Email

Email Print

Print

Food & Beverage Processing Equipment Market - Forecast(2025 - 2031)

Food & Beverage Processing Equipment Market Overview

Food & Beverage Processing Equipment market size is forecast to reach US$95 billion by 2030, after growing at a CAGR of 6.2% during 2024-2030. The major drivers in the Food & Beverage Processing Equipment Market include technological advancements that enhance efficiency, rising consumer demand for processed and convenience foods and strict food safety regulations that require updated processing methods. Additionally, the growth of the packaged food industry and the expansion of production capacities to meet global demands also contribute significantly. These factors collectively drive the need for advanced processing equipment to ensure high-quality and safe food products

Two significant trends in the Food & Beverage Processing Equipment Market are the increasing automation of processes and the focus on upcycling. Automation is revolutionizing the industry by enhancing productivity, improving product quality, and ensuring worker safety. The adoption of automated systems has several advantages, including improved hygiene, safety and an increase in productivity compared to manual systems. These benefits make automation a critical area of growth for companies aiming to stay competitive and efficient. Meanwhile, upcycling has emerged as a powerful sustainability trend, addressing the issue of food waste by transforming by-products and surplus food into new, high-quality products. According to the Upcycled Food Association, over 30% of all food produced globally is lost or wasted, posing a significant problem for society and the planet. Upcycled food helps mitigate this issue. This growing interest in upcycling reflects a broader commitment to more sustainable food production practices, aligning with efforts to reduce the environmental impact of the food industry.

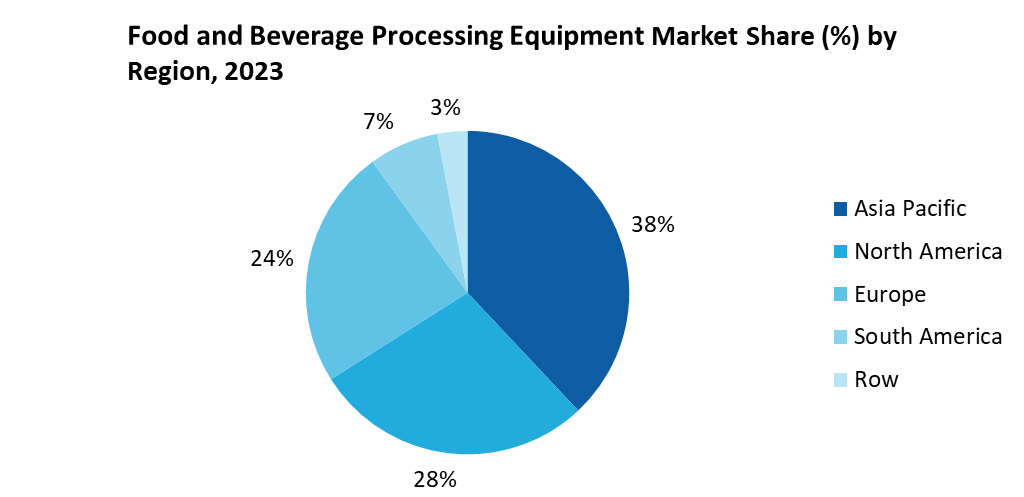

Market Snapshot:

Food & Beverage Processing Equipment Report Coverage

The report "Food & Beverage Processing Equipment Market Report – Forecast (2024-2030)" by IndustryARC covers an in-depth analysis of the following segments of the Food & Beverage Processing Equipment market.

| Attribute | Segment |

|---|---|

|

By Type |

|

|

By Mode of Operation |

|

|

By End Product Form |

|

|

By Technology |

|

|

By End Product Type |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The food and beverage processing equipment industry witnessed the demand for automation and advanced equipment escalating during the COVID 19 pandemic which arose due to the need to minimize human interaction and safety. Especially accelerating the investments in such technologies as robotics and IoT. Furthermore, the change in consumer behavior from minimally processed foods to packaged and processed necessitated equipment upgrades to accommodate increased production volumes and necessitated manufacturers to rethink their machinery requirements.

