Email

Email Print

Print

Autonomous Aircraft Market - By Autonomy Level , By Platform , By Payload Capacity , By Propulsion Type , By Range , By Fleet Type , By Type , By Application , By Geography - Opportunity Analysis & Industry Forecast, 2024-2030

Autonomous Aircraft Market Overview:

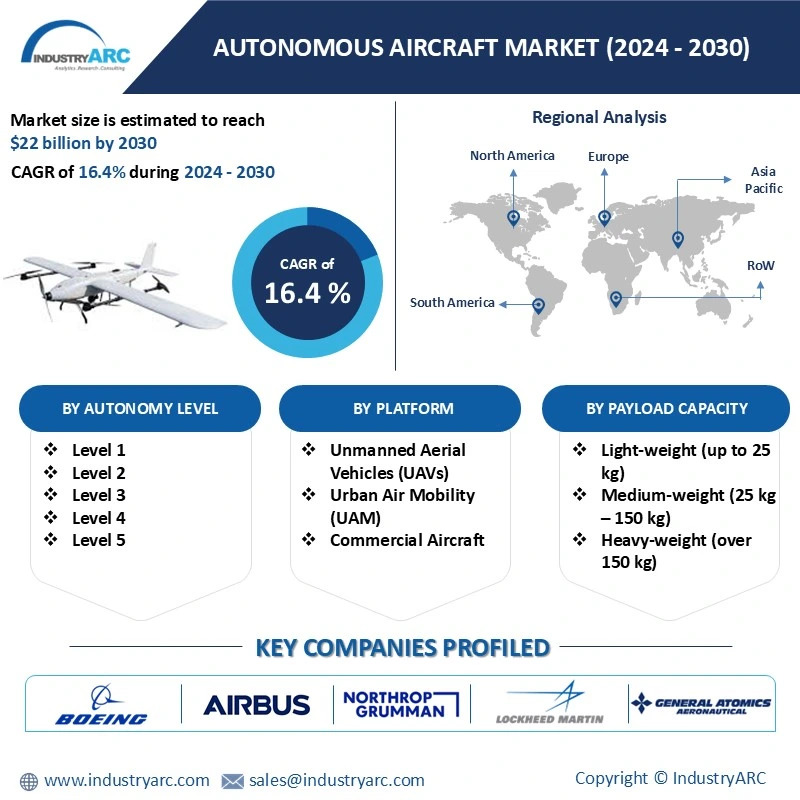

The Autonomous Aircraft Market size is estimated to reach $22 Billion by 2030, growing at a CAGR of 16.4% during the forecast period 2024-2030. Aviation is going to be entirely autonomous or highly automated by the 2040s, according to Honeywell Aerospace. A variety of crucial factors boosts the growth of the Autonomous Aircraft Market. Improvements in AI and machine learning along with sensors enable autonomous aircraft to function more securely and productively by minimizing human mistakes and improving flight routes. Increasing need for unmanned aerial vehicles (UAVs) in defense and logistics fields is fueling the market development since these aircraft handle essential duties without human assistance.

By cutting pilot expenses and enhancing fuel efficiency; autonomous aircraft offer attractive solutions for both commercial and express cargo operations. Urban air mobility (UAM) interests in city transport are producing fresh possibilities for autonomous passenger airplanes. Risky missions like reconnaissance and combat benefit from the military's increased reliance on autonomous aircraft which increases demand. Regulations and standardization initiatives simplify the process of adding autonomous aircraft to the national airspace. Logistics demand for quicker and more efficient delivery approaches drives their rapid use in the cargo market.

Market Snapshot:

Autonomous Aircraft Market - Report Coverage:

The “Autonomous Aircraft Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Autonomous Aircraft Market.

| Attribute | Segment |

|---|---|

|

By Autonomy Level |

· Level 1 · Level 2 · Level 3 · Level 4 · Level 5 |

|

By Platform |

· Unmanned Aerial Vehicles (UAVs) · Urban Air Mobility (UAM) · Commercial Aircraft |

|

By Payload Capacity |

· Light-weight (up to 25 kg) · Medium-weight (25 kg – 150 kg) · Heavy-weight (over 150 kg) |

|

By Propulsion Type |

· Electric · Hybrid · Conventional (Jet/Turbine) |

|

By Range |

· Short Range · Medium Range · Long Range |

|

Fleet Type |

· Commercial · Military & Defense · Civil: |

|

By Type |

· Fixed-Wing · Rotary-Wing · Hybrid Aircraft · Vertical Take-Off and Landing (VTOL) Aircraft · Others |

|

By Application |

· Cargo & Delivery · Surveillance & Monitoring · Passenger Transport · Agriculture · Military Operations · Others |

|

By Geography |

· North America (U.S., Canada and Mexico) · Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), · Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), · South America (Brazil, Argentina, Chile, Colombia and Rest of South America) · Rest of the World (Middle East and Africa). |

COVID-19 / Ukraine Crisis - Impact Analysis:

• The rise of Covid-19 halted progress on autonomous aircraft because of broken supply chains and a lack of funding for research. Production delays and a decline in global air travel demand caused a brief backward step in the sector. The pandemic sped up the adoption of autonomous systems in cargo delivery and oversight while companies investigated contactless methods to reduce human risks.

