Email

Email Print

Print

Evidence Management Market - Industry Analysis, Market, Size, Share, Trends, Application Analysis, Growth And Forecast 2024 - 2030

Evidence Management Overview:

The Evidence Management size is estimated to reach $15.1 billion by 2030, growing at a CAGR of 10.8% during the forecast period 2024-2030. Evidence management is the secure handling, storage and analysis of digital data. The growth of cloud-based solutions, demand for data security and encryption, digital transformation in law enforcement and legal sectors, increasing use of automation tools, rising crime rates and need for efficient investigations & strict regulatory compliance are contributing towards driving the market by providing the scalability, security, efficiency and automation of evidence workflows, assuring the integrity and accessibility of digital evidence.

Major trends in the Evidence Management market include growing use of wearable cameras, IoT sensors and drones for real-time evidence capture and management and blockchain for data integrity as these trends are highly transformative in terms of scalability and security. These technologies enable seamless collection, storage, and sharing of critical data, improving accuracy and efficiency in investigations. Wearable cameras provide on-the-ground perspectives, IoT sensors automate data gathering, and drones offer aerial insights, enhancing situational awareness. Together, they streamline evidence management, ensuring reliable and tamper-proof documentation while reducing manual errors. Moreover, blockchain technology ensures that the evidence can be followed all the way back to the custody of evidence, which is a pre-requisite to ensure evidence’s authenticity and integrity. This is to a decentralized nature, that ensures secure and transparent traceability to deter tampering and unauthorized changes. Together, these trends make for better efficiency, lower risks, and robust protection of digital evidence to drive the future of evidence management systems.

Market Snapshot:

Evidence Management Market - Report Coverage:

The “Evidence Management Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Evidence Management Market.

| Attribute | Segment |

|---|---|

|

By Type |

|

|

By Deployment Type |

|

|

By Organization Size |

|

|

By Service Model |

|

|

By Application |

|

|

By End-User Industry |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- Remote work and virtual legal processes during the COVID 19 pandemic accelerated ICT solutions adoption in the Evidence Management Market, as digital evidence was stored and shared on secure cloud platforms. As legal agencies and organizations began operating online there was a demand for scalable ICT infrastructure. It also made evidence processing more reliant on automation to make the process less manual.

- The Russia-Ukraine war made the Evidence Management Market more aware of the importance of cybersecurity. As cyberattacks and data breaches rose organizations prioritized advanced encryption and secure cloud solutions for digital evidence. The conflict pointed to a need for secure, real time ICT solutions to safeguard sensitive evidence and protect it from threats of cyber warfare and data tampering.

Key Takeaways:

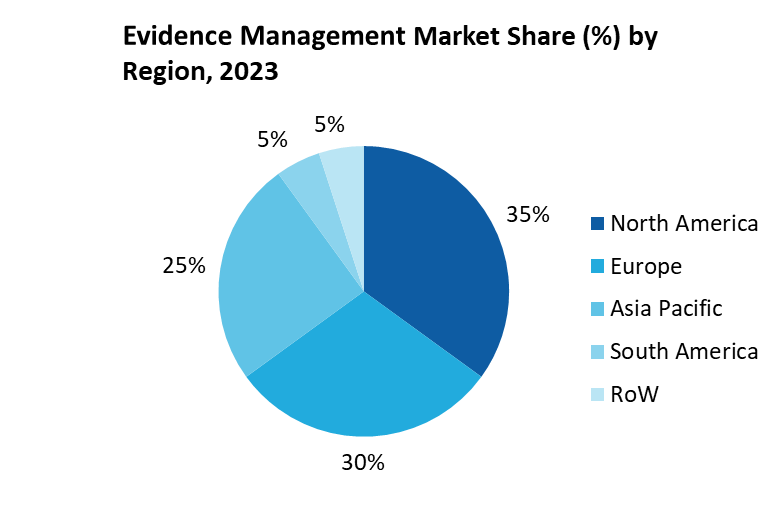

North America Leads the Market

North America dominated the market with the largest share in 2023. The Evidence Management Market is led by North America due to its proactive stance on technology adoption and regulatory framework to enhance security and efficiency. Robust guidelines for improving cloud security, namely by National Institute of Standards and Technology (NIST), is provided by government initiatives which are essential for evidence management in law enforcement and legal systems. These frameworks provide a safety guard that data is stored accessed, and managed securely. Politico states, The adoption of body-worn cameras (BWCs) has revolutionized the U.S. criminal justice system by enhancing transparency and fostering trust between law enforcement and communities. By improving evidence collection and clarifying use-of-force interactions, BWCs have strengthened relationships and accountability. As of 2020, all large police departments and 79% of officers nationwide in the U.S utilized BWCs, reflecting their pivotal role in modern policing. North America occupies a leading position in the evidence management solutions ICT sector owing to the focus on advanced security and compliance and significant investments in technology in the region.

Cloud is the Largest Segment

Cloud is the largest segment by deployment type in the Evidence Management Market, due to its widespread adoption, flexibility and cost efficiency. 96 % of businesses use at least one public cloud, and 50 % of workloads run on public cloud systems, according to Spacelift’s 2024 report. This extensive usage highlights how data and applications are increasingly being managed by cloud platforms. In addition, on average, organizations store 48 % of their data in these environments. With cloud infrastructure, businesses can process large volumes of digital evidence in a secure environment, comply with regulations,and have remote access to the data as well as easy integration with other ICT tools. Cloud solutions are the most affordable and easy to deploy compared to the private or hybrid models, making them the preferred choice for evidence management, especially for small and medium enterprises (SMEs) and large enterprises.

BFSI Leads the Market

The BFSI (Banking, Financial Services, and Insurance) sector plays a critical role in managing highly sensitive financial data, making it a prime target for cyberattacks, and is the largest segment in the Evidence Management Market by end-user industry. According to Elets BFSI, India’s financial sector alone faced over 1.3 million cyberattacks in 2023, highlighting its vulnerability to sophisticated threats like ransomware and phishing. The need for advanced evidence management solutions stems from this exposure, along with the BFSI sector’s reliance on cloud-based systems to store and manage large amounts of data to avoid breaches. The BFSI industry also operates under strict regulatory compliance, requiring robust evidence management systems to meet audit and legal obligations. According to the FBI and NakaTech, the BFSI sector’s increased risk profile and stringent regulatory environment have significantly driven up demand for Cloud Endpoint Protection and other security measures to safeguard critical data. As a result, the BFSI sector leads in adopting advanced evidence management solutions.

Rising Demand for Data Security and Encryption Boosts the Market

A key driver for the Evidence Management Market is the growing demand for data security and encryption as organizations with large volumes of sensitive digital data are exposed to growing risks from cyberattacks. Cloud-based storage and sharing of data systems have grown resulting in protecting vital information becoming the top priority. As per the World Economic Forum's Global Cybersecurity Outlook 2024, by 2025 cybercrime will cost $10.5 trillion annually. This highlights an urgent need for advanced encryption and data security measures. Organizations in sectors including finance, healthcare and government increasingly rely on digital systems to manage evidence and often sensitive data and so will need to adopt strong encryption tools to achieve the integrity and privacy of the data. Rising sophistication of cyber threats and the need to comply with strict regulations have made encryption a vital factor driving organizations to prioritize encryption and hence evidence management solutions.

Managing Large Volumes of Evidence to Hamper the Market

Managing large volumes of evidence has become a critical challenge in the evidence management market, driven by the exponential growth of digital data. According to Business Reporter, more than 2.5 quintillion bytes of data are generated daily, underscoring the increasing need for efficient storage and management solutions. This issue is particularly pronounced in policing, where over 80% of collected evidence is digital, including body camera footage, surveillance videos, and IoT sensor data. The sheer volume and diversity of this evidence strain existing systems, requiring advanced technologies to ensure secure, accessible, and organized storage. Inefficient management can lead to data loss, compromised evidence integrity, or delays in investigations. Additionally, compliance with stringent legal and privacy regulations further complicates the process. To address these challenges, law enforcement agencies must invest in scalable, cloud-based evidence management platforms capable of handling massive datasets while maintaining security, accessibility, and proper chain-of-custody protocols.

