Email

Email Print

Print

Asia-Pacific Float Glass Market - Forecast(2025 - 2031)

Asia-Pacific Float Glass Market Overview

Asia-Pacific Float Glass Market size is forecast to reach US$68.7 billion by 2030, after growing at a CAGR of 6.4% during 2024-2030. Float glass is an annealed glass, which is often used in buildings for energy-saving purposes. The growth of the float glass (flat glass) market in the Asia-Pacific region is attributed to the high demand for float glass (flat glass) from the expanding construction, automotive & transportation, consumer goods, and solar energy industries in the region. The escalating environmental apprehensions surrounding global warming in the Asia-Pacific region are anticipated to fuel the demand for float glass. This surge is attributed to float glass playing a pivotal role in attaining Leadership in Energy and Environmental Design (LEED) certification for both residential and commercial structures. As sustainable building practices gain momentum, the use of float glass becomes instrumental in enhancing energy efficiency and environmental performance. Its ability to optimize natural light, reduce energy consumption, and contribute to a building's eco-friendly credentials positions float glass as a preferred choice in construction. This burgeoning demand underscores a collective commitment to fostering greener, more sustainable urban development in the face of pressing environmental challenges. Automation and the shift from open mold to closed mold applications are driving an expanding need for glass fabric or glass roving. This transformation enhances efficiency and precision in manufacturing processes. The demand surge underscores the critical role of glass reinforcement in meeting the evolving requirements of modern automated production methods, fostering innovation in various industries.

COVID-19 Impact

During the Covid-19 pandemic, there was a sudden decline in the growth of many end-use industries in Asia-Pacific which widely use float glass that further affected the growth of the Asia-Pacific Float Glass Market. For instance, according to the International Council on Clean Transportation, sales volumes are down year-to-date compared to last year. In the first six months of 2020, China sold an average of 1.3 million new passenger cars per month. This is about a 23% decrease from the first half of 2019. Furthermore, in a survey conducted by the China Construction Industry Association on 15 April 2020, which included 804 businesses, 90.55 percent of respondents said progress had been hampered, and 66.04 percent said there was a labor shortage. Since, during the pandemic, the float glass market saw a decrease in its demand in Asia-Pacific due to many key end-use industries facing challenges during the pandemic, the market revenue of the Asia-Pacific Float Glass Market significantly decreased in 2020.

Report Coverage

The report: “Asia-Pacific Float Glass Market – Forecast (2024-2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the Asia-Pacific Float Glass Market industry.

By Raw Materials: Silica Sand, Soda Ash, Limestone, Dolomite, Alumina, Glass Cullet, and Others (Chromite, Iron Oxide, Manganese, Feldspar, and Others).

By Glass Type: Basic Float Glass, Toughened Glass, Coated Glass, Laminated Glass, Extra Clear Glass, and Others (Wired Glass, and Mirrors).

By End-Use Industry: Building and Construction [Residential (Independent Houses, Row Houses, and Large Apartments), and Commercial (Office Buildings, Education Institutes, Hospitals, Hotels and Restaurants, Airports, Shopping Malls, Supermarkets and Hypermarkets, and Others)], Solar Energy, Transportation [Automotive (Passenger Vehicles, Light Commercial Vehicles, and Heavy Commercial Vehicles), Aerospace, Marine, and Locomotive], Consumer Goods, and Others.

By Country: China, Japan, India, South Korea, Australia and New Zealand, Indonesia, Taiwan, Malaysia, Thailand, Philippines, Vietnam, and Rest of Asia-Pacific.

Key Takeaways

• China dominates the Asia-Pacific Float Glass Market. Increased construction, automobile, solar, and electronics industries is boosting the float glass market growth in the country.

• The production of automobiles has increased steadily in the recent past and is expected to further increase in the coming years in the Asia-Pacific region, owing to the increasing disposable income of people, which is expected to fuel the demand for float glass.

• Furthermore, growth opportunities exist for the Asia-Pacific Float Glass Market as there have been growing government initiatives and investments in the construction industry and solar energy industry, which is spurring the overall market growth.

For More Details on This Report - Request for Sample

Asia-Pacific Float Glass Market Segment Analysis – By Raw Material

The silica sand segment held the largest share of more than 35% by revenue in the Asia-Pacific Float Glass Market in 2023 and is estimated to grow at a CAGR of 6.3% during 2024-2030, as it is considered as one of the most vital raw materials for the production of float glass when compared with other raw materials. Silica sand is the primary component in all types of standards and specialty glass because it provides the necessary Silicon Dioxide (SiO2) for glass formulation. The importance of raw material quality in float glass manufacturing is magnified since it affects critical elements of the finished products, such as the thickness, transparency, strength, and durability of the glass. For instance, the products manufactured with high-quality silica sand can meet the optimal vision requirements (i.e. light and thermal transmittance specifications) set for the automotive glasses and building glasses, without compromising with durability and safety of consumers. Thus, owing to the vital role of silica sand in producing float glass, there will be an increase in its demand during the forecast period.