• The tensions between Russia and Ukraine boosted the requirement for cutting-edge defense technologies in the autonomous aircraft industry. As a result of the conflict there was increased interest in using autonomous military drones for gathering intelligence and executing attacks. The restrictions on Russian aviation companies blocked the access to vital components slowing down production. In several nations defense spending increased causing rapid demand for autonomous aircraft systems used in the military.

Key Takeaways:

North America Region is the Largest Region

The North American region dominates the Autonomous Aircraft Market due to the significant use of unmanned aerial systems by the US Department of Defense. For both training and overseas missions, the DoD operates over 11,000 unmanned aircraft including smaller models like the RQ-11B Raven and larger models weighing over 32,000 pounds like the RQ/MQ-4 Global Hawk. This technology is essential for genuine exercises and the assessment of devices for anticipated battle conditions. Numerous flight hours have been collected by the Department that significantly aid in developing safe operational practices for aviation. Furthermore, the DoD's emphasis on unmanned aircraft within all four military branches has further enhanced market growth. The extensive operations of North America enable it to become a forefront industry for autonomous aircraft technology.

Rotary Wing Aircrafts are Leading the Market

The market for autonomous aircraft is led by rotary-wing aircrafts for their exceptional adaptability and operational strengths. In contrast to fixed-wing aviation that needs substantial forward movement to rise off the ground, rotary-wing craft acquire lift from rotating blades enabling vertical takeoff and landing. Being able to hover significantly cuts down on flight times and permits these drones to perform in restricted spaces that fixed-wing aircraft find difficult. Those with rotorcraft can hold stationary position while maneuvering through small openings like windows to fulfil roles in urban areas like search and rescue or package transport. Due to their requirements for runways and landing areas fixed-wing aircraft are unsuitable for these operations. The ability of rotary-wing aircraft to hover and ascend without moving ahead allows for agility which renders them superior in multiple operational scenarios according to Shenzhen Grepow Battery Co., Ltd.

Military the Largest Market

The largest segment of the autonomous aircraft market is military operations fueled by rising requirements for advanced intelligence, surveillance, and reconnaissance (ISR) systems. Elistair made a formal announcement on January 2024 along with Rheinmetall Canada Inc. to improve military ISR technology. With the merger of Elistair’s KHRONOS tethered drone and Rheinmetall’s Mission Master UGVs military patrons gain advanced ISR capabilities. This equipment maintains constant monitoring throughout the day making soldier security more secure by cutting down human involvement in risky scenarios. Due to their capacity for longer flights these drones excel in areas of high risk such as nighttime operations or challenging landscapes providing round-the-clock visibility and essential observation. The effectiveness and dependability of this technology greatly strengthen the function of autonomous aircraft as vital assets in today's military missions.

Technological Advancements

The growth of unmanned aircraft is being fueled by improvements in AI and machine learning technologies. By using AI technology, the Valkyrie XQ-58A illustrates the significant possibilities provided by these innovations. The Valkyrie showcases a critical advancement in leveraging AI to enlarge military assets by exceeding a range of 3000 miles at heights up to 45000 feet. Maintaining strategic dominance over China is a priority for nations like the U.S. as they invest in this latest innovation. Sikorsky teamed up with DARPA to show that AI can enhance safety and lessen the need for crew with the autonomous Black Hawk helicopters. These developments facilitate better and flexible planning for task execution particularly in challenging conditions. With military and commercial sectors enhancing investments in AI automation the autonomous aircraft sector stands to thrive as budgets for defense increase and demand for improved operation efficiency expands.

Ethical Concerns

The autonomous aircraft industry faces considerable challenges due to ethical concerns. As per the Royal Aeronautical Society, it becomes tough to define the moral standards in ambiguous circumstances because present regulations count on human participation in major choices. Autonomous aircraft depend on AI for choices rather than human pilots who make decisions based on experience and morals. Hardware and software reliability is examined in system safety analyses assuming human pilots are ready to react in urgent situations. While AI systems execute many duties efficiently the gap in regulations for handling ethical issues in urgent circumstances constitutes a serious hurdle. Developing a set of regulations that involves ethical thought in autonomous systems is vital for greater market uptake.

