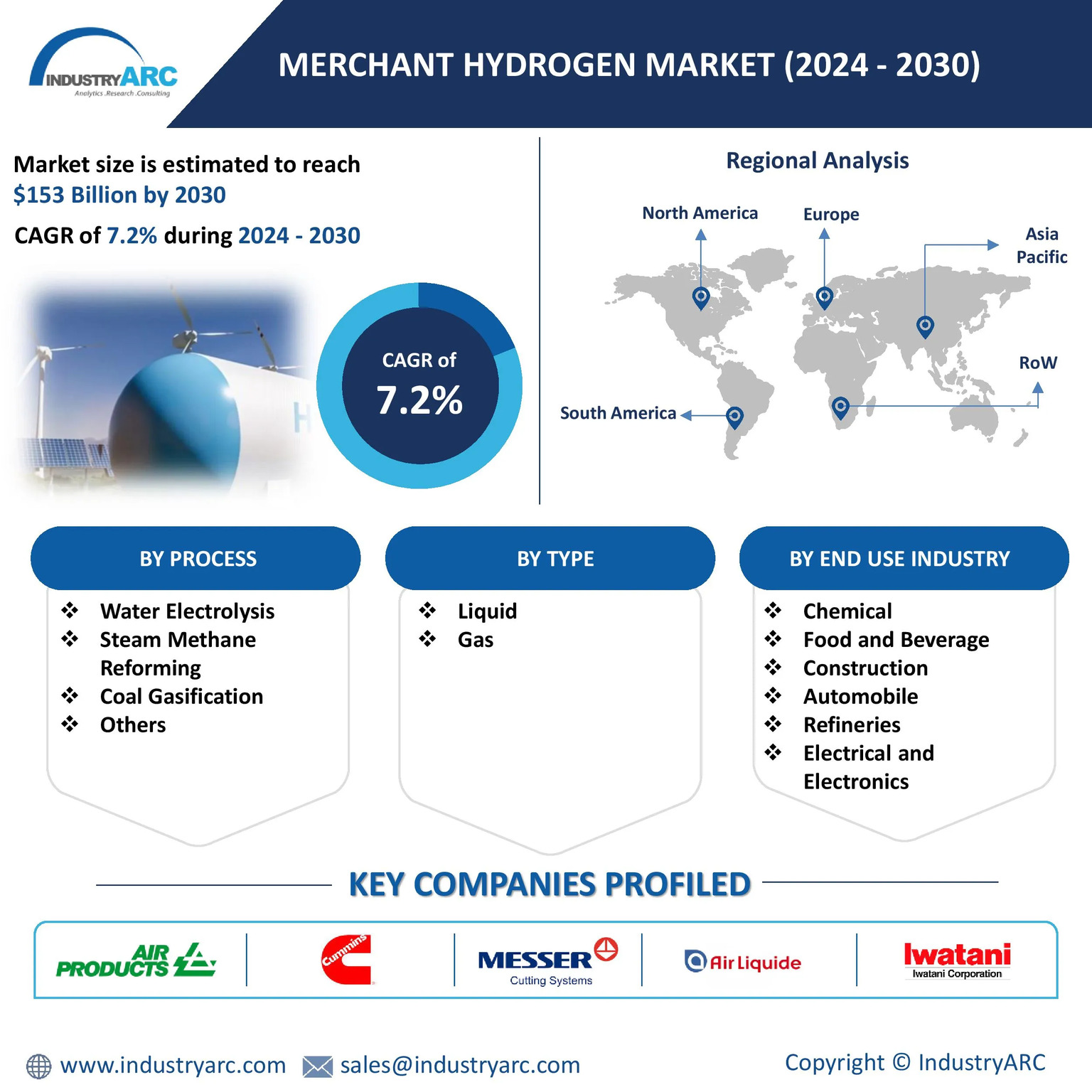

Merchant Hydrogen Market size is estimated to reach $153 billion by 2030, growing at a CAGR of 7.2% during the forecast period 2024-2030. Merchant hydrogen refers to hydrogen that is produced in a central facility or on-site and then sold to consumers for industrial use. Merchant hydrogen is used in the manufacturing of gasoline, diesel, jet fuel, plastics, metals, food products and pharmaceuticals. Increasing global efforts to reduce carbon emissions drive demand for hydrogen in industries and transport. Additionally, government incentives, subsidies and frameworks also propel market expansion. A major trend in the market is the rise in adoption of hydrogen in automotive industry. For instance, Heavy-duty commercial trucks that run on hydrogen rather than diesel are known as hydrogen-powered semi-trucks or hydrogen fuel cell semi-trucks. By offering an environmentally friendly substitute for conventional semi-trucks, this design lowers emissions and moves the transportation sector towards a more sustainable future. According to the International Energy Agency (IEA), heavy-duty vehicles, including semi-trucks, make up less than 8% of all vehicles but account for over 35% of direct CO2 emissions from road transport. Thus, the evolution of hydrogen-powered vehicles is propelling the market growth. Additionally, several countries worldwide initiatives on hydrogen-powered trains, joining global efforts to decarbonize rail transport is fueling the growth of merchant hydrogen market globally. This represents the Merchant Hydrogen Market Outlook.

Market Snapshot:

Merchant Hydrogen Market- Report Coverage:

The “Merchant Hydrogen Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the

| Attribute | Segment |

|---|---|

|

By Process |

|

|

By Type |

|

|

By End Use Industry |

|

|

By Distribution |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- Due to COVID the merchant hydrogen industry was heavily impacted. The pandemic's effects on the world economy resulted in a decline in demand for industrial gases, such as hydrogen, especially in industries like manufacturing and transportation. Many hydrogen projects, especially large-scale ones, faced delays due to disruptions in construction and financing.

