Email

Email Print

Print

Aircraft Engine Blades Market -By Blade Type, By Material, By Engine, By Manufacturing Process, By Application, By End User, By Geography - Opportunity Analysis & Industry Forecast, 2024-2030

Aircraft Engine Blades Market Overview:

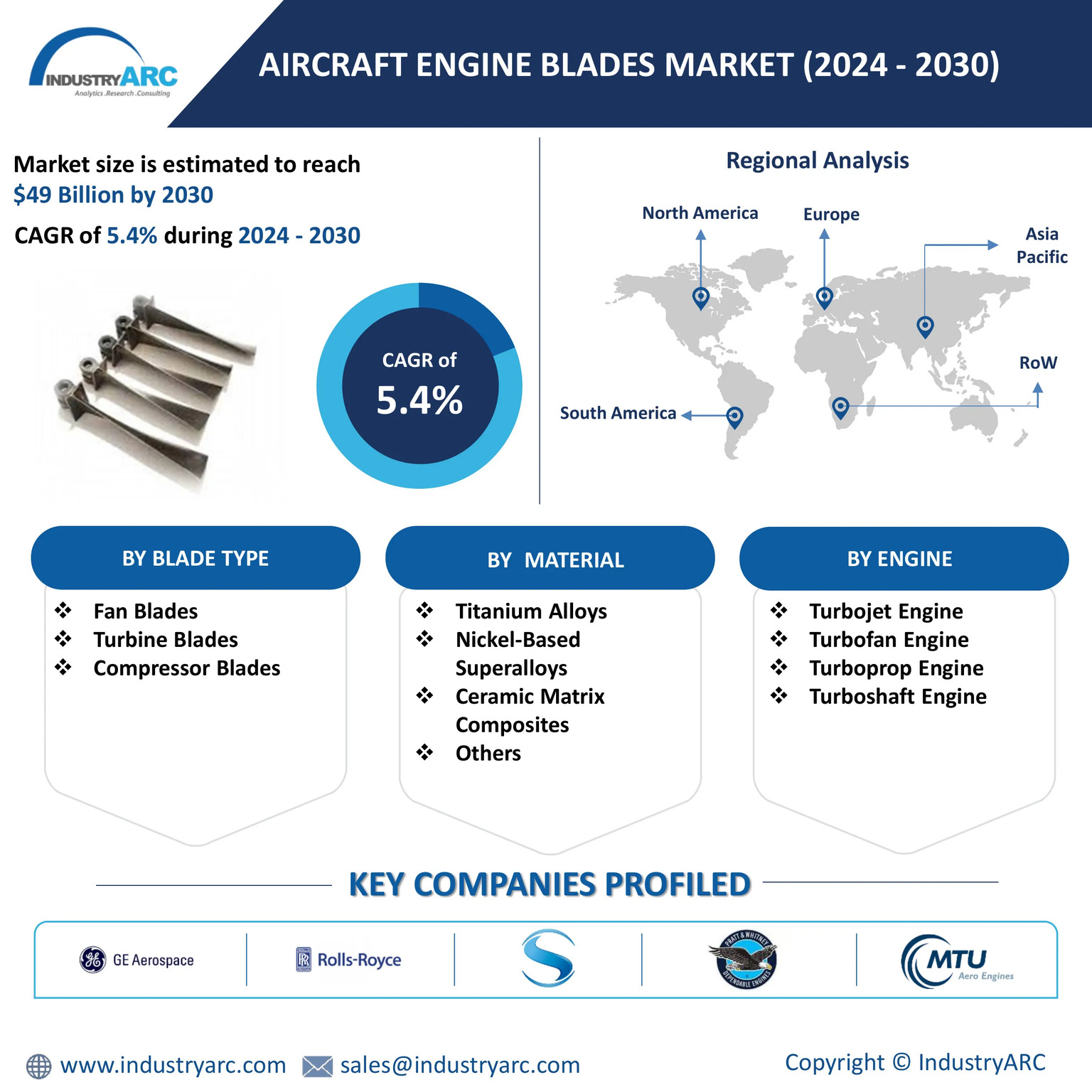

The Aircraft Engine Blades Market size is estimated to reach $49 Billion by 2030, growing at a CAGR of 5.4% during the forecast period 2024-2030. The market for aircraft engine blades is driven by several interlinked factors such as growing global demand for air travel, fleet expansion & replacement cycles and technological advancements are shaping both current dynamics and future growth opportunities. Additionally, modernization of fleet and development of more efficient engines is accelerating due to increasing pressure from governments and international regulatory organizations, such the International Civil Aviation Organization (ICAO), to reduce carbon emissions. Such factors are driving the growth of aircraft engine blades market.

