Email

Email Print

Print

Chemical Seed Treatment Market- By Chemical Type , By Crop Type , By Technique , By Form , By Functionality and By Geography - Opportunity Analysis & Industry Forecast, 2024-2030.

Chemical Seed Treatment Market Overview:

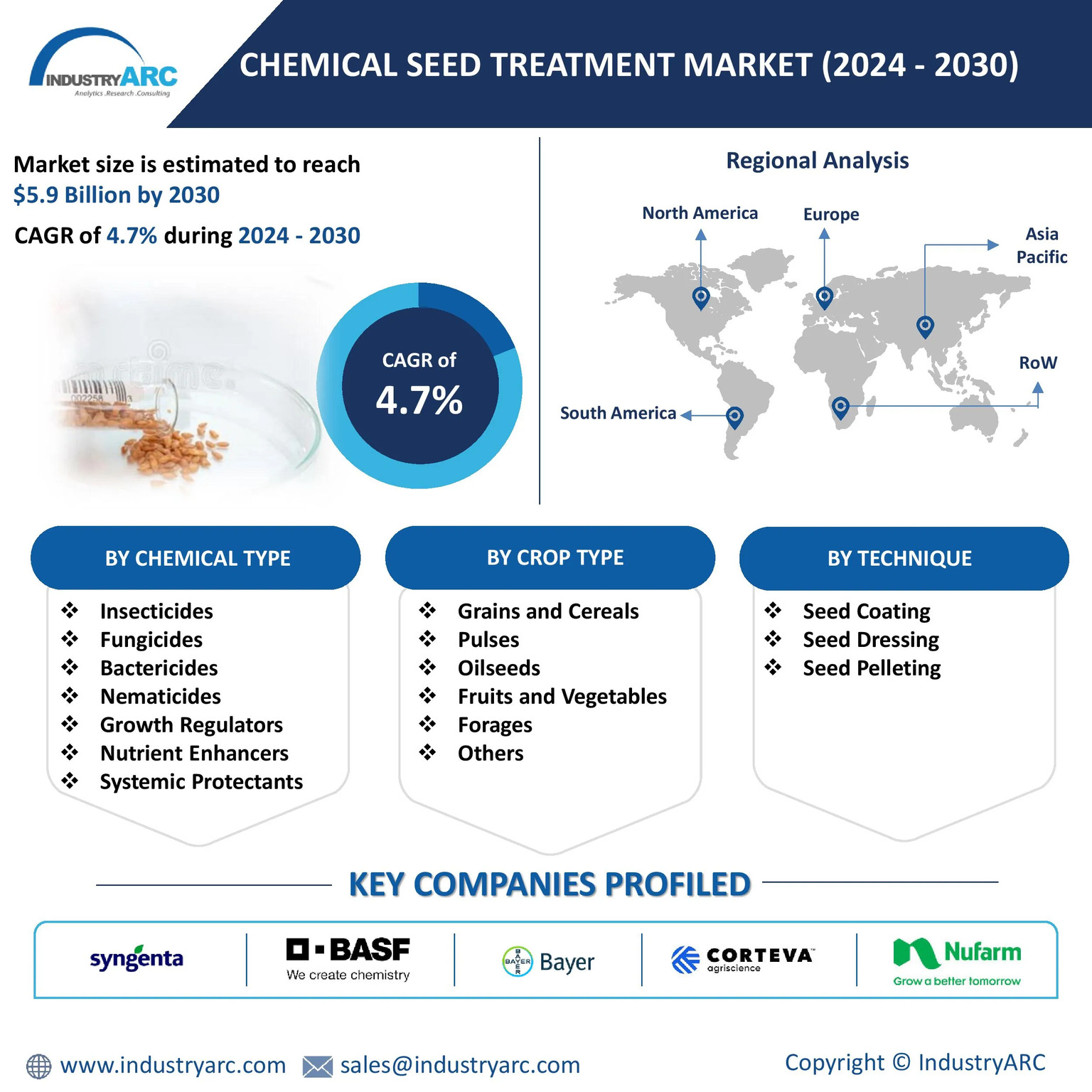

The Chemical Seed Treatment Market size is estimated to reach $5.9 Billion by 2030, growing at a CAGR of 4.7% during the forecast period 2024-2030. Chemical seed treatment is vital for today’s agriculture because it helps protect crops from pests or diseases, can boost germination rates, strengthen seedlings, and ultimately increase crop yields. The growing need for food security, rising incidences of pest attacks and the need for effective agricultural solutions amid changing climatic conditions are driving the market growth. As the global population grows, the demand for food rises, prompting farmers to enhance crop yields through effective solutions. Changing climate conditions foster environments that are conducive to pests and diseases like seed-borne and soil-borne diseases, and the cross-border movement of crops amplifies these threats, highlighting the urgent need for effective seed treatment measures to secure food production and preventing significant crop losses.