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Evidence Management. The top 10 companies in this industry are listed below:

1. Motorola Solutions, Inc

2. Genetec Inc.

3. OpenText

4. IBM Corporation

5. Palo Alto Networks

6. Oracle Corporation

7. Cisco Systems

8. Broadcom Inc.

9. Axon

10. SAP SE

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

10.8% |

|

Market Size in 2030 |

$15.1 billion |

|

Segments Covered |

By Type, By Deployment Type, By Organization Size, By Service Model, By Application, By End-User Industry and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

Relevant Reports:

Report Code: ITR 0134

Report Code: ITR 0409

Report Code: ITR 0177

1. Evidence Management Market - Overview 1.1 Definitions and Scope

2. Evidence Management Market - Executive summary

2.1 Market Revenue, Market Size and Key Trends by Company

2.2 Key Trends by type of Application

2.3 Key Trends segmented by Geography

3. Evidence Management Market

3.1 Comparative analysis

3.1.1 Product Benchmarking - Top 10 companies

3.1.2 Top 5 Financials Analysis

3.1.3 Market Value split by Top 10 companies

3.1.4 Patent Analysis - Top 10 companies

3.1.5 Pricing Analysis

4. Evidence Management Market - Startup companies Scenario Premium

4.1 Top 10 startup company Analysis by

4.1.1 Investment

4.1.2 Revenue

4.1.3 Market Shares

4.1.4 Market Size and Application Analysis

4.1.5 Venture Capital and Funding Scenario

5. Evidence Management Market - Industry Market Entry Scenario Premium

5.1 Regulatory Framework Overview

5.2 New Business and Ease of Doing business index

5.3 Case studies of successful ventures

5.4 Customer Analysis - Top 10 companies

6. Evidence Management Market Forces

6.1 Drivers

6.2 Constraints

6.3 Challenges

6.4 Porters five force model

6.4.1 Bargaining power of suppliers

6.4.2 Bargaining powers of customers

6.4.3 Threat of new entrants

6.4.4 Rivalry among existing players

6.4.5 Threat of substitutes

7. Evidence Management Market -Strategic analysis

7.1 Value chain analysis

7.2 Opportunities analysis

7.3 Product life cycle

7.4 Suppliers and distributors Market Share

8. Evidence Management Market - By Product Type(Market Size -$Million / $Billion)

8.1 Market Size and Market Share Analysis

8.2 Application Revenue and Trend Research

8.3 Product Segment Analysis

9. Evidence Management Market - By Type(Market Size -$Million / $Billion)

9.1 MARKET SEGMENTATION

9.1.1 By Deployment

9.1.1.1 On-Premise

9.1.1.2 Cloud

9.1.2 By Hardware

9.1.2.1 Body-Worn Camera

9.1.2.2 Vehicle Dash Camera

9.1.2.3 Citywide Camera

9.1.2.4 Public Transit Video

9.1.3 By Services

9.1.3.1 Consulting

9.1.3.2 Training

9.1.3.3 Support

9.2 COMPETITIVE LANDSCAPE

10. Evidence Management - By Application Type(Market Size -$Million / $Billion)

10.1 Segment type Size and Market Share Analysis

10.2 Application Revenue and Trends by type of Application

10.3 Application Segment Analysis by Type

11. Evidence Management- By Geography (Market Size -$Million / $Billion)

11.1 Evidence Management Market - North America Segment Research

11.2 North America Market Research (Million / $Billion)

11.2.1 Segment type Size and Market Size Analysis

11.2.2 Revenue and Trends

11.2.3 Application Revenue and Trends by type of Application

11.2.4 Company Revenue and Product Analysis

11.2.5 North America Product type and Application Market Size

11.2.5.1 U.S

11.2.5.2 Canada

11.2.5.3 Mexico

11.2.5.4 Rest of North America

11.3 Evidence Management- South America Segment Research

11.4 South America Market Research (Market Size -$Million / $Billion)

11.4.1 Segment type Size and Market Size Analysis

11.4.2 Revenue and Trends

11.4.3 Application Revenue and Trends by type of Application

11.4.4 Company Revenue and Product Analysis

11.4.5 South America Product type and Application Market Size