The aircraft engine blade market is undergoing significant transformation, driven by advancements in materials. One of the most prominent trends in the aircraft engine blade market is the increasing adoption of advanced materials like Ceramic Matrix Composites (CMCs) and high-strength titanium alloys. According to composite world, GE Aerospace has increased CMC manufacturing to address the demand for more efficient engines in aviation. For instance, GE Aerospace using innovative silicon carbide (SiC/SiC) composites in the turbine shrouds of their LEAP engines, which has a 1,300°C tolerance. The LEAP engine's special set of characteristics has allowed it to run hotter with less cooling, increasing efficiency to burn 15-20% less fuel while lowering emissions and maintenance costs. These innovations are driven by the need to improve fuel efficiency, meet environmental regulations, and reduce operational costs.

Market Snapshot:

Aircraft Engine Blades Market - Report Coverage:

The “Aircraft Engine Blades Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Aircraft Engine Blades Market.

| Attribute | Segment |

|---|---|

|

By Blade Type |

|

|

By Material |

|

|

By Engine |

|

|

By Manufacturing Process |

|

|

By Application |

|

|

By End – User |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- COVID-19 caused major disruptions in the aerospace supply chain, with factory shutdowns, workforce shortages, and logistical challenges leading to delays in the production and delivery of aircraft engine components, including blades. Additionally, the International Civil Aviation Organization confirmed that international passenger traffic suffered a 60% drop over 2020. The recovery of air travel has been slow, with commercial air traffic still rebounding from pandemic upset.

- Russia-Ukraine had significant impacts on the global aircraft engine blades market, disrupting supply chains, demand patterns and operational strategies within the aerospace industry. The aerospace industry relies heavily on specific raw materials such as titanium which is essential for manufacturing aircraft engine blades due to its strength and heat resistance. Russia is one of the world’s leading producers of titanium, and the Ukraine crisis has led to sanctions and trade restrictions on Russian exports. This led to increase costs and creating shortages of critical materials used in aircraft blade production.

Key Takeaways:

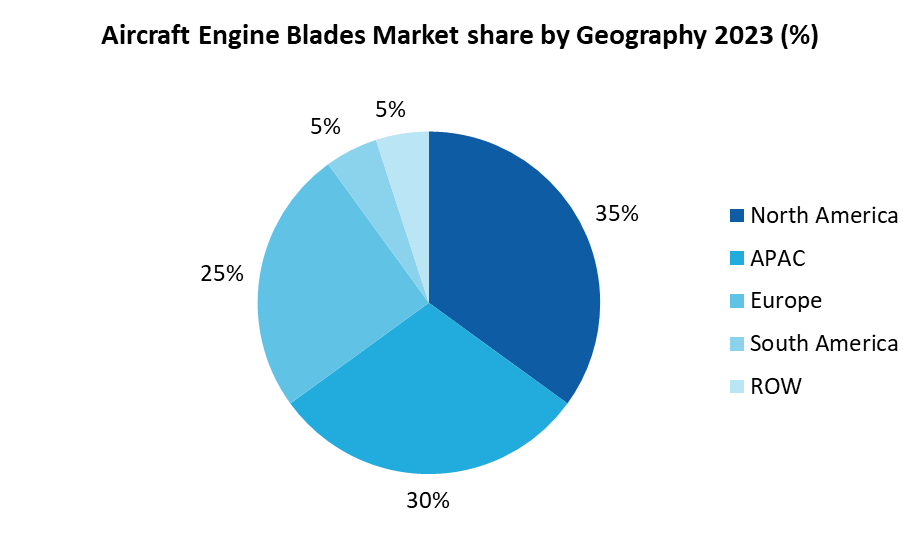

North America Dominates the Market

North America dominates the region in Aircraft Engine Blades Market with a market share of 35% during the forecast period 2024-2030. North America leads the world in aerospace manufacturing and innovation due to a number of important variables, including its supremacy in the market for aviation engine blades. The main factor for leadership is the presence of major aircraft and engine manufacturers like Boeing, GE Aviation, Pratt & Whitney, and Honeywell Aerospace. These companies are world leaders in the development and manufacture of aviation engines and components, such as high-performance engine blades. Their robust presence in the area ensures North America's continued status as a centre of aerospace research and manufacturing. The region's ability to advanced manufacturing and its investments in research and development are also very important. For instance, GE Aerospace spent $2.3 billion in research and development in 2023. Additionally, high-performance materials like composites and superalloys, which are necessary to produce strong and lightweight engine blades are expertly produced in the United States.

Turbine Blades are the Largest Segment

Turbine blades segment is projected as the fastest growing segment in Aircraft Engine Blades Market. Turbine blades referred as the heart of aircraft engines, which are an essential part of aircraft engines. They are regarded as an expensive component because of its complex design, modern production techniques, and ability to endure the high temperatures present in the engine's core. Because of this, turbine blades are more expensive than fan or compressor blades. Turbine blades' dominance in the aircraft engine blade market has been cemented by their high value and substantial demand. GE Aerospace announced plans to inject more than $650 million into its manufacturing facilities and supply chain during 2024 to improve production and strengthen quality to better support its commercial and defense customers. Such investments drive the aircraft engine blades market

Commercial Aviation is the Largest Application

Commercial aviation is the most significant application for aircraft engine blades. This dominance can be attributed to several key factors such as the vast fleets operated by commercial airlines create a consistently high demand for engine blades. Regular maintenance and replacements are essential to ensure the safety and efficiency of these aircraft. The steady growth of the global air travel industry has led to increased demand for commercial aircraft and their associated components, including engine blades. According to Airports Council International, the international passenger air traffic is anticipated to touch 4.1 billion or 43% by the end of 2024 and domestic passenger traffic projected to reach 5.4 billion by the end of 2024, making up 57% of the total. Commercial airlines regularly renew their fleets to maintain operational efficiency and meet evolving passenger demands, which further drives demand for new engines and blades. Therefore, combining these factors leads to rise in demand for commercial aviation which drives the demand for aircraft engine blades market.

Aircraft Modernization Efforts to Drive the Market

Aircraft modernization efforts act as a catalyst for the growth of the aircraft engine blades market. As airlines seek to replace older, less efficient aircraft with newer models, there is a corresponding increase in demand for new engines and their components, including blades. New aircraft model with more fuel efficient than old aircrafts leads to reduce operating cost for airlines with the help of technological advancement such as AI offers great support in efficient operation. Airlines are being urged to switch to more fuel-efficient aircraft because of stricter environmental rules, particularly those related to carbon emissions. Because they frequently include innovative innovations that increase fuel efficiency and lower emissions, these further fuels the desire for new engines and blades. The B737 MAX's new generation engine is called LEAP-1B. Maximum thrust at take-off is 28,000 lbf, and the fan diameter is 69 inches. This engine was developed to address the problem of decarbonizing air travel. It provides Boeing 737 MAX operators with improved fuel efficiency and CO2 emissions (15% lower1) and NOx emissions (up to 50% lower2). Therefore, modernized aircraft helps to meet with stricter environmental requirements by replacing aging fleets with next-generation aircraft which simultaneously drives the aircraft engine blades market.

Engine Failure to Hamper the Market

Engine failure poses a major challenge in the aircraft engine blades market, driven by factors like material fatigue, thermal stress, and damage from foreign object debris. According to SKY BRAY, foreign object damage can be estimated to cost the aerospace industry $4 billion a year. Blade failures, often caused by high temperatures, rotational speeds, and debris impacts, can lead to catastrophic engine malfunctions. Additionally, According to Flight Global, the grounding of the PW1000G-series engine had a significant impact on the aviation industry. By April 2024, more than 600 out of almost 2,000 GTF-powered jets were out of service. To counter the challenge of engine failures, manufacturers are focusing on predictive maintenance technologies and real-time monitoring systems. The impact of these failures is profound, both in terms of safety risks and economic costs. While advanced materials and technologies like predictive maintenance offer solutions, the industry continue to innovate and maintain rigorous standards to reduce engine blade failures and their cascading effects.