Innovations like nano-enabled seed treatments are transforming the chemical seed treatment market by enhancing the delivery and effectiveness of active ingredients. Nanotechnology allows for the development of smaller particles that can penetrate seed coatings more efficiently, ensuring a more uniform distribution of protective agents. This targeted application improves protection against pests and diseases while reducing the amount of chemical needed, minimizing environmental impact. The rise of precision agriculture and data analytics is revolutionizing the chemical seed treatment market by enabling farmers to optimize their applications based on specific field conditions and pest pressures. By utilizing advanced technology, such as soil sensors and satellite imagery, farmers can make informed decisions about when and how much seed treatment to apply.

Market Snapshot:

Chemical Seed Treatment Market- Report Coverage:

The “Chemical Seed Treatment Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Chemical Seed Treatment Market.

| Attribute | Segment |

|---|---|

|

By Chemical Type |

|

|

By Crop Type |

|

|

By Technique |

|

|

By Form |

|

|

By Functionality |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

Due to Covid-19, Farmers increasingly sought resilient crops, driving demand for advanced seed treatments that offer protection against diseases and pests. Economic pressures made many farmers more cost-conscious, prioritizing investments in effective treatments that ensure higher yields. In some regions, government support and subsidies for agricultural inputs helped stabilize food production. The pandemic also highlighted vulnerabilities in global supply chains, prompting a shift towards local sourcing of agricultural inputs and enhanced collaboration between farmers and local producers.

During Russia-Ukraine war, geopolitical instability created uncertainty in agricultural markets, leading farmers to adopt cautious approaches regarding input purchases. Export restrictions imposed by some countries have exacerbated supply constraints and price volatility. The conflict may also prompt shifts in trade alliances, affecting the flow of agricultural products and inputs.

Key Takeaways:

-

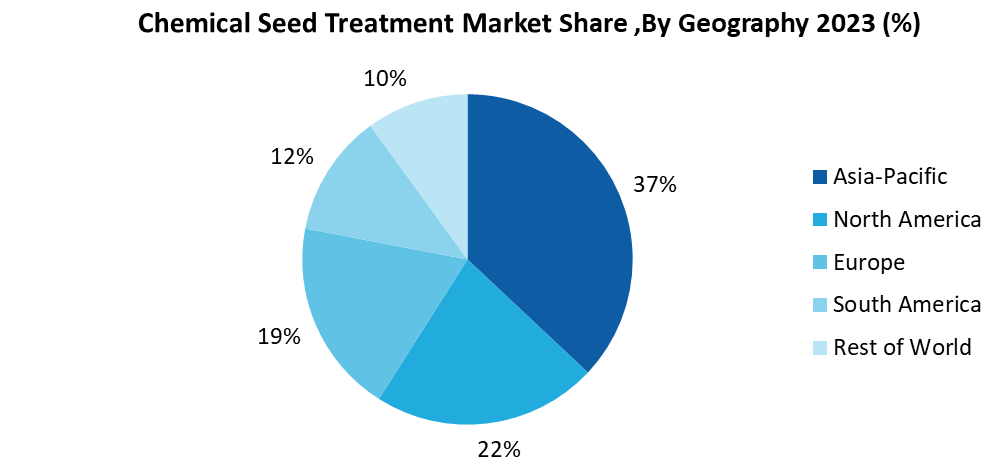

Asia-Pacific Region is Projected as Fastest Growing Region

The growth of the chemical seed treatment market in Asia-Pacific is significantly driven by the strong performances of its two largest markets, China and India. Both countries are experiencing robust agricultural expansion, largely fueled by high pesticide exports and effective crop protection solutions. China is the world’s leading producer and exporter of pesticides, with nearly 85% of its output sent to over 180 countries during peak years. According to August 2024 data from AgNews, China's pesticide exports reached $210 billion in the second quarter of 2024, with an export volume of 762,800 tons. Similarly, as per November 2023, India’s agrochemical exports hit a record US$ 5.5 billion for the financial year 2022-23, positioning the country as the second-largest agrochemical exporter globally. With government support for agrochemical projects, India aims to reach US$ 10 billion in exports over the next three years, indicating strong competitive potential. Indian producers are attracting global interest with their competitively priced generic agrochemicals, which boosts export volumes. The combination of affordability and high quality makes India an appealing destination for agrochemical manufacturing.

