Email

Email Print

Print

Encapsulated Flavours Market – By Flavour Type, By Shell Material, By Release Mechanism, By Form, By Type, By Application, By Geography - Opportunity Analysis & Industry Forecast, 2024-2030

Encapsulated Flavours Market Overview:

The Encapsulated Flavours Market size is estimated to reach $4.9 Million by 2030, growing at a CAGR of 5.7% during the forecast period 2024-2030. Flavours encapsulation involves enclosing flavors in protective coatings to preserve their stability, enhance shelf life, and control release. This technology ensures flavors remain fresh until consumption, offering benefits like improved product longevity and better taste masking. The market is driven by the growing demand for processed and convenience foods, health and wellness trends favoring natural products, advancements in encapsulation technologies, and the expanding functional food sector, along with diverse consumer flavor preferences and a focus on sustainability.

A major trend in the Encapsulation Flavours Market is the growing demand for natural and clean-label ingredients. As consumers become more health-conscious, there is a significant push for products made with natural, non-artificial flavors. According to the International Food Information Council (IFIC), 62% of Americans check ingredient lists for transparency, driving companies to innovate encapsulation techniques that preserve the integrity of natural ingredients. Another key trend is technological advancements in encapsulation, such as microencapsulation and nanotechnology. Innovations like IFF’s FLAVORFIT™ tools, which help create better-tasting, healthier products, and Ingredion’s Q-NATURALE® emulsifier, which enhances flavor delivery while reducing costs, are making encapsulated flavors more effective and versatile in the market.

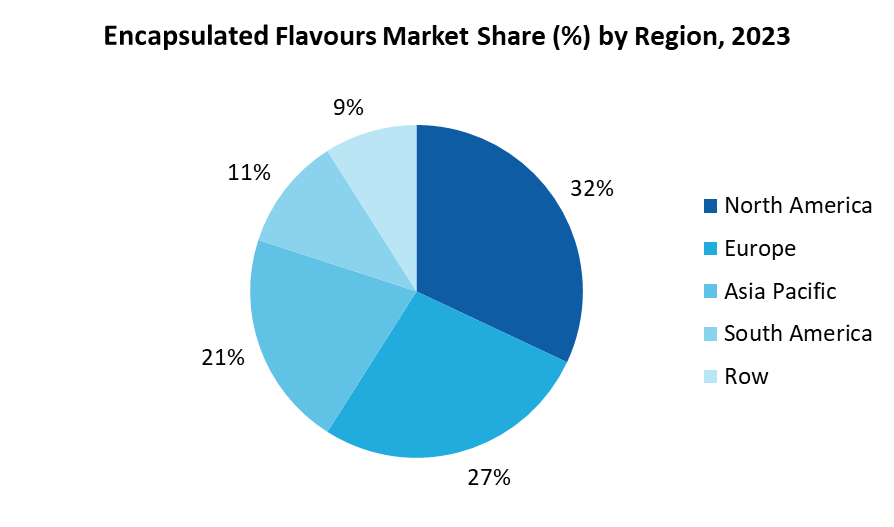

Market Snapshot:

Encapsulated Flavours Market - Report Coverage:

The “Encapsulated Flavours Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Encapsulated Flavours Market.

| Attribute | Segment |

|---|---|

|

Flavour Type |

· Citric Flavours · Berry Flavours · Spice Flavours · Nut Flavours · General Fruit Flavours · Exotic Fruit Flavours · Chocolate Flavour · Herbs and Botanicals · Others |

|

By Source |

· Natural Flavours · Artificial Flavours |

|

By Shell Material |

· Polysaccharides · Proteins · Lipids · Synthetic Polymers · Others |

|

By Release Mechanism |

· Immediate Release · Controlled Release · Triggered Release |

|

By Form |

· Powder · Liquid · Granules · Pastilles · Others |

|

By Type |

· Spray Drying · Spray Chilling · Fluid Bed Coating · Emulsification · Coacervation · Liposome Encapsulation · Others |

|

By Application |

· Food & Beverage · Pharmaceuticals · Cosmetics & Personal Care · Pet Food · Others |

|

By Geography |

· North America (U.S., Canada and Mexico) · Europe (Germany, France, UK, Italy, Spain, Netherlands, Denmark, Belgium and Rest of Europe), · Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand, Thailand, Malaysia, Indonesia and Rest of Asia-Pacific), · South America (Brazil, Argentina, Chile, Colombia and Rest of South America) · Rest of the World (Middle East and Africa). |