11.4.5.1 Brazil

11.4.5.2 Venezuela

11.4.5.3 Argentina

11.4.5.4 Ecuador

11.4.5.5 Peru

11.4.5.6 Colombia

11.4.5.7 Costa Rica

11.4.5.8 Rest of South America

11.5 Evidence Management- Europe Segment Research

11.6 Europe Market Research (Market Size -$Million / $Billion)

11.6.1 Segment type Size and Market Size Analysis

11.6.2 Revenue and Trends

11.6.3 Application Revenue and Trends by type of Application

11.6.4 Company Revenue and Product Analysis

11.6.5 Europe Segment Product type and Application Market Size

11.6.5.1 U.K

11.6.5.2 Germany

11.6.5.3 Italy

11.6.5.4 France

11.6.5.5 Netherlands

11.6.5.6 Belgium

11.6.5.7 Denmark

11.6.5.8 Spain

11.6.5.9 Rest of Europe

11.7 Evidence Management - APAC Segment Research

11.8 APAC Market Research (Market Size -$Million / $Billion)

11.8.1 Segment type Size and Market Size Analysis

11.8.2 Revenue and Trends

11.8.3 Application Revenue and Trends by type of Application

11.8.4 Company Revenue and Product Analysis

11.8.5 APAC Segment - Product type and Application Market Size

11.8.5.1 China

11.8.5.2 Australia

11.8.5.3 Japan

11.8.5.4 South Korea

11.8.5.5 India

11.8.5.6 Taiwan

11.8.5.7 Malaysia

11.8.5.8 Hong kong

11.8.5.9 Rest of APAC

11.9 Evidence Management - Middle East Segment and Africa Segment Research

11.10 Middle East & Africa Market Research (Market Size -$Million / $Billion)

11.10.1 Segment type Size and Market Size Analysis

11.10.2 Revenue and Trend Analysis

11.10.3 Application Revenue and Trends by type of Application

11.10.4 Company Revenue and Product Analysis

11.10.5 Middle East Segment Product type and Application Market Size

11.10.5.1 Israel

11.10.5.2 Saudi Arabia

11.10.5.3 UAE

11.10.6 Africa Segment Analysis

11.10.6.1 South Africa

11.10.6.2 Rest of Middle East & Africa

12. Evidence Management Market - Entropy

12.1 New product launches

12.2 M&A s, collaborations, JVs and partnerships

13. Evidence Management Market - Industry / Segment Competition landscape Premium

13.1 Market Share Analysis

13.1.1 Market Share by Country- Top companies

13.1.2 Market Share by Region- Top 10 companies

13.1.3 Market Share by type of Application - Top 10 companies

13.1.4 Market Share by type of Product / Product category- Top 10 companies

13.1.5 Market Share at global level - Top 10 companies

13.1.6 Best Practises for companies

14. Evidence Management Market - Key Company List by Country Premium

15. Evidence Management Market Company Analysis

15.1 Market Share, Company Revenue, Products, M&A, Developments

15.2 Company 2

15.3 Company 3 & More

16. Evidence Management Market - Appendix

16.1 Abbreviations

16.2 Sources

17. Evidence Management Market - Methodology

17.1 Research Methodology

17.1.1 Company Expert Interviews

17.1.2 Industry Databases

17.1.3 Associations

17.1.4 Company News

17.1.5 Company Annual Reports

17.1.6 Application Trends

17.1.7 New Products and Product database

17.1.8 Company Transcripts

17.1.9 R&D Trends

17.1.10 Key Opinion Leaders Interviews

17.1.11 Supply and Demand Trends

LIST OF TABLES

1.Global MARKET SEGMENTATION Market 2023-2030 ($M)

1.1 By Deployment Market 2023-2030 ($M) - Global Industry Research

1.1.1 On-Premise Market 2023-2030 ($M)

1.1.2 Cloud Market 2023-2030 ($M)

1.2 By Hardware Market 2023-2030 ($M) - Global Industry Research

1.2.1 Body-Worn Camera Market 2023-2030 ($M)

1.2.2 Vehicle Dash Camera Market 2023-2030 ($M)

1.2.3 Citywide Camera Market 2023-2030 ($M)

1.2.4 Public Transit Video Market 2023-2030 ($M)

1.3 By Services Market 2023-2030 ($M) - Global Industry Research

1.3.1 Consulting Market 2023-2030 ($M)

1.3.2 Training Market 2023-2030 ($M)

1.3.3 Support Market 2023-2030 ($M)

2.Global COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

3.Global MARKET SEGMENTATION Market 2023-2030 (Volume/Units)