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Autonomous Aircraft Market. The top 10 companies in this industry are listed below:

1. Boeing

2. Airbus

3. Northrop Grumman

4. Lockheed Martin

5. General Atomics Aeronautical Systems

6. Elbit Systems

7. Thales Group

8. BAE Systems

9. RTX

10. SAAB

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

16.4% |

|

Market Size in 2030 |

$22 Billion |

|

Segments Covered |

By Autonomy Level, By Platform, By Payload Capacity, By Propulsion Type, By Range, By Fleet Type, By Type, By Application and By Geography |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

1. Boeing 2. Airbus 3. Northrop Grumman 4. Lockheed Martin 5. General Atomics Aeronautical Systems 6. Elbit Systems 7. Thales Group 8. BAE Systems 9. RTX 10. SAAB |

For more Automotive Market reports, please click here

1. Autonomous Aircraft Market - Overview

1.1. Definitions and Scope

2. Autonomous Aircraft Market - Executive Summary

2.1. Key trends by Autonomy Level

2.2. Key trends by Platform

2.3. Key trends by Payload Capacity

2.4. Key trends by Propulsion Type

2.5. Key trends by Range

2.6. Key trends by Fleet Type

2.7. Key trends by Type

2.8. Key trends by Application

2.9. Key trends by Geography

3. Autonomous Aircraft Market - Comparative Analysis

3.1. Company Benchmarking - Key Companies

3.2. Financial Analysis - Key Companies

3.3. Market Share Analysis - Key Companies

3.4. Patent Analysis

3.5. Pricing Analysis

4. Autonomous Aircraft Market - Start-up Companies Scenario

4.1. Key Start-up Company Analysis by

4.1.1. Investment & Revenue

4.1.2. Venture Capital and Funding Scenario

5. Autonomous Aircraft Market – Market Entry Scenario Premium

5.1. Regulatory Framework Overview

5.2. New Business and Ease of Doing Business Index

5.3. Case Studies of Successful Ventures

6. Autonomous Aircraft Market - Forces

6.1. Market Drivers

6.2. Market Constraints

6.3. Market Challenges

6.4. Porter's Five Force Model

6.4.1. Bargaining Power of Suppliers

6.4.2. Bargaining Powers of Customers

6.4.3. Threat of New Entrants

6.4.4. Rivalry Among Existing Players

6.4.5. Threat of Substitutes

7. Autonomous Aircraft Market – Strategic Analysis

7.1. Value Chain Analysis

7.2. Opportunities Analysis

7.3. Product Life Cycle/Market Life Cycle Analysis

7.4. Supplier/Distributor Analysis

8. Autonomous Aircraft Market – By Autonomy Level (Market Size – $Million/$Billion)

8.1. Level 1

8.2. Level 2

8.3. Level 3

8.4. Level 4

8.5. Level 5

9. Autonomous Aircraft Market – By Platform (Market Size – $Million/$Billion)

9.1. Unmanned Aerial Vehicles (UAVs)

9.2. Urban Air Mobility (UAM)

9.3. Commercial Aircraft

10. Autonomous Aircraft Market – By Payload Capacity (Market Size – $Million/$Billion)

10.1. Light-weight (up to 25 kg)

10.2. Medium-weight (25 kg – 150 kg)

10.3. Heavy-weight (over 150 kg)

11. Autonomous Aircraft Market – By Propulsion Type (Market Size – $Million/$Billion)

11.1. Electric

11.2. Hybrid

11.3. Conventional (Jet/Turbine)

12. Autonomous Aircraft Market – By Range (Market Size – $Million/$Billion)

12.1. Short Range

12.2. Medium Range

12.3. Long Range

13. Autonomous Aircraft Market – By Fleet Type (Market Size – $Million/$Billion)

13.1. Commercial:

13.1.1. Passenger

13.1.2. Cargo

13.2. Military & Defense

13.2.1. Surveillance and Reconnaissance

13.2.2. Combat Aircraft

13.2.3. Intelligence and Targeting

13.3. Civil

13.3.1. Emergency Services

13.3.2. Environmental Monitoring

13.4. Others

14. Autonomous Aircraft Market – By Type (Market Size – $Million/$Billion)

14.1. Fixed-Wing

14.2. Rotary-Wing

14.3. Hybrid Aircraft

14.4. Vertical Take-Off and Landing (VTOL) Aircraft

14.5. Others

15. Autonomous Aircraft Market – By Application (Market Size – $Million/$Billion)