- The Russia-Ukraine war has drastically affected the supply of critical agricultural exports mainly grains and sunflower oil, which are essential in the food processing industry. Sanctions and severed trade routes raised raw material costs, leading equipment manufacturers to concentrate on energy efficient machinery and alternative modes of resource use. This geopolitical tension also forced companies to spread their supply chains, therefore, raising the need for investing in regionally sourced equipment and locally manufactured solutions.

Key Takeaways

Bakery Processing Equipment is the Largest Segment

The bakery processing equipment segment stands out as the largest in the Food & Beverage Processing Equipment market. This segment's growth is fueled by the increasing global demand for baked goods, such as bread, pastries and other bakery products due to changing consumer preferences, the rise in convenience foods and the growing popularity of on-the-go snacking options. The need for specialized equipment to handle the production, packaging and quality control of these goods is significant as manufacturers seek to maintain efficiency and consistency in their products. Additionally, equipment supplier Rademaker has announced a strategic partnership with Form & Frys, a Danish specialist in folding, forming, and filling machinery. This collaboration marks a significant step in Rademaker's evolution as a bakery equipment provider for mid-range to large-scale manufacturers across European and North American markets. With this partnership, Rademaker is set to be the exclusive supplier of Form & Frys equipment in key territories, including the UK, Germany, France, and the US—markets identified for their strong potential and alignment with the company’s values. Product lines that can be created using Form & Frys’ customized machines include Danish pastries, pies, pasties, and stuffed-crust pizzas, further supporting the growing demand for bakery products.

Semi-Automatic is the Largest Segment

The semi-automatic segment is the largest in the Food & Beverage Processing Equipment market due to its balance between automation and manual control. This equipment type is highly valued for its ability to significantly enhance labor productivity while offering flexibility in production processes. Its technical and economic feasibility makes it particularly attractive for small to medium-sized food processing operations. Additionally, semi-automatic systems allow for easier customization and adjustments during production, which is essential for meeting varying consumer demands in the rapidly evolving food industry. This versatility and cost-effectiveness contribute to the segment's dominance in the market. According to IMEKOFOODS, a semi-automatic system for classifying and describing foods achieved an accuracy of 91% for classification and 78% for description, highlighting its effectiveness in linking food consumption to food composition data through automated nutrient intake transformation.

APAC Leads the Market

The Asia-Pacific region commands a leading position in the Food & Beverage Processing Equipment Market, primarily driven by a surge in consumer demand for natural, healthy and conveniently packaged foods. High Hydrostatic Pressure (HPP) is a preservation technique that uses extremely high pressure to inactivate harmful microorganisms while preserving the food's natural flavor, texture, and nutritional value. China represents a tremendous opportunity for HPP driven by the country's rapidly evolving food industry. Currently, Hiperbaric holds a 23.5% market share in China and aims to capture 45% within the next five years. Consumers in the Asia Pacific region are increasingly seeking products that meet their evolving health-conscious preferences, prompting a rapid adoption of advanced food processing technologies. According to the Department of Global Business Management at Gangseo University, Seoul, South Korea, the Asia-Pacific region led the market, accounting for more than half of the worldwide revenue in 2022. This dominant position is indicative of the region's critical role in global food production and processing. The region's robust industrial infrastructure and investment in technological advancements further contribute to its leading position in the market. As consumer preferences continue to evolve, the Asia-Pacific is well-positioned to maintain its dominance through continuous innovation and adaptation in food and beverage processing technologies.

Rising Demand for Convenience Foods Drives the Market

A significant driver in the Food & Beverage Processing Equipment Market is the rising consumer demand for processed and convenience foods. Modern lifestyles, characterized by juggling work, family, and commuting, have led to a surge in demand for quick and easy meal options. This time constraint leads to a growing reliance on convenience foods, such as ready-to-eat meals from grocery stores and fast-food options. According to Grocery Trader, the biscuits and cakes have shown remarkable resilience amid the cost-of-living crisis. The strongest growth has occurred in more affordable segments such as Everyday Treats priced around $7.02 per kg compared to an average of $7.31. FBC UK's focus on smaller packs at competitive price points, particularly in the Everyday Treat segment of 'Sweet Biscuits, reflects this trend. Fox’s Favourites Crunch Creams experienced a 22% year-on-year increase, while Paterson’s, Britain’s leading shortbread brand grew by 17%, reaching $15.62 million. This shift in consumer behaviour is prompting food manufacturers to invest in advanced processing equipment that can meet the rising demand for convenient, high-quality products. To maintain efficiency, consistency, and safety in production, companies are adopting innovative technologies that allow them to scale up operations without compromising product standards. This trend underscores the crucial role that cutting-edge food processing equipment plays in satisfying the needs of a time-constrained population.