Asia-Pacific Float Glass Market Segment Analysis – By Glass Type

The coated glass segment held the largest share in the Asia-Pacific Float Glass Market in 2023 and is estimated to grow at a CAGR of 7.1% during 2024-2030, owing to the various advantages associated with coated glass such as a higher level of comfort, cost-effective, better thermal performance, high level of energy efficiency, and more. Coated glass is an industrial glass product that has thin coatings of metal oxides (0.01 m to 0.8 m) sprayed on it. As a result, the coating is made up of a stack of different types and thicknesses of sub-coatings. It changes the way the glass reacts to solar light in both visible and infrared spectrums. The majority of Low-E coated glass is made through sputter coating, which involves putting a specific coating on polished glass sheets. When an optical coating is applied to the surface of a lens, the anti-reflective coating reduces the reflection of an optical device. The coating is made up of a thin transparent film that produces two reflected waves, resulting in a double interface. The use of coated glass to meet the needs of the visible portion of the spectrum (380 to 780 nanometers), to improve the thermal and solar performance of float glass without changing the composition of the glass itself, and to change the surface characteristics of the glass has increased market growth. As a result of these advantages, production and demand for Asia-Pacific float glass are expected to increase during the forecast period.

Asia-Pacific Float Glass Market Segment Analysis – By End-Use Industry

The building and construction segment held the largest share in the Asia-Pacific Float Glass Market in 2023 and is estimated to grow at a CAGR of 6.2% during 2024-2030. The growing trend towards fascinating materials and rising demand for float glass as transparent glazing material in the building envelope, including windows in the external walls, is estimated to drive the Asia-Pacific Float Glass Market in the residential sector. The increasing use of laminated glass owing to its seamless safety solution, from entry doors and glass floors, to display cases and aquariums in residential buildings has even further raised the market growth. Currently, with the upsurge of new upcoming construction projects the Asia-Pacific Float Glass Market is estimated to see substantial growth in the forecast period. For instance, in September 2022, Mahindra Lifespaces Developers has acquired a 7.89-acre plot of land next to Kanakapura Road's Holiday Village Resort. Under its top residential housing component, which is a part of Mahindra Lifespaces, it wants to construct 5 lac square feet of carpet space. With such investments in the residential construction sector, the Asia-Pacific Float Glass Market is also estimated to experience an upsurge in the upcoming years.

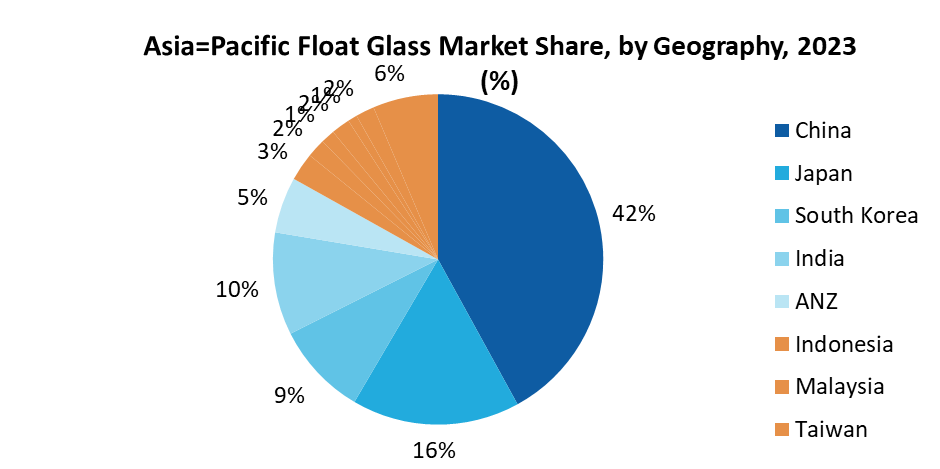

Asia-Pacific Float Glass Market Segment Analysis – By Country

China held the largest share in the Asia-Pacific Float Glass Market in 2023 up to 62.5% by revenue. Major growing industries in China include construction, solar power, automotive, and electronics. With the growth of these industries, the market for Asia-Pacific Float Glass is expected to grow further in the region. China is the largest manufacturer and installer of solar photovoltaic power systems in the world. In the country’s 14th Five-Year Plan (FYP) China is planning to expand its solar installations. In September 2023, As the second-largest economy in the world continues to increase its investments in renewable energy, China's installed solar capacity is expected to double to 1,000 gigawatts (GW) by the end of 2026. China is the largest producer & exporter of Consumer Electronics in the world. China’s consumer electronics production held the largest market share for its electronics exports in 2023. Therefore, the demand for float glass is increasing in the country, owing to the rising automotive, solar, and electronics industries.