COVID-19 / Ukraine Crisis - Impact Analysis:

- The market for encapsulated flavors was disrupted by the COVID 19 Pandemic in sourcing of critical ingredients such as Emulsifiers and Coating Materials used during Encapsulation. Encapsulated flavors in food products saw temporary deficit due to shutdowns in production for factory. The shift toward processed and shelf storable foods during lockdowns created demand, which manufacturers responded to by favouring concentrated flavours in extended shelf-life foods.

- The encapsulated flavors market was directly hit by the Russia-Ukraine war, the region having been the source of sunflower oil and starch derivatives, the raw materials for which were unavailable during the war. This conflict created supply shortages which manufacturers resorted to using other raw materials sometimes at higher cost. Alongside these disruptions, the price of encapsulated flavors increased and production costs rose in the food and beverages industry, particularly in Europe.

Key Takeaways:

North America Region is Projected as Leading Region

North America is projected as the leading region in Encapsulated Flavours Market with CAGR of xx% during the forecast period 2024-2030. North America commands the largest share in the Encapsulation Flavours Market, driven by its robust food and beverage sector, which is a leader in adopting advanced flavor technologies. The region's focus on maintaining high standards of taste and quality in food products has led to the widespread use of encapsulation to preserve and enhance flavors, particularly in processed foods. This is significant given that approximately 60% of the American diet consists of processed foods, according to the Centers for Disease Control and Prevention (CDC). Encapsulation technology is essential in these products to ensure that flavors remain stable and appealing over extended shelf lives. Additionally, the consumer demand for convenience foods, coupled with a well-developed food processing industry, has further increased the adoption of encapsulated flavors in North America. According to the United States Securities and Exchange Commission (SEC), North America accounted for the largest share of 30.29% of the total sales in the International Flavors & Fragrances Inc. (IFF), which consists of 86 subsidiaries worldwide. 2023 Annual Sales Report, highlighting the region's leading role in the global flavor market.

Spray Drying is the Largest Segment

Spray drying is the most commonly used method in the encapsulated flavours market due to its flexibility, efficiency, and cost-effectiveness. According to the Indian Council of Agricultural Research, spray drying is a preferred microencapsulation technology in both the food and pharmaceutical industries because it is economical, scalable and capable of producing high-quality powder. Encapsulation, which involves enclosing active substances within a protective coating, is essential for shielding flavors from environmental factors like oxygen and moisture. Spray drying has been widely adopted for food production since the late 1950s, especially for encapsulating fats, oils, and flavourings. The process converts a liquid emulsion into powder form through rapid water evaporation in a hot drying chamber, typically at temperatures between 100–300 °C. This method is particularly effective for creating stable, high-quality particles, and it offers significant cost advantages over other techniques like freeze drying, with up to 30–50 times lower costs, as noted by the National Institutes of Health (NIH). Its ability to operate continuously and adapt to various formulations makes spray drying the most popular encapsulation method in the industry.

F&B are the Largest Application

The Food and Beverage industry is the largest segment by application in the Encapsulation Flavours Market, driven primarily by the critical role that taste plays in consumer preference. Flavors are essential for delivering the taste profiles that consumers expect, but these flavors can be compromised by evaporation or oxidation during production, transport, and storage, leading to a loss of intensity or an undesired change in taste. Encapsulation technology is crucial in this context as it effectively locks in and protects flavors, ensuring that the final product maintains its intended taste up until consumption. The growing global food industry, with its increasing demand for processed and convenience foods, further amplifies the need for such technology. According to the United States Securities and Exchange Commission (SEC), the Nourish segment, which includes a wide array of food-related products such as flavors, beverages, dairy products, and snacks, accounted for the largest share of 52.79% in the International Flavors & Fragrances Inc. 2023 Annual Sales Report. This significant share highlights the central role that encapsulated flavors play in the food and beverage industry, underscoring their importance in maintaining product quality and consumer satisfaction.

