Email

Email Print

Print

Conveyor Belts Market Overview

Conveyor Belts Market size is estimated at $5.9 billion in 2030, projected to grow at a CAGR of 4.8% during the forecast period 2024-2030. Conveyor belts, comprising two or more pulleys driving a continuous loop, have become integral components in material handling across various industries. The typical belt thickness is approximately 20 mm, although customization exists to cater to diverse end-user requirements. The conveyor belt landscape is undergoing a significant transformation, with technological advancements and constant upgrades driving improvements in efficiency, reliability, and durability. Manufacturers are actively engaged in developing advanced materials and designs, enhancing conveyor belt performance and lifespan. A noteworthy trend is the expanding adoption of conveyor belt systems in new applications beyond traditional sectors like manufacturing and logistics. Industries such as food processing, agriculture, and e-commerce fulfillment centers are increasingly integrating conveyor belts into their operations. The conveyor belt market is experiencing a surge in demand, particularly in emerging economies like China and India. The rapid pace of industrialization and infrastructure development in these regions is fueling the need for efficient material-handling solutions. The construction of malls, airports, and industrial facilities is creating lucrative opportunities for market players. This transformative phase in the global conveyor belt market is characterized by technological innovation, diversification of applications, and the broadening scope of industrial activities in emerging economies. As a result, the conveyor belt industry is poised for continued growth, with advancements in technology and the expanding range of applications continuing to shape the market landscape. Manufacturers and stakeholders are likely to play a pivotal role in driving further innovation and meeting the evolving demands of diverse industries.

Report Coverage

“Conveyor Belts Market– Forecast (2024-2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the Conveyor Belts market.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Key Takeaways

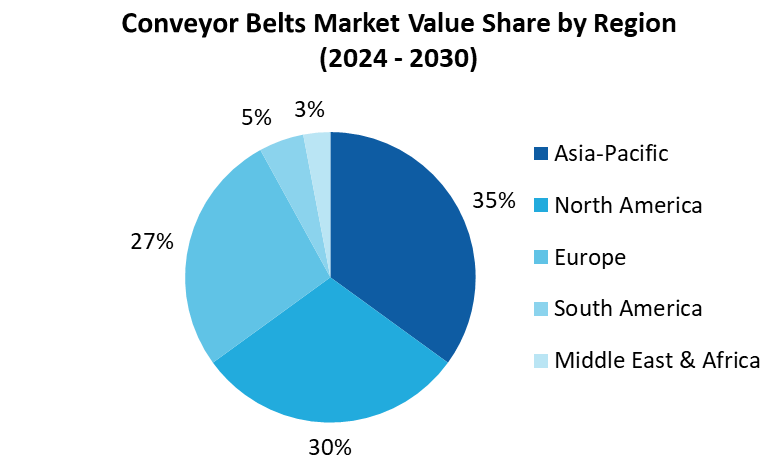

• Geographically Asia Pacific dominated the global conveyor belts market share of 51% in 2023, owing to rapidly increasing population along with urbanization, rising industrial investment, and modernizing infrastructure in developing nations such as China and India in this region. Among all the end-users, the industrial segment has the highest market share in the global conveyor belt market.

• With increasing industrialization globally, there's a rising demand for efficient material handling solutions, which has boosted the demand for conveyor belts

• The conveyor belt market is highly competitive, with key players continuously investing in research and development to introduce innovative products and gain a competitive edge. Mergers, acquisitions, and partnerships are common strategies to expand market presence and product offerings.

For More Details on This Report - Request for Sample

Belt Type - Segment Analysis

Light weight segment dominated the Conveyor Belts Market share in 2023. The demand for lightweight conveyor belts is propelled by increasing consumer reliance on packed food and beverage products. Additionally, the rise in demand for electronic devices necessitates efficient production processes, further driving the need for these conveyor systems. These belts enable seamless transportation, enhancing productivity in various manufacturing sectors, and catering to the evolving needs of modern industries.

End User - Segment Analysis

Food & Beverage dominated the Conveyor Belts Market share in 2023. The demand for food and beverage conveyor belts is driven by several factors including the growing need for automation in food processing, stringent food safety regulations necessitating hygienic handling, increasing demand for packaged foods, and rising adoption of conveyor systems for efficient material handling in the food and beverage industry. Additionally, advancements in conveyor belt technology such as improved durability, flexibility, and easy maintenance contribute to heightened demand. These are factors propel the market growth.

