Email

Email Print

Print

Online Gaming Market Overview

Online gaming market is anticipated to reach $152.6 billion by 2030 with a CAGR of 9.1% in the forecast period 2024-2030. This growth is owing to the increased spending on online games and the growing penetration of smartphones & tablets. In addition, availability of high-speed internet connectivity and reliable network is also one of the key factors fuelling the demand for online gaming solutions and services. Moreover, constant improvements in network connectivity and advancements in AR, VR, and XR technologies are estimated to provide key growth opportunities for the iGaming market in forecast period 2024-2030.

Additionally, the ascent of mobile gaming within the online gaming market is emblematic of a significant shift propelled by the ubiquitous presence of smartphones. This evolution has positioned mobile gaming as a pivotal and burgeoning segment, capitalizing on its inherent convenience and accessibility. With smartphones becoming a staple in daily life, consumers increasingly turn to mobile platforms for their gaming entertainment, fostering a broad and diverse audience. As a result, mobile gaming has emerged as a dominant force within the online gaming market, shaping industry dynamics and offering lucrative opportunities for developers and stakeholders alike.

Moreover, companies are strategically leveraging in-game purchases and microtransactions as key revenue streams. By offering players virtual goods, skins, and additional content for a fee, these companies capitalize on the demand for personalized gaming experiences and aesthetic enhancements. This monetization strategy not only drives profitability but also fosters player engagement and retention. Through carefully curated in-game economies, companies cultivate a dynamic ecosystem where players can customize their gaming experiences while contributing to the sustained growth of the online gaming market.

Online Gaming Market Report Coverage

The report: “Online Gaming Market Forecast (2024-2030)”, by Industry ARC, covers an in-depth analysis of the following segments of the Gait Trainer Market.

By Type: Smartphones Online Gaming, Tablets Online Gaming, Gaming Consoles, Handheld Consoles, PC, Others.

By Gender: Male, Female.

By Age : Below 18, 18 to 35, 36 to 49 and 50 and above.

By Game Genre: First Person Shooter (FPS), Sports, Battle Royale, Real time strategy (RTS), Role Playing Games (RPG), Racing, Strategy, Simulation, Adventure, Puzzle, Social, Educational, others.

By Game Type: Single player, Multi player, MMO, and Others.

By Channel: Browser Based, App Based, Preloaded/Offline Purchase, and Others.

By Channel: Free To Play, Freemium, Pay to Play, Subscription, Pay per Download, One Time Purchase, Others.

By Geography: North America (U.S., Canada, Mexico), Europe (Germany, U.K., France, Italy, Spain, Russia and Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia & New Zealand, and Rest of Asia Pacific), South America (Brazil, Argentina and Rest of South America), and Rest of the World (Middle East and Africa)

Key Takeaways

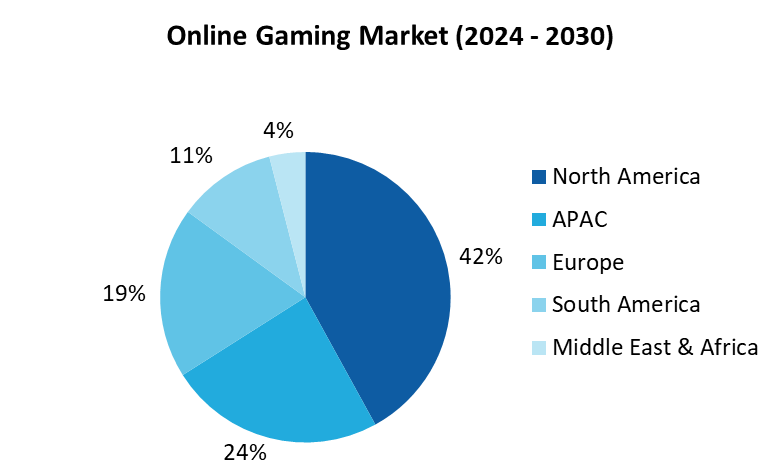

- North America dominated the online gaming market size with more than 42%. Owing to rise in investments, internet usage and government support

- Smart phone online gaming market is anticipated to grow at a CAGR of 6.5% in the forecast period 2024-2030. Owing to high smartphone and internet penetration across the globe, the market is projected to grow rapidly in the forecast period.

- Virtual reality in online gaming is growing at a highest CAGR in the forecast period. Most of the virtual reality input devices are prototypes, and companies are investing heavily in Research & Development (R&D) to build consumer versions which can be connected to consoles, desktops, and smartphones.