Impact of Stringent Food Safety Regulations Boosts the Adoption of Advanced Processing Technologies

Another significant driver is the stringent food safety regulations imposed by governments and international bodies, which compel manufacturers to adopt advanced processing technologies. Food safety is a critical concern, as contamination can lead to severe health risks and massive economic losses due to recalls and legal penalties. To comply with these regulations, manufacturers must upgrade their equipment to ensure hygienic processing environments, precise temperature control, and effective contamination prevention measures. For instance, the U.S. Food and Drug Administration (FDA) enforces rigorous standards under the Food Safety Modernization Act (FSMA), notably the Preventive Controls for Human Food rule. This regulation mandates food facilities to develop and implement a Food Safety Plan, encompassing hazard analysis, preventive controls, monitoring, corrective actions, and verification activities. Compliance with such regulations requires manufacturers to enhance their equipment, ensuring precise control over critical parameters like temperature, pressure, and sanitation. This has led to increased demand for automated systems that provide real-time monitoring and control, swiftly addressing any deviation from safe processing conditions. As these regulations become more widespread, including in emerging economies, the drive for compliance is spurring continual innovation and investment in cutting-edge food processing technologies.

Pollution Prevention is a Key Challenge

One of the significant challenges in the Food & Beverage Processing Equipment Market is the integration of effective pollution prevention (P2) practices to reduce toxic chemical releases and waste. The U.S. Environmental Protection Agency (EPA) has identified the food and beverage manufacturing sector as a key contributor to the Toxics Release Inventory (TRI), with about 1,707 facilities reporting the management of 2 billion pounds of production-related waste in 2020. These facilities release substantial quantities of hazardous chemicals, including ammonia and nitrate compounds, into the air and water, raising serious environmental and public health concerns. To address this issue, the EPA has emphasized the importance of P2 practices, such as source reduction, which involves eliminating waste at its origin rather than relying on treatment or disposal. Specific strategies include improving maintenance schedules to prevent leaks in refrigeration systems, particularly those using ammonia, and implementing dry cleanup methods to minimize wastewater contamination. Additionally, installing flow meters and water control units during cleaning processes can help reduce water usage and limit wastewater generation. However, integrating these P2 practices presents challenges for manufacturers. It often requires substantial investments in new equipment, training for staff, and modifications to existing operations. These hurdles can be difficult for smaller facilities to overcome, potentially hindering widespread adoption of P2 practices and limiting their effectiveness in reducing the sector’s environmental impact.

For more details on this report - Request for Sample

Food & Beverage Processing Equipment Industry Outlook

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the Food & Beverage Processing Equipment market. Global Food & Beverage Processing Equipment top 10 companies include:

1. Tetra Laval Group

2. GEA Group AG

3. Bühler AG

4. SPX Flow, Inc.

5. John Bean Technologies Corporation (JBT)

6. Marel hf.

7. Robert Bosch GmbH

8. Krones AG

9. Bucher Industries AG

10. BAADER

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

6.2% |

|

Market Size in 2030 |

$95 Billion |

|

Segments Covered |

By Type, By Mode of Operation, By End Product Form, By Technology, By End Product Type and By Geography |

|

Geographies Covered |

North America (U.S, Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Netherlands, Belgium and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, New Zealand, Singapore and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America) and Rest of the World (Middle East and Africa) |

|

Key Market Players |

1. Tetra Laval Group 2. GEA Group AG 3. Bühler AG 4. SPX Flow, Inc. 5. John Bean Technologies Corporation (JBT) 6. Marel hf. 7. Robert Bosch GmbH 8. Krones AG 9. Bucher Industries AG 10. BAADER |

For more Food and Beverage Market related reports, please click here

LIST OF TABLES

1.Global Food & Beverage Processing Equipment Market By Type Market 2023-2030 ($M)