Health and Wellness Trends

Health and wellness trends are a major driver in the Encapsulation Flavours Market, as consumers increasingly seek food products that not only taste good but also align with their health-conscious lifestyles. Encapsulation technology plays a crucial role in this by enabling the inclusion of health-promoting ingredients like vitamins, probiotics, and plant-based extracts while maintaining their stability and flavor integrity. As the Food and Drug Administration (FDA) moves closer to updating the definition of "healthy" food, consumer expectations are evolving. According to the International Food Information Council (IFIC) 2023 Food & Health Survey, the most common attributes consumers associate with a healthy food are "fresh" (37%), "low in sugar" (32%), and "good source of protein" (29%). Encapsulation allows manufacturers to meet these demands by protecting sensitive ingredients and ensuring that health benefits are delivered without compromising on taste. As health and wellness trends continue to influence consumer behaviour, the demand for encapsulated flavors that support these attributes is expected to grow, further driving the market forward.

Balancing Flavor Stability and Sustainable Packaging

One of the major challenges in the Encapsulation Flavours Market is balancing flavor stability with the growing consumer demand for sustainable packaging. As consumers increasingly prefer products with minimal plastic and eco-friendly packaging, this shift poses a significant challenge for flavor stability. Encapsulated flavors are designed to protect delicate flavor compounds from environmental factors such as heat, light, and moisture, ensuring that the taste remains consistent throughout the product's shelf life. However, reducing or eliminating traditional protective packaging can expose these flavors to elements that could compromise their stability. According to Dsm-firmenich, a global leader in flavor and fragrance innovation, the consumer desire for less plastic and packaging, while beneficial for the environment, adds another layer of complexity for product developers who must find new ways to maintain flavor integrity. This challenge is compounded by the need to meet both sustainability goals and consumer expectations for high-quality, long-lasting flavors in a market where taste is a key driver of product success. Overcoming this hurdle requires ongoing innovation in encapsulation technologies to ensure flavors remain stable even as packaging becomes more environmentally friendly.

For more details on this report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Encapsulated Flavours Market. The top 10 companies in this industry are listed below:

- Cargill, Incorporated

- Kerry Group

- Givaudan

- Symrise AG

- Dsm-firmenich

- International Flavors & Fragrances (IFF)

- ScentSational Technologies

- Ingredion Incorporated

- Balchem Corporation

- Tate & Lyle PLC

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

5.7% |

|

Market Size in 2030 |

$4.9 Billion |

|

Segments Covered |

By Flavour Type, By Source, By Shell Material, By Release Mechanism, By Form, By Type, By Application and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Denmark, Netherlands, Belgium and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Thailand, Malaysia, and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa) |

|

Key Market Players |

2. Kerry Group 3. Givaudan 4. Symrise AG 6. International Flavors & Fragrances (IFF) 10. Tate & Lyle PLC |

For more Food and Beverage Market reports, please click here

The Encapsulated Flavours Market is projected to grow at 5.7% CAGR during the forecast period 2024-2030.

The Encapsulated Flavours Market size is estimated to be $3.32 billion in 2023 and is projected to reach $4.9 billion by 2030

The leading players in the Encapsulated Flavours Market are Cargill, Incorporated, Kerry Group, Givaudan, Symrise AG, Dsm-firmenich and Others.

Growing demand for natural and clean-label ingredients and advancements in encapsulation technologies for better flavor retention and controlled release are some of the major Encapsulated Flavours Market trends in the industry which will create growth opportunities for the market during the forecast period.

Increasing demand for processed and convenience foods, health and wellness trends favoring natural products, advancements in encapsulation technologies and the expanding functional food sector are the driving factors of the market.