For more details on this report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Aircraft Engine Blades Market. The top 10 companies in this industry are listed below:

- GE Aerospace

- Rolls-Royce Holdings plc

- Safran Aircraft Engines

- Pratt & Whitney

- MTU Aero Engines AG

- CFM International

- IHI Corporation

- GKN Aerospace

- Honeywell Aerospace

- RTX

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

5.4% |

|

Market Size in 2030 |

$49 Billion |

|

Segments Covered |

By Blade Type, By Material, By Engine, By Manufacturing Process, By Application, By End- User and By Geography. |

|

Geographies Covered |

North America (U.S., Canada, and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

1. GE Aerospace 2. Rolls-Royce Holdings plc 3. Safran Aircraft Engines 4. Pratt & Whitney 5. MTU Aero Engines AG 6. CFM International 7. IHI Corporation 8. GKN Aerospace 9. Honeywell Aerospace 10. RTX |

For more Aerospace and Defense Market reports, please click here

LIST OF TABLES

1.Global MARKET SEGMENTATION Market 2023-2030 ($M)

1.1 Blade Type Market 2023-2030 ($M) - Global Industry Research

1.1.1 Compressor Blades Market 2023-2030 ($M)

1.1.2 Turbine Blades Market 2023-2030 ($M)

1.1.3 Fan Blades Market 2023-2030 ($M)

1.1.4 Commercial Market 2023-2030 ($M)

1.1.5 Military Market 2023-2030 ($M)

1.1.6 General Aviation Market 2023-2030 ($M)

1.2 Material Market 2023-2030 ($M) - Global Industry Research

1.2.1 Titanium Market 2023-2030 ($M)

1.2.2 Nickel Alloy Market 2023-2030 ($M)

1.2.3 Composites Market 2023-2030 ($M)

2.Global COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

3.Global MARKET SEGMENTATION Market 2023-2030 (Volume/Units)

3.1 Blade Type Market 2023-2030 (Volume/Units) - Global Industry Research

3.1.1 Compressor Blades Market 2023-2030 (Volume/Units)

3.1.2 Turbine Blades Market 2023-2030 (Volume/Units)

3.1.3 Fan Blades Market 2023-2030 (Volume/Units)

3.1.4 Commercial Market 2023-2030 (Volume/Units)

3.1.5 Military Market 2023-2030 (Volume/Units)

3.1.6 General Aviation Market 2023-2030 (Volume/Units)

3.2 Material Market 2023-2030 (Volume/Units) - Global Industry Research

3.2.1 Titanium Market 2023-2030 (Volume/Units)

3.2.2 Nickel Alloy Market 2023-2030 (Volume/Units)

3.2.3 Composites Market 2023-2030 (Volume/Units)

4.Global COMPETITIVE LANDSCAPE Market 2023-2030 (Volume/Units)

5.North America MARKET SEGMENTATION Market 2023-2030 ($M)

5.1 Blade Type Market 2023-2030 ($M) - Regional Industry Research

5.1.1 Compressor Blades Market 2023-2030 ($M)

5.1.2 Turbine Blades Market 2023-2030 ($M)

5.1.3 Fan Blades Market 2023-2030 ($M)

5.1.4 Commercial Market 2023-2030 ($M)

5.1.5 Military Market 2023-2030 ($M)

5.1.6 General Aviation Market 2023-2030 ($M)

5.2 Material Market 2023-2030 ($M) - Regional Industry Research

5.2.1 Titanium Market 2023-2030 ($M)

5.2.2 Nickel Alloy Market 2023-2030 ($M)

5.2.3 Composites Market 2023-2030 ($M)

6.North America COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

7.South America MARKET SEGMENTATION Market 2023-2030 ($M)

7.1 Blade Type Market 2023-2030 ($M) - Regional Industry Research

7.1.1 Compressor Blades Market 2023-2030 ($M)

7.1.2 Turbine Blades Market 2023-2030 ($M)

7.1.3 Fan Blades Market 2023-2030 ($M)

7.1.4 Commercial Market 2023-2030 ($M)

7.1.5 Military Market 2023-2030 ($M)

7.1.6 General Aviation Market 2023-2030 ($M)

7.2 Material Market 2023-2030 ($M) - Regional Industry Research

7.2.1 Titanium Market 2023-2030 ($M)

7.2.2 Nickel Alloy Market 2023-2030 ($M)

7.2.3 Composites Market 2023-2030 ($M)

8.South America COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

9.Europe MARKET SEGMENTATION Market 2023-2030 ($M)