15.1. Cargo & Delivery

15.2. Surveillance & Monitoring

15.3. Passenger Transport

15.4. Agriculture

15.5. Military Operations

15.6. Others

16. Autonomous Aircraft Market – by Geography (Market Size – $Million/$Billion)

16.1. North America

16.1.1. U.S

16.1.2. Canada

16.1.3. Mexico

16.2. Europe

16.2.1. Germany

16.2.2. France

16.2.3. UK

16.2.4. Italy

16.2.5. Spain

16.2.6. Russia

16.2.7. Rest of Europe

16.3. Asia-Pacific

16.3.1. China

16.3.2. Japan

16.3.3. South Korea

16.3.4. India

16.3.5. Australia & New Zealand

16.3.6. Rest of Asia-Pacific

16.4. South America

16.4.1. Brazil

16.4.2. Argentina

16.4.3. Chile

16.4.4. Colombia

16.4.5. Rest of South America

16.5. Rest of The World

16.5.1. Middle East

16.5.2. Africa

17. Autonomous Aircraft Market – Entropy

17.1. New product launches

17.2. M&A's, collaborations, JVs and partnerships

18. Autonomous Aircraft Market – Industry/Segment Competition Landscape

18.1. Market Share Analysis

18.1.1. Market Share by Global

18.1.2. Market Share by Region

18.1.3. Market Share by Country

19. Autonomous Aircraft Market – Key Company List by Country Premium

20. Autonomous Aircraft Market – Company Analysis

20.1. Boeing

20.2. Airbus

20.3. Northrop Grumman

20.4. Lockheed Martin

20.5. General Atomics Aeronautical Systems

20.6. Elbit Systems

20.7. Thales Group

20.8. BAE Systems

20.9. RTX

20.10 .SAAB

"Financials to the Private Companies would be provided on a best-effort basis."

Connect with our experts to get customized reports that best suit your requirements. Our

reports include global-level data, niche markets, and competitive landscape.

LIST OF TABLES

1.Global MARKET SEGMENTATION Market 2023-2030 ($M)

1.1 Aircraft Type Market 2023-2030 ($M) - Global Industry Research

1.1.1 Fixed-wing Market 2023-2030 ($M)

1.1.2 Rotary-wing Market 2023-2030 ($M)

1.1.3 Cargo Aircraft Market 2023-2030 ($M)

1.1.4 Passenger Aircraft Market 2023-2030 ($M)

1.2 End User Market 2023-2030 ($M) - Global Industry Research

1.2.1 Commercial Market 2023-2030 ($M)

1.2.2 Defense Market 2023-2030 ($M)

2.Global COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

3.Global MARKET SEGMENTATION Market 2023-2030 (Volume/Units)

3.1 Aircraft Type Market 2023-2030 (Volume/Units) - Global Industry Research

3.1.1 Fixed-wing Market 2023-2030 (Volume/Units)

3.1.2 Rotary-wing Market 2023-2030 (Volume/Units)

3.1.3 Cargo Aircraft Market 2023-2030 (Volume/Units)

3.1.4 Passenger Aircraft Market 2023-2030 (Volume/Units)

3.2 End User Market 2023-2030 (Volume/Units) - Global Industry Research

3.2.1 Commercial Market 2023-2030 (Volume/Units)

3.2.2 Defense Market 2023-2030 (Volume/Units)

4.Global COMPETITIVE LANDSCAPE Market 2023-2030 (Volume/Units)

5.North America MARKET SEGMENTATION Market 2023-2030 ($M)

5.1 Aircraft Type Market 2023-2030 ($M) - Regional Industry Research

5.1.1 Fixed-wing Market 2023-2030 ($M)

5.1.2 Rotary-wing Market 2023-2030 ($M)

5.1.3 Cargo Aircraft Market 2023-2030 ($M)

5.1.4 Passenger Aircraft Market 2023-2030 ($M)

5.2 End User Market 2023-2030 ($M) - Regional Industry Research

5.2.1 Commercial Market 2023-2030 ($M)

5.2.2 Defense Market 2023-2030 ($M)

6.North America COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

7.South America MARKET SEGMENTATION Market 2023-2030 ($M)

7.1 Aircraft Type Market 2023-2030 ($M) - Regional Industry Research

7.1.1 Fixed-wing Market 2023-2030 ($M)

7.1.2 Rotary-wing Market 2023-2030 ($M)

7.1.3 Cargo Aircraft Market 2023-2030 ($M)

7.1.4 Passenger Aircraft Market 2023-2030 ($M)

7.2 End User Market 2023-2030 ($M) - Regional Industry Research

7.2.1 Commercial Market 2023-2030 ($M)

7.2.2 Defense Market 2023-2030 ($M)

8.South America COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

9.Europe MARKET SEGMENTATION Market 2023-2030 ($M)