-

Seed Coating to Register the Fastest Growth

Seed Coating is anticipated to be the fastest-growing segment in the chemical seed treatment market primarily driven by the effectiveness of liquid and dry form. Its ease of application allows farmers to utilize various methods such as soaking, spraying, or coating, enhancing versatility and convenience. Seed Coating provide superior coverage and penetration, ensuring that active ingredients effectively protect seeds from pests and diseases. Among these, FS (Flowable Concentrate for Seed Treatment) formulations have gained popularity due to their concentrated nature and water-based composition, making them safer to apply. For example, Xelora, a systemic fungicide, features this unique FS formulation, delivering effective protection while being user-friendly for farmers.In addition to pest control, seed coating also trending dyes and pigments that are resistant to acids and alkalis, aiding in seed identification and quality assurance. These pigments boast high color strength, excellent dispersibility, and strong hiding power, enhancing the visual appeal of seeds while offering protection against harsh environmental conditions, thereby extending shelf life. BASF's Color Coat Liquid Seed Colorant, for instance, allows seed treaters to easily identify treated seeds, reflecting product quality and enabling growers to plant with confidence.

-

Fungicide Chemical is Leading the Market

Fungicides held the largest market share in 2023. Fungal pathogens represent a major threat to crops, leading to significant yield losses globally. Diseases such as powdery mildew, rust, and blight can severely damage crops if not properly managed. As per a article on Plant Production and Protection of Food and Agricultural organization, the widespread incidence of these diseases poses a serious risk to global crop yields, with potential losses reaching up to 40%. This creates a strong demand for fungicides to protect seeds and promote crop health. Their versatility allows for use across various crop types, including grains, fruits, and vegetables, thereby expanding their market reach. Fungicides can also be combined with other seed treatments, such as insecticides and fertilizers, to enhance overall seed protection and productivity. Additionally, continuous advancements in fungicide formulations, including systemic and multi-site action products, improve their effectiveness and longevity, making them vital for modern agriculture. Supportive regulations in many regions further encourage the use of fungicides, ensuring compliance with safety standards. For instance, in February 2024, Meristem announced a Gold Standard fungicide designed to combat Pythium and Phytophthora, presenting a potential alternative to traditional liquid seed treatments. The EPA has approved Meristem Crop Performance’s Metalaxyl ST fungicide, along with its biocontrol product Prephyte ST, as part of the Bio-Capsule Technology for efficient at-plant seed application.

-

Growing Need for Food Security

A January 2024 World Bank blog warns that short-term food insecurity could cause the number of people facing severe food insecurity to rise to 943 million by 2025, with projections reaching 956 million by 2028. This trend highlights the growing efficiency and productivity of agricultural practices, emphasizing the vital role of innovations like chemical seed treatments in enhancing crop yields. As farming practices become more intensive, the demand for effective solutions to address challenges from pests and diseases becomes increasingly urgent. Chemical seed treatments improve germination rates and seedling vigor, ultimately resulting in higher yields. Some chemical seeds are modified to increase the nutritional content of crops, addressing deficiencies in essential vitamins and minerals in various populations. This often involves leveraging advanced technologies and practices to maximize land use, including the application of chemical seed treatments to ensure robust and resilient crops. Farmers are increasingly turning to methods such as monoculture and high-input farming, which depend heavily on seed treatments for protection against pests, diseases, and environmental stressors. As agricultural systems intensify, the risk of pest and disease outbreaks rises, making chemical seed treatments a proactive strategy to mitigate these risks and enable farmers to operate with greater confidence.

-

Competition from Biological Alternatives

As awareness of sustainable farming practices grows, many farmers are exploring biological and organic methods to protect their crops, which can offer effective pest and disease management without the use of synthetic chemicals. Government regulations and consumer preferences increasingly favour environmentally friendly options, pushing agricultural producers to consider these non-chemical solutions. The negative effects of synthetic chemicals on soil health, water quality, and biodiversity are prompting a shift towards more sustainable agricultural practices. Also, public awareness of potential health risks associated with synthetic chemicals are leading farmers to adopt safer alternatives. Despite this urgency, regulatory bottlenecks and market resistance have hindered the widespread adoption of biopesticides in the UK. However, biopesticides offer an alternative that protects crops and aligns with the UK’s environmental and sustainability goals.These alternatives often include biopesticides, natural repellents, and integrated pest management (IPM) strategies that promote ecological balance. For example in April 2024, Bayer announced it aims to launch First Bioinsecticide expectedly in 2028 which will help farmers control pests in arable crops Also in January 2024, the Indian Institute of Spices Research (IISR) Kozhikode developed a new granular lime-based Trichoderma bio-pesticide for controlling a variety of soil-borne pathogens.