1.1 Pre-Processing Market 2023-2030 ($M) - Global Industry Research

1.1.1 Sorting & Grading Market 2023-2030 ($M)

1.1.2 Mixing & Blending Market 2023-2030 ($M)

1.2 Processing Market 2023-2030 ($M) - Global Industry Research

1.2.1 Forming Market 2023-2030 ($M)

1.2.2 Extruding Market 2023-2030 ($M)

1.2.3 Coating Market 2023-2030 ($M)

1.2.4 Thermal Market 2023-2030 ($M)

1.2.5 Homogenization Market 2023-2030 ($M)

1.2.6 Filtration Market 2023-2030 ($M)

1.2.7 Pressing Market 2023-2030 ($M)

2.Global Food & Beverage Processing Equipment Market By End Product Form Market 2023-2030 ($M)

2.1 Solid Market 2023-2030 ($M) - Global Industry Research

2.2 Liquid Market 2023-2030 ($M) - Global Industry Research

2.3 Semi-Solid Market 2023-2030 ($M) - Global Industry Research

3.Global Food & Beverage Processing Equipment Market By Mode of Operation Market 2023-2030 ($M)

3.1 Semi-Automatic Market 2023-2030 ($M) - Global Industry Research

3.2 Automatic Market 2023-2030 ($M) - Global Industry Research

4.Global Food & Beverage Processing Equipment Market By Type Market 2023-2030 (Volume/Units)

4.1 Pre-Processing Market 2023-2030 (Volume/Units) - Global Industry Research

4.1.1 Sorting & Grading Market 2023-2030 (Volume/Units)

4.1.2 Mixing & Blending Market 2023-2030 (Volume/Units)

4.2 Processing Market 2023-2030 (Volume/Units) - Global Industry Research

4.2.1 Forming Market 2023-2030 (Volume/Units)

4.2.2 Extruding Market 2023-2030 (Volume/Units)

4.2.3 Coating Market 2023-2030 (Volume/Units)

4.2.4 Thermal Market 2023-2030 (Volume/Units)

4.2.5 Homogenization Market 2023-2030 (Volume/Units)

4.2.6 Filtration Market 2023-2030 (Volume/Units)

4.2.7 Pressing Market 2023-2030 (Volume/Units)

5.Global Food & Beverage Processing Equipment Market By End Product Form Market 2023-2030 (Volume/Units)

5.1 Solid Market 2023-2030 (Volume/Units) - Global Industry Research

5.2 Liquid Market 2023-2030 (Volume/Units) - Global Industry Research

5.3 Semi-Solid Market 2023-2030 (Volume/Units) - Global Industry Research

6.Global Food & Beverage Processing Equipment Market By Mode of Operation Market 2023-2030 (Volume/Units)

6.1 Semi-Automatic Market 2023-2030 (Volume/Units) - Global Industry Research

6.2 Automatic Market 2023-2030 (Volume/Units) - Global Industry Research

7.North America Food & Beverage Processing Equipment Market By Type Market 2023-2030 ($M)

7.1 Pre-Processing Market 2023-2030 ($M) - Regional Industry Research

7.1.1 Sorting & Grading Market 2023-2030 ($M)

7.1.2 Mixing & Blending Market 2023-2030 ($M)

7.2 Processing Market 2023-2030 ($M) - Regional Industry Research

7.2.1 Forming Market 2023-2030 ($M)

7.2.2 Extruding Market 2023-2030 ($M)

7.2.3 Coating Market 2023-2030 ($M)

7.2.4 Thermal Market 2023-2030 ($M)

7.2.5 Homogenization Market 2023-2030 ($M)

7.2.6 Filtration Market 2023-2030 ($M)

7.2.7 Pressing Market 2023-2030 ($M)

8.North America Food & Beverage Processing Equipment Market By End Product Form Market 2023-2030 ($M)

8.1 Solid Market 2023-2030 ($M) - Regional Industry Research

8.2 Liquid Market 2023-2030 ($M) - Regional Industry Research

8.3 Semi-Solid Market 2023-2030 ($M) - Regional Industry Research

9.North America Food & Beverage Processing Equipment Market By Mode of Operation Market 2023-2030 ($M)