3.1 By Deployment Market 2023-2030 (Volume/Units) - Global Industry Research

3.1.1 On-Premise Market 2023-2030 (Volume/Units)

3.1.2 Cloud Market 2023-2030 (Volume/Units)

3.2 By Hardware Market 2023-2030 (Volume/Units) - Global Industry Research

3.2.1 Body-Worn Camera Market 2023-2030 (Volume/Units)

3.2.2 Vehicle Dash Camera Market 2023-2030 (Volume/Units)

3.2.3 Citywide Camera Market 2023-2030 (Volume/Units)

3.2.4 Public Transit Video Market 2023-2030 (Volume/Units)

3.3 By Services Market 2023-2030 (Volume/Units) - Global Industry Research

3.3.1 Consulting Market 2023-2030 (Volume/Units)

3.3.2 Training Market 2023-2030 (Volume/Units)

3.3.3 Support Market 2023-2030 (Volume/Units)

4.Global COMPETITIVE LANDSCAPE Market 2023-2030 (Volume/Units)

5.North America MARKET SEGMENTATION Market 2023-2030 ($M)

5.1 By Deployment Market 2023-2030 ($M) - Regional Industry Research

5.1.1 On-Premise Market 2023-2030 ($M)

5.1.2 Cloud Market 2023-2030 ($M)

5.2 By Hardware Market 2023-2030 ($M) - Regional Industry Research

5.2.1 Body-Worn Camera Market 2023-2030 ($M)

5.2.2 Vehicle Dash Camera Market 2023-2030 ($M)

5.2.3 Citywide Camera Market 2023-2030 ($M)

5.2.4 Public Transit Video Market 2023-2030 ($M)

5.3 By Services Market 2023-2030 ($M) - Regional Industry Research

5.3.1 Consulting Market 2023-2030 ($M)

5.3.2 Training Market 2023-2030 ($M)

5.3.3 Support Market 2023-2030 ($M)

6.North America COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

7.South America MARKET SEGMENTATION Market 2023-2030 ($M)

7.1 By Deployment Market 2023-2030 ($M) - Regional Industry Research

7.1.1 On-Premise Market 2023-2030 ($M)

7.1.2 Cloud Market 2023-2030 ($M)

7.2 By Hardware Market 2023-2030 ($M) - Regional Industry Research

7.2.1 Body-Worn Camera Market 2023-2030 ($M)

7.2.2 Vehicle Dash Camera Market 2023-2030 ($M)

7.2.3 Citywide Camera Market 2023-2030 ($M)

7.2.4 Public Transit Video Market 2023-2030 ($M)

7.3 By Services Market 2023-2030 ($M) - Regional Industry Research

7.3.1 Consulting Market 2023-2030 ($M)

7.3.2 Training Market 2023-2030 ($M)

7.3.3 Support Market 2023-2030 ($M)

8.South America COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

9.Europe MARKET SEGMENTATION Market 2023-2030 ($M)

9.1 By Deployment Market 2023-2030 ($M) - Regional Industry Research

9.1.1 On-Premise Market 2023-2030 ($M)

9.1.2 Cloud Market 2023-2030 ($M)

9.2 By Hardware Market 2023-2030 ($M) - Regional Industry Research

9.2.1 Body-Worn Camera Market 2023-2030 ($M)

9.2.2 Vehicle Dash Camera Market 2023-2030 ($M)

9.2.3 Citywide Camera Market 2023-2030 ($M)

9.2.4 Public Transit Video Market 2023-2030 ($M)

9.3 By Services Market 2023-2030 ($M) - Regional Industry Research

9.3.1 Consulting Market 2023-2030 ($M)

9.3.2 Training Market 2023-2030 ($M)

9.3.3 Support Market 2023-2030 ($M)

10.Europe COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

11.APAC MARKET SEGMENTATION Market 2023-2030 ($M)