For more details on this report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Chemical Seed Treatment Market. The top 10 companies in this industry are listed below:

- Syngenta International AG

- BASF SE

- Bayer AG

- Corteva Agriscience

- NuFarm Ltd.

- Precision Laboratories

- FMC Corporation

- Croda Int. PLC

- Germains Seed Technology

- Valent Biosciences Corporation

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

4.7% |

|

Market Size in 2030 |

$5.9 Billion |

|

Segments Covered |

By Chemical Type, By Crop, By Technique, By Form, By Functionality and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, , Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

For more Agriculture Market reports, please click here

LIST OF TABLES

1.Global MARKET SEGMENTATION Market 2023-2030 ($M)

1.1 By Application Market 2023-2030 ($M) - Global Industry Research

1.1.1 Chemical Market 2023-2030 ($M)

1.2 By Crop Market 2023-2030 ($M) - Global Industry Research

1.2.1 Cornmaize Market 2023-2030 ($M)

1.2.2 Soybean Market 2023-2030 ($M)

1.2.3 Wheat Market 2023-2030 ($M)

1.2.4 Rice Market 2023-2030 ($M)

1.2.5 Canola Market 2023-2030 ($M)

1.2.6 Cotton Market 2023-2030 ($M)

2.Global MARKET SEGMENTATION Market 2023-2030 (Volume/Units)

2.1 By Application Market 2023-2030 (Volume/Units) - Global Industry Research

2.1.1 Chemical Market 2023-2030 (Volume/Units)

2.2 By Crop Market 2023-2030 (Volume/Units) - Global Industry Research

2.2.1 Cornmaize Market 2023-2030 (Volume/Units)

2.2.2 Soybean Market 2023-2030 (Volume/Units)

2.2.3 Wheat Market 2023-2030 (Volume/Units)

2.2.4 Rice Market 2023-2030 (Volume/Units)

2.2.5 Canola Market 2023-2030 (Volume/Units)

2.2.6 Cotton Market 2023-2030 (Volume/Units)

3.North America MARKET SEGMENTATION Market 2023-2030 ($M)

3.1 By Application Market 2023-2030 ($M) - Regional Industry Research

3.1.1 Chemical Market 2023-2030 ($M)

3.2 By Crop Market 2023-2030 ($M) - Regional Industry Research

3.2.1 Cornmaize Market 2023-2030 ($M)

3.2.2 Soybean Market 2023-2030 ($M)

3.2.3 Wheat Market 2023-2030 ($M)

3.2.4 Rice Market 2023-2030 ($M)

3.2.5 Canola Market 2023-2030 ($M)

3.2.6 Cotton Market 2023-2030 ($M)

4.South America MARKET SEGMENTATION Market 2023-2030 ($M)

4.1 By Application Market 2023-2030 ($M) - Regional Industry Research

4.1.1 Chemical Market 2023-2030 ($M)

4.2 By Crop Market 2023-2030 ($M) - Regional Industry Research

4.2.1 Cornmaize Market 2023-2030 ($M)

4.2.2 Soybean Market 2023-2030 ($M)

4.2.3 Wheat Market 2023-2030 ($M)

4.2.4 Rice Market 2023-2030 ($M)

4.2.5 Canola Market 2023-2030 ($M)

4.2.6 Cotton Market 2023-2030 ($M)

5.Europe MARKET SEGMENTATION Market 2023-2030 ($M)

5.1 By Application Market 2023-2030 ($M) - Regional Industry Research

5.1.1 Chemical Market 2023-2030 ($M)

5.2 By Crop Market 2023-2030 ($M) - Regional Industry Research

5.2.1 Cornmaize Market 2023-2030 ($M)

5.2.2 Soybean Market 2023-2030 ($M)

5.2.3 Wheat Market 2023-2030 ($M)

5.2.4 Rice Market 2023-2030 ($M)

5.2.5 Canola Market 2023-2030 ($M)

5.2.6 Cotton Market 2023-2030 ($M)

6.APAC MARKET SEGMENTATION Market 2023-2030 ($M)