- Online gaming top 10 companies include Ubisoft, Activision Blizzard, Zynga Inc., Microsoft, Betsson AB, Konami, Sega, Sony Corp., Tencent, and Wargaming

For More Details on This Report - Request for Sample

By Type- Segment Analysis

Smart phone online gaming market is anticipated to grow at a CAGR of 4.5% in the forecast period 2024-2030. High smartphone and internet penetration across the globe is enhancing the markets to grow rapidly in the forecast period. Online Mobile games are becoming more popular and attract players with additional premium contents or functionalities. Games such as Battle Royale hits Fortnite and PUBG are still driving the market’s growth and shape online gaming in general. With the rapid penetration of these online games, several gaming companies have been investing heavily for the development of Battle Royale and other online mobile games. In 2022, esports tournaments hosted a cumulative prize pool of US$ 3.2 million. Web3 gaming firms in India raised $620.5 mn in 2022 across 32 deals. Hence these fundings help the gaming industries to develop innovative smartphone and other games thereby accelerating the market in the forecast period 2024-2030.

By game genre - Segment Analysis

Battle royal in online gaming is growing at a highest CAGR in the forecast period. Significant development of new mechanisms, gameplay features and other are enhancing this genre to grow in the forecast period. Battle royal games such as PUBG Mobile / Game for Peace in China and Asia Pacific, Garena Free Fire in Latin America, and Fortnite, Apex Legends in the United States have been witnessing a strong growth in their respective region in the forecast period. Honor of Kings is identified as the year’s top performer, earning more than $2.2 billion throughout the year. Moreover, companies such as Tencent and Ubisoft have invested heavily for development of games in this genre. A number of leading FPS games have also had a battle royale mode launched over the last couple of years including Call of Duty (Activision), Counter Strike (Valve) as well as a number of independent game titles focused on this sector. Hence these developments are analyzed to drive the market in the forecast period 2024-2030.

By Geography - Segment Analysis

In 2023, North America dominated the online gaming market share with more than 42%. Owing to rise in usage of smartphone and internet. In 2023, internet penetration in the region reached 93% and the average time spent across digital media by an adult has increased. For instance, mobile users in the US spent an average of 3hrs 28mins on their devices in 2023. Moreover, with the increasing number of 5G connections in the region, the market is expected to witness further growth. Hence these benefits are analyzed to drive the market for online gaming in the forecast period 2024-2030.

Drivers – Online Gaming Market

• Growing Support from the government

In recent years, Governments across several countries are realizing the potential and reach of the online games and providing incentives for gaming studios to develop and retain their creative, technology and employees locally as well as programs that aim to attract foreign talent. In Sweden, Sweden Game Arena, a public-private partnership that helps students develop games using government-funded offices and equipment, was set up. Similarly, countries such as U.S, U.K and other are providing several investments and funding to support these industries. Hence with the growing support from the government of several countries, online gaming sector is analyzed to grow in the forecast period 2024-2030.

• Emergence of AI in online gaming

Emergence of AI in online gaming is boosting the market in the forecast period. The use of artificial intelligence in online gaming is significantly increasing owing to the advantages. Several gaming industries have been using AI-techniques in their online games to minimize the chances of cheating and facilitate a fair gaming trend. Similarly, AI determines the player’s behavior in gaming and take actions accordingly. Hence these advantages are analyzed to drive the market in the forecast period 2024-2030.

Challenges –Online Gaming Market

• Increasing Online Fraud, regulatory compliance and profitability pressures

The threat of malicious activity is growing in online gaming where fraudulent transactions can translate to millions of dollars in losses. With more players, more bets, and more financial transactions, the online frauds have been increasing in the forecast period. Although online gaming has a global audience, the laws governing licensing and legal activities vary widely by region, country, and state jurisdictions. On the other hand growing competition among established companies, start-ups, and independent developers to entice new customers with “play-for-free” offerings partially subsidized by ad revenue, in the hopes of transitioning them to more lucrative “pay-to-play” games. To maintain existing revenue streams and create new revenue sources, gaming companies are making sizable, ongoing investments in product development and technology infrastructure. Hence the increasing investments will in turn raise the pressure on these industries and hamper the market growth in the forecast period.

Market Landscape

Technology launches, acquisitions, Partnerships and R&D activities are key strategies adopted by players in the Online gaming market. In 2023, the market of Online gaming market has been fragmented by several companies vying for top share. Online gaming top 10 companies include Ubisoft Entertainment, Blizzard Entertainment, Inc, Zynga Inc, Microsoft, Konami, Sega, Sony, Tencent, Wargaming, Electronic Arts and others.

Acquisitions/Technology Launches

• In October 2023, Microsoft finalized its acquisition of Activision Blizzard, marking the largest deal in the video game industry's history. Valued at $69 billion, this strategic move strengthens Microsoft's position in the online gaming market, offering opportunities for synergies and expansion across gaming platforms and franchises.