- The Russia-Ukraine conflict impacted the Merchant Hydrogen market. Rising energy prices and inflation have increased the cost of producing and transporting hydrogen. The crisis has disrupted global supply chains, affecting the availability of critical components and materials for hydrogen production and infrastructure

Key Takeaways:

-

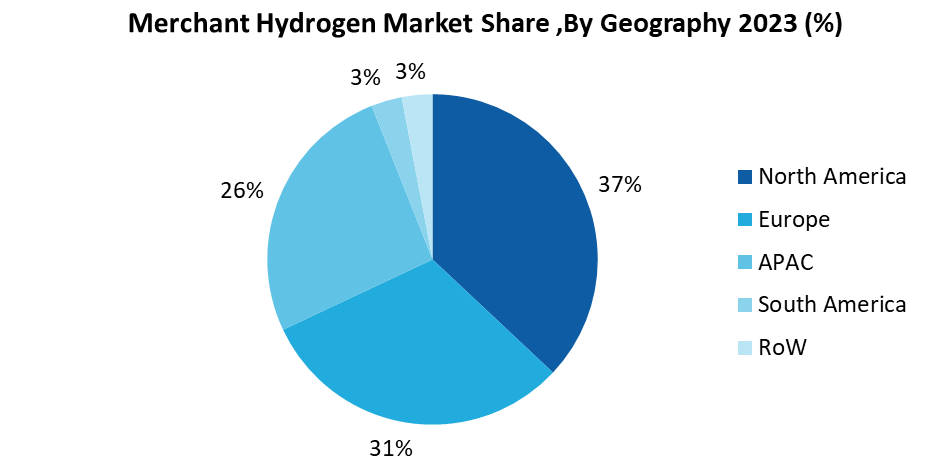

North America Dominates the Market

North America is the dominant region in the Merchant Hydrogen market due to its established hydrogen production infrastructure and increasing demand from industries such as refineries, chemicals and transportation. In January 2024, U.S. Department of Energy announced $623 million in grants to help build hydrogen refueling infrastructure and an electric vehicle charging network across the United States. More than $90 million in funding will support projects in California, Colorado, and Texas that will deploy clean hydrogen fueling infrastructure for medium-duty and heavy-duty vehicles. In March 2024, The University of Texas at Austin (UT) published a report entitled A Framework for Hydrogen in Texas that outlines the state's capabilities to produce clean hydrogen at a competitive cost. The report, led by researchers at UT, outlines the benefits, challenges, and opportunities associated with scaling up the clean hydrogen industry in Texas. Such factors are driving the growth of merchant hydrogen market in this region.

-

Steam Methane Reforming is the Largest Segment

In the Merchant Hydrogen market, Steam Methane Reforming (SMR) is the largest segment, by process. SMR produces a hydrogen rich gas that is typically on the order of 70-75% hydrogen on a dry mass basis, along with smaller amounts of methane, carbon monoxide and carbon dioxide as per Clean Energy States Alliance report. For instance, according to U.S. Department of Energy, around 95% of hydrogen is produced by this process in the United States. A steam methane reformer provides the user with high-purity gas at a reasonable price. Because of its high purity, hydrogen produced by steam methane reformers is mostly used in industrial operations for goods like ammonia manufacture and petroleum refining. Additionally, the efficiency of the method is around 70-80% with a Technology Readiness Level (TRL) of 9. Steam reforming can also produce hydrogen from other fuels such as ethanol, propane, and gasoline. Thus, the steam methane reforming process is growing in merchant hydrogen market globally.