9.1 Semi-Automatic Market 2023-2030 ($M) - Regional Industry Research

9.2 Automatic Market 2023-2030 ($M) - Regional Industry Research

10.South America Food & Beverage Processing Equipment Market By Type Market 2023-2030 ($M)

10.1 Pre-Processing Market 2023-2030 ($M) - Regional Industry Research

10.1.1 Sorting & Grading Market 2023-2030 ($M)

10.1.2 Mixing & Blending Market 2023-2030 ($M)

10.2 Processing Market 2023-2030 ($M) - Regional Industry Research

10.2.1 Forming Market 2023-2030 ($M)

10.2.2 Extruding Market 2023-2030 ($M)

10.2.3 Coating Market 2023-2030 ($M)

10.2.4 Thermal Market 2023-2030 ($M)

10.2.5 Homogenization Market 2023-2030 ($M)

10.2.6 Filtration Market 2023-2030 ($M)

10.2.7 Pressing Market 2023-2030 ($M)

11.South America Food & Beverage Processing Equipment Market By End Product Form Market 2023-2030 ($M)

11.1 Solid Market 2023-2030 ($M) - Regional Industry Research

11.2 Liquid Market 2023-2030 ($M) - Regional Industry Research

11.3 Semi-Solid Market 2023-2030 ($M) - Regional Industry Research

12.South America Food & Beverage Processing Equipment Market By Mode of Operation Market 2023-2030 ($M)

12.1 Semi-Automatic Market 2023-2030 ($M) - Regional Industry Research

12.2 Automatic Market 2023-2030 ($M) - Regional Industry Research

13.Europe Food & Beverage Processing Equipment Market By Type Market 2023-2030 ($M)

13.1 Pre-Processing Market 2023-2030 ($M) - Regional Industry Research

13.1.1 Sorting & Grading Market 2023-2030 ($M)

13.1.2 Mixing & Blending Market 2023-2030 ($M)

13.2 Processing Market 2023-2030 ($M) - Regional Industry Research

13.2.1 Forming Market 2023-2030 ($M)

13.2.2 Extruding Market 2023-2030 ($M)

13.2.3 Coating Market 2023-2030 ($M)

13.2.4 Thermal Market 2023-2030 ($M)

13.2.5 Homogenization Market 2023-2030 ($M)

13.2.6 Filtration Market 2023-2030 ($M)

13.2.7 Pressing Market 2023-2030 ($M)

14.Europe Food & Beverage Processing Equipment Market By End Product Form Market 2023-2030 ($M)

14.1 Solid Market 2023-2030 ($M) - Regional Industry Research

14.2 Liquid Market 2023-2030 ($M) - Regional Industry Research

14.3 Semi-Solid Market 2023-2030 ($M) - Regional Industry Research

15.Europe Food & Beverage Processing Equipment Market By Mode of Operation Market 2023-2030 ($M)

15.1 Semi-Automatic Market 2023-2030 ($M) - Regional Industry Research

15.2 Automatic Market 2023-2030 ($M) - Regional Industry Research

16.APAC Food & Beverage Processing Equipment Market By Type Market 2023-2030 ($M)

16.1 Pre-Processing Market 2023-2030 ($M) - Regional Industry Research

16.1.1 Sorting & Grading Market 2023-2030 ($M)

16.1.2 Mixing & Blending Market 2023-2030 ($M)

16.2 Processing Market 2023-2030 ($M) - Regional Industry Research

16.2.1 Forming Market 2023-2030 ($M)

16.2.2 Extruding Market 2023-2030 ($M)

16.2.3 Coating Market 2023-2030 ($M)

16.2.4 Thermal Market 2023-2030 ($M)

16.2.5 Homogenization Market 2023-2030 ($M)

16.2.6 Filtration Market 2023-2030 ($M)

16.2.7 Pressing Market 2023-2030 ($M)

17.APAC Food & Beverage Processing Equipment Market By End Product Form Market 2023-2030 ($M)

17.1 Solid Market 2023-2030 ($M) - Regional Industry Research

17.2 Liquid Market 2023-2030 ($M) - Regional Industry Research

17.3 Semi-Solid Market 2023-2030 ($M) - Regional Industry Research

18.APAC Food & Beverage Processing Equipment Market By Mode of Operation Market 2023-2030 ($M)