• In July 2022, Sony Interactive Entertainment acquired of Haven Entertainment Studios Inc. The move aims to bolster Sony's presence in the online gaming market by expanding its portfolio of gaming studios and enhancing its ability to develop innovative gaming experiences for players worldwide.

For more Information and Communications Technology Market reports, please click here

1. Global Online Gaming - Market Overview

1.1 Definitions and Scope

2. Global Online Gaming - Executive Summary

2.1 Market Revenue, Market Size and Key Trends by Company

2.2 Key trends by type

2.3 Key trends segmented by geography

3. Global Online Gaming - Market Forces

3.1 Market Drivers

3.2 Market Constraints

3.3 Market Opportunities

3.4 Porters five force model

3.4.1 Bargaining power of suppliers

3.4.2 Bargaining powers of customers

3.4.3 Threat of new entrants

3.4.4 Rivalry among existing players

4. Global Online Gaming Market - Startup companies Scenario Premium Premium

4.1Top 10 startup company Analysis by

4.1.1 Investment

4.1.2 Revenue

4.1.3 Market Shares

4.1.4 Market Size and Application Analysis

4.1.5 Venture Capital and Funding Scenario

5. Global Online Gaming Market - Industry Market Entry Scenario Premium Premium

5.1 Regulatory Framework Overview

5.2 New Business and Ease of Doing business index

5.3 Case studies of successful ventures

5.4 Customer Analysis - Top 10 companies

6. Global Online Gaming Market – By Type (Market Size -$Million/Billion)

6.1 Smartphones Online Gaming

6.2 Tablets Online Gaming

6.3 Gaming Consoles

6.4 Handheld Consoles

6.5 PC

6.6 Others

7 Global Online Gaming Market – By Gender (Market Size -$Million/Billion)

7.1 Male

7.2 Female

8 Global Online Gaming Market– By Age (Market Size -$Million/Billion)

8.1 Below 18

8.2 18 to 35

8.3 36 to 49

8.4 50 and above

9 Global Online Gaming Market – By Game Genre (Market Size -$Million/Billion)

9.1 First Person Shooter (FPS)

9.2 Sports

9.3 Battle Royale

9.4 Real time strategy (RTS)

9.5 Role Playing Games (RPG)

9.6 Racing

9.7 Strategy

9.8 Simulation

9.9 Adventure

9.10 Puzzle

9.11 Social

9.12 Educational

9.13 others

10 Global Online Gaming Market – By Game Type (Market Size -$Million/Billion)

10.1 Single player

10.2 Multi player

10.3 MMO

10.4 Other

11 Global Online Gaming Market – By Channel (Market Size -$Million/Billion)

11.1 Browser Based

11.2 App Based

11.3 Preloaded/Offline Purchase

11.4 Others

12 Global Online Gaming Market – By Channel (Market Size -$Million/Billion)

12.1 Free To Play

12.2 Freemium

12.3 Pay to Play

12.4 Subscription

12.5 Pay per Download

12.6 One Time Purchase

12.7 Others

13 Global Online Gaming Market – By Geography (Market Size -$Million/Billion)

13.1 North America

13.1.1 U.S

13.1.2 Canada

13.1.3 Mexico

13.2 South America

13.2.1 Brazil

13.2.2 Argentina

13.2.3 Chile

13.2.4 Colombia

13.2.5 Rest of South America

13.3 Europe

13.3.1 U.K

13.3.2 Germany

13.3.3 France

13.3.4 Italy

13.3.5 Spain

13.3.6 Russia

13.3.7 Rest of Europe

13.4 APAC

13.4.1 China

13.4.2 India

13.4.3 Japan

13.4.4 Singapore

13.4.5 Malaysia

13.4.6 South Korea

13.4.7 Australia

13.4.7 Thailand

13.4.7 Rest of APAC

13.5 Rest of World (ROW)

13.5.1 Middle East

13.5.2 Africa

14 Global Online Gaming Market – Entropy

14.1. New product launches

14.2. M&A's, collaborations, JVs and partnerships

15. Global Online Gaming Market– Industry / Segment Competition landscape Premium Premium

15.1. Market Share Analysis

15.1.1. Market Share by Country- Top companies

15.1.2. Market Share by Region- Top companies

15.1.3. Market Share by type of Product / Product category- Top companies

15.2. Best Practises for companies

16. Global Online Gaming Market – Key Company List by Country Premium Premium

17. Global Online Gaming Market Company Analysis

17.1 Ubisoft Entertainment

17.2 Blizzard Entertainment, Inc

17.3 Zynga Inc.

17.4 Microsoft Corporation

17.5 Konami

17.6 Sega

17.7 Sony Corp.

17.8 Tencent

17.9 Wargaming Airy Technology

17.10 Electronic Arts

"*Financials would be provided on a best-efforts basis for private companies"