Geography - Segment Analysis

APAC held the largest share 35% of the market in 2023, The APAC region presents abundant manufacturing potential across diverse industries, propelling the need for conveyor belts. In sectors like mining, robust growth forecasts escalate the demand for conveyor belts for efficient material transport. Moreover, small and medium enterprises (SMEs) increasingly embrace conveyor belt usage, especially in emerging economies like India, Indonesia, and Mexico, further fueling market expansion. Additionally, rapid industrialization in countries such as China and India amplifies the demand for streamlined material handling solutions, with conveyor belts playing a pivotal role in facilitating efficient transportation of raw materials in the construction and mining sectors.

Drivers – Conveyor Belts Market

• Growing Manufacturing Activities

The conveyor belt market is poised for robust expansion, buoyed by a surge in global manufacturing endeavors. For instance, in 2022, U.S. manufacturing contributed $2.3 trillion to GDP. Also, The National Manufacturing Policy of the Government of India aims to boost manufacturing's GDP share to 25% by 2025. Moreover, according to the UK statistics, UK manufacturers' product sales totaled $539.84 billion in 2022, highlighting significant industrial output. With manufacturing activities on the rise across various sectors worldwide, the demand for conveyor belts is anticipated to soar. These belts play a pivotal role in streamlining production processes, enhancing efficiency, and reducing operational costs, thus becoming indispensable assets for manufacturing facilities. As industries strive for greater productivity and automation, the conveyor belt market is positioned to capitalize on this trend, projecting a promising trajectory of sustained growth in the foreseeable future.

• Growing the Infrastructure Developments

As nations bolster infrastructure to fuel economic expansion and trade, the demand for conveyor belts escalates. Vital for airports, ports, and logistics centers, these belts facilitate the efficient handling of baggage, cargo, and bulk materials. Their significance lies in streamlining operations, enhancing productivity, and optimizing logistical processes. With ongoing investments in infrastructure projects globally, the need for reliable conveyor systems intensifies, spurring innovation in material design, durability, and automation. Consequently, manufacturers are pushed to meet burgeoning demands, driving advancements in conveyor technology to meet the evolving needs of modern transportation and logistics networks, fostering sustainable growth and development.

Challenges – Conveyor Belts Market

High Initial Installation and Maintenance Costs

The formidable obstacle of high initial installation and maintenance expenses hampers the widespread adoption of conveyor belt systems, impeding market expansion. Businesses face a substantial barrier, as the financial burden associated with these costs deters potential adopters. Overcoming this challenge requires innovative solutions and cost-effective strategies to make conveyor belt systems more accessible and appealing to a broader range of enterprises, ultimately fostering their integration into various industries.

Key Market Players:

The Conveyor Belts Market’s main strategies include innovative product launches, mergers and acquisitions, joint ventures, and R&D activities. Conveyor Belts Market's top 10 companies are

- Bando Chemical Industries

- Continental AG

- Bridgestone corporation

- Bando Chemical Industries, Ltd.

- Habasit AG,

- Ammeraal Beltech, Ltd.

- Mitsuboshi Belting Ltd.

- Forbo Movement Systems

- The Yokohama Rubber Company, Ltd.

- SIG Societ Italiana Gomma S.p.A.

Recent Developments

. In March 2023, Yokohama Rubber introduced Hamaheat Super 80, a high-temperature heat-resistant conveyor belt, catering to steel and cement industries. Designed to endure extreme temperatures, it prevents deterioration caused by conveying materials like ores, cokes, and clinkers. Leveraging advanced rubber compounding technologies, Yokohama delivers durability, extending service life amidst challenging operating conditions.

. In March 2023, Habasit introduced the HabasitLINK M2483 Sphere Top 1” plastic modular belt, enhancing multi-directional movement in logistics and parcel handling. This innovation enables controlled movement of goods across conveyors, offering increased automation and decreased labor needs. As volumes in these facilities surge, the belt provides a solution for efficient, versatile conveying.

. In June 2022, Continental acquired WCCO Belting, a North Dakota-based belting manufacturer, integrating it into its conveying solutions business. This move enhances Continental's portfolio in conveyor belting and strengthens its presence in the agricultural sector. The acquisition promises a comprehensive product and service offering for equipment manufacturers, distributors, dealers, and farmers, ensuring improved support and service.