11.1 By Deployment Market 2023-2030 ($M) - Regional Industry Research

11.1.1 On-Premise Market 2023-2030 ($M)

11.1.2 Cloud Market 2023-2030 ($M)

11.2 By Hardware Market 2023-2030 ($M) - Regional Industry Research

11.2.1 Body-Worn Camera Market 2023-2030 ($M)

11.2.2 Vehicle Dash Camera Market 2023-2030 ($M)

11.2.3 Citywide Camera Market 2023-2030 ($M)

11.2.4 Public Transit Video Market 2023-2030 ($M)

11.3 By Services Market 2023-2030 ($M) - Regional Industry Research

11.3.1 Consulting Market 2023-2030 ($M)

11.3.2 Training Market 2023-2030 ($M)

11.3.3 Support Market 2023-2030 ($M)

12.APAC COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

13.MENA MARKET SEGMENTATION Market 2023-2030 ($M)

13.1 By Deployment Market 2023-2030 ($M) - Regional Industry Research

13.1.1 On-Premise Market 2023-2030 ($M)

13.1.2 Cloud Market 2023-2030 ($M)

13.2 By Hardware Market 2023-2030 ($M) - Regional Industry Research

13.2.1 Body-Worn Camera Market 2023-2030 ($M)

13.2.2 Vehicle Dash Camera Market 2023-2030 ($M)

13.2.3 Citywide Camera Market 2023-2030 ($M)

13.2.4 Public Transit Video Market 2023-2030 ($M)

13.3 By Services Market 2023-2030 ($M) - Regional Industry Research

13.3.1 Consulting Market 2023-2030 ($M)

13.3.2 Training Market 2023-2030 ($M)

13.3.3 Support Market 2023-2030 ($M)

14.MENA COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

LIST OF FIGURES

1.US Evidence Management Market Revenue, 2023-2030 ($M)

2.Canada Evidence Management Market Revenue, 2023-2030 ($M)

3.Mexico Evidence Management Market Revenue, 2023-2030 ($M)

4.Brazil Evidence Management Market Revenue, 2023-2030 ($M)

5.Argentina Evidence Management Market Revenue, 2023-2030 ($M)

6.Peru Evidence Management Market Revenue, 2023-2030 ($M)

7.Colombia Evidence Management Market Revenue, 2023-2030 ($M)

8.Chile Evidence Management Market Revenue, 2023-2030 ($M)

9.Rest of South America Evidence Management Market Revenue, 2023-2030 ($M)

10.UK Evidence Management Market Revenue, 2023-2030 ($M)

11.Germany Evidence Management Market Revenue, 2023-2030 ($M)

12.France Evidence Management Market Revenue, 2023-2030 ($M)

13.Italy Evidence Management Market Revenue, 2023-2030 ($M)

14.Spain Evidence Management Market Revenue, 2023-2030 ($M)

15.Rest of Europe Evidence Management Market Revenue, 2023-2030 ($M)

16.China Evidence Management Market Revenue, 2023-2030 ($M)

17.India Evidence Management Market Revenue, 2023-2030 ($M)

18.Japan Evidence Management Market Revenue, 2023-2030 ($M)

19.South Korea Evidence Management Market Revenue, 2023-2030 ($M)

20.South Africa Evidence Management Market Revenue, 2023-2030 ($M)

21.North America Evidence Management By Application

22.South America Evidence Management By Application

23.Europe Evidence Management By Application

24.APAC Evidence Management By Application

25.MENA Evidence Management By Application

The Evidence Management is projected to grow at 10.8% CAGR during the forecast period 2024-2030.

The Evidence Management size is estimated to be $7.2 billion in 2023 and is projected to reach $15.1 billion by 2030

The leading players in the Evidence Management are Motorola Solutions, Inc, Genetec Inc., OpenText, IBM Corporation, Palo Alto Networks and Others.

Growing use of wearable cameras, IoT sensors and drones for real-time evidence capture and management and blockchain for data integrity are some of the major Evidence Management trends in the industry which will create growth opportunities for the market during the forecast period.

Growth of cloud-based solutions, demand for data security and encryption, digital transformation in law enforcement and legal sectors, increasing use of automation tools, rising crime rates and need for efficient investigations & strict regulatory compliance are the driving factors of the Evidence Management.