-

Chemical is the Largest Segment

The chemical sector dominates the merchant hydrogen market due to its usage in several key chemicals. Ammonia manufacturing, for instance, is the largest consumer of hydrogen. Ammonia, a critical component of fertilizers, is primarily produced through the Haber-Bosch process. This process requires a substantial amount of hydrogen gas as a key reactant. For instance, In August 2024, AM Green Ammonia B.V. announced it has reached Final Investment Decision (FID) for its first million-ton green ammonia project located in the Kakinada district of the Indian state of Andhra Pradesh. The company aims to achieve a green ammonia production capacity of 5 million ton per annum (mtpa) by 2030—equivalent to about 1 mtpa of green hydrogen. In addition to the Kakinada project, AM Green plans green ammonia production across multiple locations in India to achieve its planned 5 mtpa of green ammonia capacity by 2030. Such factors are propelling the growth of chemical segment in Merchant Hydrogen market globally.

-

Growing Demand for Clean Fuel to Drive the Market

Growing demand for clean fuel globally is driving the growth of merchant hydrogen market globally. The rise in need to reduce greenhouse gas emissions and mitigate climate change is driving the demand for cleaner energy sources. For instance, Chinese government is targeting to build at least 1,200 hydrogen refueling stations for mobility across the country by 2025, according to a journal from emerging technology news. Additionally, China is forecast to have 12,000 to 18,000 fuel-cell vehicles (FCVs) plying its roads in 2024. This success in FCVs is generating demand for hydrogen refueling stations, and even the country's local governments have now begun to include in plans and regulations. The expansion of hydrogen refueling stations is essential to support the growth of the FCEV, further boosting demand for merchant hydrogen market.

High Production Cost to Hamper the Market

One of the key challenges in the merchant hydrogen market is the high production cost. For instance, as per A strategic analysis of hydrogen energy in QUAD nations journal, the cost of producing hydrogen in the US is high despite the considerable investment in R&D to reduce production costs. The cost of generating hydrogen varies depending on the source. For instance, the cost of producing hydrogen is $2.4/kg from fossil fuels, $2/kg from CCS, $4/kg from electrolyzed water, $3.6/kg from solar thermochemical methods, and $3.7/kg from wind. Large capital expenditures are required to build large-scale hydrogen production plants, particularly those which depend on renewable energy sources. However, ambitious initiatives like the Hydrogen Shot are working to drastically reduce the cost of clean hydrogen to $1 per kilogram within a decade, accelerating the clean energy transition.

For more details on this report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Merchant Hydrogen Market. The top 10 companies in this industry are listed below:

Linde plc

- Air Liquide

- Air Products and Chemicals, Inc.

- Messer Group GmbH

- Iwatani Corporation

- Cummins Inc.

- ENGIE

- Uniper SE

- Kenan Advantage Group, Inc.

- Taiyo Nippon Sanso Corporation

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

7.2% |

|

Market Size in 2030 |

$153 Billion |

|

Segments Covered |

By Process, By Type, By End Use Industry, By Distribution and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Netherlands, Belgium and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Indonesia, Malaysia, Thailand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

For more Chemicals and Materials Market reports, please click here

The Merchant Hydrogen Market is projected to grow at 7.2% CAGR during the forecast period 2024-2030.

The Merchant Hydrogen Market size is estimated to be $93.9 billion in 2023 and is projected to reach $153 Billion by 2030.

The leading players in the Merchant Hydrogen Market are Linde plc, Air Liquide, Air Products and Chemicals, Inc., Messer Group GmbH, Iwatani Corporation, Cummins Inc. and Others.

The rise in adoption of green hydrogen in trains and Integration of hydrogen in several industrial processes like steel production and chemicals are some of the market trends in the industry which will create growth opportunities for the market during the forecast period.

Key driving factors include increasing global efforts to reduce carbon emissions, government incentives, subsidies, frameworks and policies for hydrogen production, growing usage of ultra-low sulfur diesel and growing demand for chemicals are the driving factors of the market.