9.1 Aircraft Type Market 2023-2030 ($M) - Regional Industry Research

9.1.1 Fixed-wing Market 2023-2030 ($M)

9.1.2 Rotary-wing Market 2023-2030 ($M)

9.1.3 Cargo Aircraft Market 2023-2030 ($M)

9.1.4 Passenger Aircraft Market 2023-2030 ($M)

9.2 End User Market 2023-2030 ($M) - Regional Industry Research

9.2.1 Commercial Market 2023-2030 ($M)

9.2.2 Defense Market 2023-2030 ($M)

10.Europe COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

11.APAC MARKET SEGMENTATION Market 2023-2030 ($M)

11.1 Aircraft Type Market 2023-2030 ($M) - Regional Industry Research

11.1.1 Fixed-wing Market 2023-2030 ($M)

11.1.2 Rotary-wing Market 2023-2030 ($M)

11.1.3 Cargo Aircraft Market 2023-2030 ($M)

11.1.4 Passenger Aircraft Market 2023-2030 ($M)

11.2 End User Market 2023-2030 ($M) - Regional Industry Research

11.2.1 Commercial Market 2023-2030 ($M)

11.2.2 Defense Market 2023-2030 ($M)

12.APAC COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

13.MENA MARKET SEGMENTATION Market 2023-2030 ($M)

13.1 Aircraft Type Market 2023-2030 ($M) - Regional Industry Research

13.1.1 Fixed-wing Market 2023-2030 ($M)

13.1.2 Rotary-wing Market 2023-2030 ($M)

13.1.3 Cargo Aircraft Market 2023-2030 ($M)

13.1.4 Passenger Aircraft Market 2023-2030 ($M)

13.2 End User Market 2023-2030 ($M) - Regional Industry Research

13.2.1 Commercial Market 2023-2030 ($M)

13.2.2 Defense Market 2023-2030 ($M)

14.MENA COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

LIST OF FIGURES

1.US Autonomous Aircraft Market Revenue, 2023-2030 ($M)

2.Canada Autonomous Aircraft Market Revenue, 2023-2030 ($M)

3.Mexico Autonomous Aircraft Market Revenue, 2023-2030 ($M)

4.Brazil Autonomous Aircraft Market Revenue, 2023-2030 ($M)

5.Argentina Autonomous Aircraft Market Revenue, 2023-2030 ($M)

6.Peru Autonomous Aircraft Market Revenue, 2023-2030 ($M)

7.Colombia Autonomous Aircraft Market Revenue, 2023-2030 ($M)

8.Chile Autonomous Aircraft Market Revenue, 2023-2030 ($M)

9.Rest of South America Autonomous Aircraft Market Revenue, 2023-2030 ($M)

10.UK Autonomous Aircraft Market Revenue, 2023-2030 ($M)

11.Germany Autonomous Aircraft Market Revenue, 2023-2030 ($M)

12.France Autonomous Aircraft Market Revenue, 2023-2030 ($M)

13.Italy Autonomous Aircraft Market Revenue, 2023-2030 ($M)

14.Spain Autonomous Aircraft Market Revenue, 2023-2030 ($M)

15.Rest of Europe Autonomous Aircraft Market Revenue, 2023-2030 ($M)

16.China Autonomous Aircraft Market Revenue, 2023-2030 ($M)

17.India Autonomous Aircraft Market Revenue, 2023-2030 ($M)

18.Japan Autonomous Aircraft Market Revenue, 2023-2030 ($M)

19.South Korea Autonomous Aircraft Market Revenue, 2023-2030 ($M)

20.South Africa Autonomous Aircraft Market Revenue, 2023-2030 ($M)

21.North America Autonomous Aircraft By Application

22.South America Autonomous Aircraft By Application

23.Europe Autonomous Aircraft By Application

24.APAC Autonomous Aircraft By Application

25.MENA Autonomous Aircraft By Application

The Autonomous Aircraft Market is projected to grow at 16.4% CAGR during the forecast period 2024-2030.

The Autonomous Aircraft Market size is estimated to be $22 Billion in 2023 and is projected to reach $22 Billion by 2030

The leading players in the Autonomous Aircraft Market are Boeing, Airbus, Northrop Grumman, Lockheed Martin, General Atomics Aeronautical Systems and Others.