Asia-Pacific Float Glass Market Drivers

Bolstering Automotive Industry

Automobiles use processed float glass that undergoes heating and chemical treatments (i.e toughened glass). The glass becomes tougher and stronger as a result of this toughening process, allowing it to withstand external stress. Float glass also offers beneficial properties such as protection against harmful infrared rays, prevention of excessive heating in the car, and reduction of noise. All these properties can be inculcated in the glass for optimum comfort while driving the vehicle. In the automotive industry, it is used for installations in the side, roof, window panels, and more. The demand for automotive is thriving in the Asia-Pacific countries. For instance, according to the European Automobile Manufacturers Association, in 2022, 85.4 million motor vehicles were produced globally in 2022, a 5.7% increase from 2021. The automotive glass will be in higher demand as the demand for automobiles and their aftermarket applications grows. This factor will significantly boost the overall demand for automotive glass and drive the growth of the float glass market in the Asia-Pacific countries.

Accelerating Solar Energy Industry

Most photovoltaic modules use float glass cover plates to provide structural strength to the PV module and to encapsulate the cells. Float glass is frequently used as the device's substrate (or superstrate) in thin-film solar systems. In reality, float glass is the single greatest component by mass in the majority of solar modules currently in production. The solar industry’s demand for glass is currently less than the overall market. However, with the huge growth in the solar industry, this situation is changing. The solar industry is growing in Asia-Pacific. For instance, according to the International Renewable Energy Agency (IRENA), approximately 63% of PV employment globally was accounted for by China, the world's largest installation market and top producer of PV equipment. With the projected growth in photovoltaics in the Asia-Pacific region, the demand for float glass for the solar industry will far exceed the current supply, and various new float-glass plants will have to be built to meet its needs over the next 20 years. Such expansion will drive the Asia-Pacific Float Glass Market.

Asia-Pacific Float Glass Market Challenges

Increase in Raw Material Prices

In recent times there has been an increase in the prices of raw materials that are used for float glass manufacturing such as soda ash, iron oxide, limestone, feldspar, and more, owing to which there is an increase in the price of float glass as well. The naturally forming soda ash is mined from an ore called trona. Excess use of trona is bounding the manufacturing opportunities of soda ash. Exhaustion of natural resources on earth is distressing the mineral ore - trona. As trona ore is getting depleted continuously, it affects the manufacturing process of soda ash and thus causing a rise in price for the process, thereby increasing the price of soda ash. Thus, the cost of raw materials is continuously increasing or fluctuating because of factors such as transportation & logistics, depletion of natural resources, and more, which is affecting the price of float glass as well. Hence, the volatility and increase in prices of float glass raw materials are expected to be a significant challenge for the float glass market manufacturers, which will hinder the market growth during the forecast period.

Cutting and Scheduling Problem in Float Glass Manufacturing

During float glass manufacturing the processing time to cut a rectangular unit of glass (called a plate) is proportional to its size. An offloading machine takes the same amount of time (regardless of size) to pick up, move, and release the glass to a container, then return. Thus, some slashed glass cannot be picked up before it gets to the end of the conveyor because the offloading machines are all busy and henceforth some glass is wasted. This wasted glass is called scrap. This means that even if there isn't an offloading machine to pick up the glass, it will still be made and thrown away as scrap. The challenge of eliminating wasted glass in float glass manufacturing is a complex optimization problem that requires simultaneous consideration of cutting and sequencing. Because of the limitations of the glass-making process and the equipment involved, there are several operational restrictions, which is acting as restrain for the float glass market.

Asia-Pacific Float Glass Market Landscape

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the Asia-Pacific Float Glass Market. Major players in the Asia-Pacific Float Glass Market are AGC Inc., China Glass Holdings Limited, Sejal Glass Ltd., Nippon Sheet Glass Co. Ltd., Xinyi Glass Holdings Co. Ltd., Kibing Group, Saint-Gobain Glass India, Jinjing Group, Gujarat Guardian Limited, and BG Float Glass Company Ltd.

Acquisitions/Technology Launches

• In May 2023, CTIEC establishes a new factory in Indonesia and leads the way in glass exports. After everything is finished, the facility's melting load for float glass sheets will be 1,200 metric tons per day.

• In March 2022, Saint-Gobain India opened three new locations with ₹500 crore in investment. A new float glass unit, an integrated windows line facility, and an urban forest were all part of the project.