6.1 By Application Market 2023-2030 ($M) - Regional Industry Research

6.1.1 Chemical Market 2023-2030 ($M)

6.2 By Crop Market 2023-2030 ($M) - Regional Industry Research

6.2.1 Cornmaize Market 2023-2030 ($M)

6.2.2 Soybean Market 2023-2030 ($M)

6.2.3 Wheat Market 2023-2030 ($M)

6.2.4 Rice Market 2023-2030 ($M)

6.2.5 Canola Market 2023-2030 ($M)

6.2.6 Cotton Market 2023-2030 ($M)

7.MENA MARKET SEGMENTATION Market 2023-2030 ($M)

7.1 By Application Market 2023-2030 ($M) - Regional Industry Research

7.1.1 Chemical Market 2023-2030 ($M)

7.2 By Crop Market 2023-2030 ($M) - Regional Industry Research

7.2.1 Cornmaize Market 2023-2030 ($M)

7.2.2 Soybean Market 2023-2030 ($M)

7.2.3 Wheat Market 2023-2030 ($M)

7.2.4 Rice Market 2023-2030 ($M)

7.2.5 Canola Market 2023-2030 ($M)

7.2.6 Cotton Market 2023-2030 ($M)

LIST OF FIGURES

1.US Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

2.Canada Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

3.Mexico Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

4.Brazil Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

5.Argentina Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

6.Peru Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

7.Colombia Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

8.Chile Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

9.Rest of South America Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

10.UK Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

11.Germany Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

12.France Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

13.Italy Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

14.Spain Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

15.Rest of Europe Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

16.China Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

17.India Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

18.Japan Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

19.South Korea Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

20.South Africa Chemical Seed Treatment Market Revenue, 2023-2030 ($M)

21.North America Chemical Seed Treatment By Application

22.South America Chemical Seed Treatment By Application

23.Europe Chemical Seed Treatment By Application

24.APAC Chemical Seed Treatment By Application

25.MENA Chemical Seed Treatment By Application

26.ADAMA AGRICULTURAL SOLUTIONS LTD, Sales /Revenue, 2015-2018 ($Mn/$Bn)

27.ADVANCED BIOLOGICAL MARKETING INC, Sales /Revenue, 2015-2018 ($Mn/$Bn)

28.BASF SE, Sales /Revenue, 2015-2018 ($Mn/$Bn)

29.BAYER CROPSCIENCE AG, Sales /Revenue, 2015-2018 ($Mn/$Bn)

30.BIOWORKS INC, Sales /Revenue, 2015-2018 ($Mn/$Bn)

31.BRETTYOUNG LIMITED, Sales /Revenue, 2015-2018 ($Mn/$Bn)

32.CHEMTURA AGROSOLUTIONS, Sales /Revenue, 2015-2018 ($Mn/$Bn)

33.DUPONT, Sales /Revenue, 2015-2018 ($Mn/$Bn)

34.INCOTEC GROUP BV, Sales /Revenue, 2015-2018 ($Mn/$Bn)

35.VERDESIAN LIFE SCIENCES, Sales /Revenue, 2015-2018 ($Mn/$Bn)

36.MONSANTO COMPANY, Sales /Revenue, 2015-2018 ($Mn/$Bn)

37.NOVOZYMES A/S, Sales /Revenue, 2015-2018 ($Mn/$Bn)

38.NUFARM LTD, Sales /Revenue, 2015-2018 ($Mn/$Bn)

39.PLANT HEALTH CARE, Sales /Revenue, 2015-2018 ($Mn/$Bn)

40.PRECISION LABORATORIES LLC, Sales /Revenue, 2015-2018 ($Mn/$Bn)

41.SYNGENTA INTERNATIONAL AG, Sales /Revenue, 2015-2018 ($Mn/$Bn)

42.VALENT USA CORPORATION, Sales /Revenue, 2015-2018 ($Mn/$Bn)

43.WOLF TRAX INC, Sales /Revenue, 2015-2018 ($Mn/$Bn)

The Chemical Seed Treatment Market is projected to grow at 4.7% CAGR during the forecast period 2024-2030.

The Chemical Seed Treatment Market size is estimated to be $4.5 million in 2023 and is projected to reach $5.9 billion by 2030.

The leading players in the Chemical Seed Treatment Market are Syngenta Group, BASF SE, Bayer AG, Corteva Agriscience and Others.

Globalization of Seed Trade, Technological Advancements, Digital Agriculture, Climate Resilience and investment in R&D are some of the major Chemical Seed Treatment Market trends in the industry which will create growth opportunities for the market during the forecast period.

Key driving factors include the rising prevalence of pests and diseases, and growing need for food security.