For more Automation and Instrumentation Market reports, please click here

1. Conveyor Belts Market - Overview

1.1 Definitions and Scope

2. Conveyor Belts Market - Executive Summary

2.1 Key Trends by Belt Type

2.2 Key Trends by Conveyor Module

2.3 Key Trends by End User Industry

2.4 Key Trends by Geography

3. Conveyor Belts Market - Comparative Analysis

3.1 Company Benchmarking

3.2 Global Financial Analysis

3.3 Market Share Analysis

3.4 Patent Analysis

3.5 Pricing Analysis

4. Conveyor Belts Market - Start-up Companies Scenario (Premium)

4.1 Key Start-up Company Analysis by

4.1.1 Investment

4.1.2 Revenue

4.1.3 Venture Capital and Funding Scenario

5. Conveyor Belts Market – Market Entry Scenario Premium (Premium)

5.1 Regulatory Framework Overview

5.2 New Business and Ease of Doing Business Index

5.3 Case Studies of Successful Ventures

6. Conveyor Belts Market - Forces

6.1 Market Drivers

6.2 Market Constraints/Challenges

6.3 Porter’s Five Force Model

6.3.1 Bargaining power of suppliers

6.3.2 Bargaining powers of customers

6.3.3 Threat of new entrants

6.3.4 Rivalry among existing players

6.3.5 Threat of substitutes

7. Conveyor Belts Market – Strategic Analysis

7.1 Value Chain Analysis

7.2 Opportunities Analysis

7.3 Market Life Cycle

8. Conveyor Belts Market – By Belt Type (Market Size -$Million/Billion)

8.1 Light Weight

8.2 Medium Weight

9. Conveyor Belts Market – By Conveyor Module (Market Size -$Million/Billion)

9.1 Telescopic Conveyor/Booms

9.2 Sorting Modules

9.3 Singualtion Modules

9.4 Curved belt Conveyors

9.5 Specialty Belt Conveyors

9.6 Diverting

9.7 Timing

9.8 Others

10. Conveyor Belts Market - By End Use Industry (Market Size-$Million/Billion)

10.1 Automotive

10.2 Aerospace

10.3 Airport

10.4 Retail

10.5 Food & Beverage

10.6 Malls

10.7 Industrial

10.8 Mining

10.9 Oil & Gas

10.10 Others

11. Conveyor Belts Market – by Geography (Market Size - $Million/$Billion)

11.1 North America

11.1.1 U.S.

11.1.2 Canada

11.1.3 Mexico

11.2 Europe

11.2.1 U.K.

11.2.2 Germany

11.2.3 France

11.2.4 Italy

11.2.5 Netherlands

11.2.6 Spain

11.2.7 Rest of Europe

11.3 Asia-Pacific

11.3.1 China

11.3.2 Japan

11.3.3 India

11.3.4 South Korea

11.3.5 Australia & New Zealand

11.3.6 Rest of Asia-Pacific

11.4 South America

11.4.1 Brazil

11.4.2 Argentina

11.4.3 Chile

11.4.4 Colombia

11.4.5 Rest of South America

11.5 Rest of The World

11.5.1 Middle East

11.5.2 Africa

12. Conveyor Belts Market - Entropy

13. Conveyor Belts Market – Industry/Segment Competition Landscape (Premium)

13.1 Market Share Analysis

13.1.1 Global Market Share – Key Companies

13.1.2 Market Share by Region – Key Companies

13.1.3 Market Share by Countries – Key Companies

13.2 Competition Matrix

13.3 Best Practices for Companies

14. Conveyor Belts Market – Key Company List by Country Premium (Premium)

15. Conveyor Belts Market - Company Analysis

15.1 Bando Chemical Industries

15.2 Continental AG

15.3 Bridgestone corporation

15.4 Habasit AG

15.5 Fenner Dunlop

15.6 Ammeraal Beltech, Ltd.

15.7 Mitsubishi Belting Ltd.

15.8 Forbo Movement Systems

15.9 The Yokohama Rubber Company, Ltd.

15.10 SIG Societ Italiana Gomma S.p.A.

* "Financials would be provided to private companies on best-efforts basis."

Connect with our experts to get customized reports that best suit your requirements. Our reports include global-level data, niche markets and competitive landscape.