18.1 Semi-Automatic Market 2023-2030 ($M) - Regional Industry Research

18.2 Automatic Market 2023-2030 ($M) - Regional Industry Research

19.MENA Food & Beverage Processing Equipment Market By Type Market 2023-2030 ($M)

19.1 Pre-Processing Market 2023-2030 ($M) - Regional Industry Research

19.1.1 Sorting & Grading Market 2023-2030 ($M)

19.1.2 Mixing & Blending Market 2023-2030 ($M)

19.2 Processing Market 2023-2030 ($M) - Regional Industry Research

19.2.1 Forming Market 2023-2030 ($M)

19.2.2 Extruding Market 2023-2030 ($M)

19.2.3 Coating Market 2023-2030 ($M)

19.2.4 Thermal Market 2023-2030 ($M)

19.2.5 Homogenization Market 2023-2030 ($M)

19.2.6 Filtration Market 2023-2030 ($M)

19.2.7 Pressing Market 2023-2030 ($M)

20.MENA Food & Beverage Processing Equipment Market By End Product Form Market 2023-2030 ($M)

20.1 Solid Market 2023-2030 ($M) - Regional Industry Research

20.2 Liquid Market 2023-2030 ($M) - Regional Industry Research

20.3 Semi-Solid Market 2023-2030 ($M) - Regional Industry Research

21.MENA Food & Beverage Processing Equipment Market By Mode of Operation Market 2023-2030 ($M)

21.1 Semi-Automatic Market 2023-2030 ($M) - Regional Industry Research

21.2 Automatic Market 2023-2030 ($M) - Regional Industry Research

LIST OF FIGURES

1.US Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

2.Canada Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

3.Mexico Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

4.Brazil Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

5.Argentina Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

6.Peru Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

7.Colombia Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

8.Chile Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

9.Rest of South America Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

10.UK Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

11.Germany Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

12.France Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

13.Italy Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

14.Spain Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

15.Rest of Europe Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

16.China Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

17.India Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

18.Japan Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

19.South Korea Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

20.South Africa Food & Beverage Processing Equipment Market Revenue, 2023-2030 ($M)

21.North America Food & Beverage Processing Equipment By Application

22.South America Food & Beverage Processing Equipment By Application

23.Europe Food & Beverage Processing Equipment By Application

24.APAC Food & Beverage Processing Equipment By Application

25.MENA Food & Beverage Processing Equipment By Application

26.Marel, Sales /Revenue, 2015-2018 ($Mn/$Bn)

27.GEA Group, Sales /Revenue, 2015-2018 ($Mn/$Bn)

28.Buhler, Sales /Revenue, 2015-2018 ($Mn/$Bn)

29.JBT Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

30.Alfa Laval, Sales /Revenue, 2015-2018 ($Mn/$Bn)

31.Bucher Industries, Sales /Revenue, 2015-2018 ($Mn/$Bn)

32.Clextral, Sales /Revenue, 2015-2018 ($Mn/$Bn)

33.SPX Flow, Sales /Revenue, 2015-2018 ($Mn/$Bn)

34.Bigtem Makine, Sales /Revenue, 2015-2018 ($Mn/$Bn)

35.Fenco Food Machinery, Sales /Revenue, 2015-2018 ($Mn/$Bn)

36.Krones Group, Sales /Revenue, 2015-2018 ($Mn/$Bn)

The Food & Beverage Processing Equipment Market is projected to grow at 6.2% CAGR during the forecast period 2024-2030.

The Food & Beverage Processing Equipment Market size is estimated to be $63.2 billion in 2023 and is projected to reach $95 billion by 2030

The leading players in the Food & Beverage Processing Equipment Market are Tetra Laval Group, GEA Group AG, Bühler AG, SPX Flow, Inc., John Bean Technologies Corporation (JBT) and Others

Increasing automaton of processes and the focus on upcycling are some of the major Food & Beverage Processing Equipment Market trends in the industry which will create growth opportunities for the market during the forecast period.

Technological advancements, rising consumer demand for processed foods, strict food safety regulations, growth of the packaged food industry and the expansion of production capacities are the driving factors of the market.