9.1 Blade Type Market 2023-2030 ($M) - Regional Industry Research

9.1.1 Compressor Blades Market 2023-2030 ($M)

9.1.2 Turbine Blades Market 2023-2030 ($M)

9.1.3 Fan Blades Market 2023-2030 ($M)

9.1.4 Commercial Market 2023-2030 ($M)

9.1.5 Military Market 2023-2030 ($M)

9.1.6 General Aviation Market 2023-2030 ($M)

9.2 Material Market 2023-2030 ($M) - Regional Industry Research

9.2.1 Titanium Market 2023-2030 ($M)

9.2.2 Nickel Alloy Market 2023-2030 ($M)

9.2.3 Composites Market 2023-2030 ($M)

10.Europe COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

11.APAC MARKET SEGMENTATION Market 2023-2030 ($M)

11.1 Blade Type Market 2023-2030 ($M) - Regional Industry Research

11.1.1 Compressor Blades Market 2023-2030 ($M)

11.1.2 Turbine Blades Market 2023-2030 ($M)

11.1.3 Fan Blades Market 2023-2030 ($M)

11.1.4 Commercial Market 2023-2030 ($M)

11.1.5 Military Market 2023-2030 ($M)

11.1.6 General Aviation Market 2023-2030 ($M)

11.2 Material Market 2023-2030 ($M) - Regional Industry Research

11.2.1 Titanium Market 2023-2030 ($M)

11.2.2 Nickel Alloy Market 2023-2030 ($M)

11.2.3 Composites Market 2023-2030 ($M)

12.APAC COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

13.MENA MARKET SEGMENTATION Market 2023-2030 ($M)

13.1 Blade Type Market 2023-2030 ($M) - Regional Industry Research

13.1.1 Compressor Blades Market 2023-2030 ($M)

13.1.2 Turbine Blades Market 2023-2030 ($M)

13.1.3 Fan Blades Market 2023-2030 ($M)

13.1.4 Commercial Market 2023-2030 ($M)

13.1.5 Military Market 2023-2030 ($M)

13.1.6 General Aviation Market 2023-2030 ($M)

13.2 Material Market 2023-2030 ($M) - Regional Industry Research

13.2.1 Titanium Market 2023-2030 ($M)

13.2.2 Nickel Alloy Market 2023-2030 ($M)

13.2.3 Composites Market 2023-2030 ($M)

14.MENA COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

LIST OF FIGURES

1.US Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

2.Canada Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

3.Mexico Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

4.Brazil Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

5.Argentina Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

6.Peru Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

7.Colombia Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

8.Chile Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

9.Rest of South America Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

10.UK Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

11.Germany Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

12.France Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

13.Italy Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

14.Spain Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

15.Rest of Europe Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

16.China Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

17.India Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

18.Japan Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

19.South Korea Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

20.South Africa Aircraft Engine Blades Market Revenue, 2023-2030 ($M)

21.North America Aircraft Engine Blades By Application

22.South America Aircraft Engine Blades By Application

23.Europe Aircraft Engine Blades By Application

24.APAC Aircraft Engine Blades By Application

25.MENA Aircraft Engine Blades By Application

The Aircraft Engine Blades Market is projected to grow at 5.4% CAGR during the forecast period 2024-2030.

The Aircraft Engine Blades Market size is estimated to be $34.5 billion in 2023 and is projected to reach $49 Billion by 2030.

The leading players in the Aircraft Engine Blades Market are GE Aerospace, Rolls-Royce Holdings plc, Safran Aircraft Engines, Pratt & Whitney, MTU Aero Engines AG and others.

Adoption of Ceramic Matrix Composites (CMCs) and Advanced Alloys, Sustainability and Environmental Regulations, adoption of Additive Manufacturing (3D Printing) and Hybrid Electric and Sustainable Aviation Fuel (SAF)-Compatible Engines are the major trends that will shape the market in the future.

Rising demand for air travel and fleet expansion, technological advancements in engine efficiency and regional aircraft growth leads to the rise in demand for aircraft engine blades market.