For more Chemicals and Materials Market reports, please click here

1. Asia-Pacific Float Glass Market- Market Overview

1.1 Definitions and Scope

2. Asia-Pacific Float Glass Market- Executive Summary

2.1 Key Trends by Raw Materials

2.2 Key Trends by Glass Type

2.3 Key Trend by End-Use Industry

2.4 Key Trends by Country

3. Asia-Pacific Float Glass Market – Comparative analysis

3.1 Market Share Analysis- Major Companies

3.2 Product Benchmarking- Major Companies

3.3 Top 5 Financials Analysis

3.4 Patent Analysis- Major Companies

3.5 Pricing Analysis (ASPs will be provided)

4. Asia-Pacific Float Glass Market - Startup companies Scenario Premium Premium

4.1 Major startup company analysis:

4.1.1 Investment

4.1.2 Revenue

4.1.3 Product portfolio

4.1.4 Venture Capital and Funding Scenario

5. Asia-Pacific Float Glass Market – Industry Market Entry Scenario Premium Premium

5.1 Regulatory Framework Overview

5.2 New Business and Ease of Doing Business Index

5.3 Successful Venture Profiles

5.4 Customer Analysis – Major companies

6. Asia-Pacific Float Glass Market - Market Forces

6.1 Market Drivers

6.2 Market Constraints

6.3 Porters Five Force Model

6.3.1 Bargaining Power of Suppliers

6.3.2 Bargaining Powers of Buyers

6.3.3 Threat of New Entrants

6.3.4 Competitive Rivalry

6.3.5 Threat of Substitutes

7. Asia-Pacific Float Glass Market – Strategic Analysis

7.1 Value/Supply Chain Analysis

7.2 Opportunity Analysis

7.3 Product/Market Life Cycle

7.4 Distributor Analysis – Major Companies

8. Asia-Pacific Float Glass Market– By Raw Material (Market Size -US$ Million, KT)

8.1 Silica Sand

8.2 Soda Ash

8.3 Limestone

8.4 Dolomite

8.5 Alumina

8.6 Glass Cullet

8.7 Others

8.7.1 Chromite

8.7.2 Iron Oxide

8.7.3 Manganese

8.7.4 Feldspar

8.7.5 Others

9. Asia-Pacific Float Glass Market– By Glass Type (Market Size – US$ Million, KT)

9.1 Basic Float Glass

9.2 Toughened Glass

9.3 Coated Glass

9.4 Laminated Glass

9.5 Extra Clear Glass

9.6 Others

9.6.1 Wired Glass

9.6.2 Mirrors

10. Asia-Pacific Float Glass Market– By End-Use Industry (Market Size -US$ Million, KT)

10.1 Building and Construction

10.1.1 Residential

10.1.1.1 Independent Houses

10.1.1.2 Row Houses

10.1.1.3 Large Apartments

10.1.2 Commercial

10.1.2.1 Office Building

10.1.2.2 Education Institutes

10.1.2.3 Hospitals

10.1.2.4 Hotels and Restaurants

10.1.2.5 Airports

10.1.2.6 Shopping Malls

10.1.2.7 Supermarkets and Hypermarkets

10.1.2.8 Others

10.2 Solar Energy

10.3 Transportation

10.3.1 Automotive

10.3.1.1 Passenger Vehicles

10.3.1.2 Light Commercial Vehicles

10.3.1.3 Heavy Commercial Vehicles

10.3.2 Aerospace

10.3.3 Marine

10.3.4 Locomotive

10.4 Consumer Goods

10.5 Others

11. Asia-Pacific Float Glass Market - By Country (Market Size -US$ Million, KT)

11.1 China

11.2 Japan

11.3 India

11.4 South Korea

11.5 Australia and New Zealand

11.6 Indonesia

11.7 Taiwan

11.8 Malaysia

11.9 Thailand

11.10 Philippines

11.11 Vietnam

11.12 Rest of Asia-Pacific

12. Asia-Pacific Float Glass Market – Entropy

12.1 New Product Launches

12.2 M&As, Collaborations, JVs and Partnerships

13. Asia-Pacific Float Glass Market – Market Share Analysis Premium

13.1 Company Benchmarking Matrix – Major Companies

13.2 Market Share at Global Level - Major companies

13.3 Market Share by Key Region - Major companies

13.4 Market Share by Key Country - Major companies

13.5 Market Share by Key Application - Major companies

13.6 Market Share by Key Product Type/Product category - Major companies

14. Asia-Pacific Float Glass Market – Key Company List by Country Premium Premium

15. Asia-Pacific Float Glass Market Company Analysis - Business Overview, Product Portfolio, Financials, and Developments

15.1 AGC Inc.

15.2 China Glass Holdings Limited

15.3 Sejal Glass Ltd

15.4 Nippon Sheet Glass Co. Ltd.

15.5 Xinyi Glass Holdings Co. Ltd.

15.6 Kibing Group

15.7 Saint-Gobain Glass India

15.8 Jinjing Group

15.9 Gujarat Guardian Limited

15.10 BG Float Glass Company Ltd.

"*Financials would be provided on a best-efforts basis for private companies"