Email

Email Print

Print

Gaming Monitors Market - By Display Technology , By Screen Size , By Resolution , By Price Range , By Geography - Global Opportunity Analysis & Industry Forecast, 2024-2030.

Gaming Monitors Market Overview

Gaming Monitors market size is forecast to reach $35 billion by 2030, after growing at a CAGR of 6.1% during 2024-2030. The gaming monitor market is experiencing significant growth, driven by the increasing popularity of gaming and advancements in display technology. Additionally, the demand for high-resolution displays, faster refresh rates and immersive features like curved screens and HDR capabilities. Moreover, the rise in the popularity of streaming games as well as the growth of content creators and influencers are driving the demand for gaming monitors. A major trend in the market is Mini-LED Backlighting. This technology offers improved contrast, better local dimming zones, and more accurate color reproduction compared to traditional LED backlighting. The adoption of ultra-high refresh rates is a growing trend in the gaming monitor market, driven by the demand for smoother and more responsive gaming experiences. Monitors with refresh rates of 240Hz and above are becoming increasingly popular among competitive gamers and enthusiasts who require precise visuals for fast-paced games like first-person shooters and battle royales. For instance, in July 2024, LG launched the LG UltraGear OLED series in four sizes – 27-inch, 34-inch, 39-inch and 45-inch – in India for gamers. As per the company, the gaming monitors offer OLED technology enhanced with Micro Lens Array Plus (MLA+) and the display offers response times of 0.03ms and a refresh rate of up to 240HZ for smooth motion and reduced eye strain.

Market Snapshot:

Gaming Monitors Market - Report Coverage:

The “Gaming Monitors Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Gaming Monitors Market.

| Attribute | Segment |

|---|---|

|

By Display Technology |

|

|

By Screen Size |

|

|

By Resolution |

|

|

By Price Range |

|

|

By Geography |

|

Key Takeaways

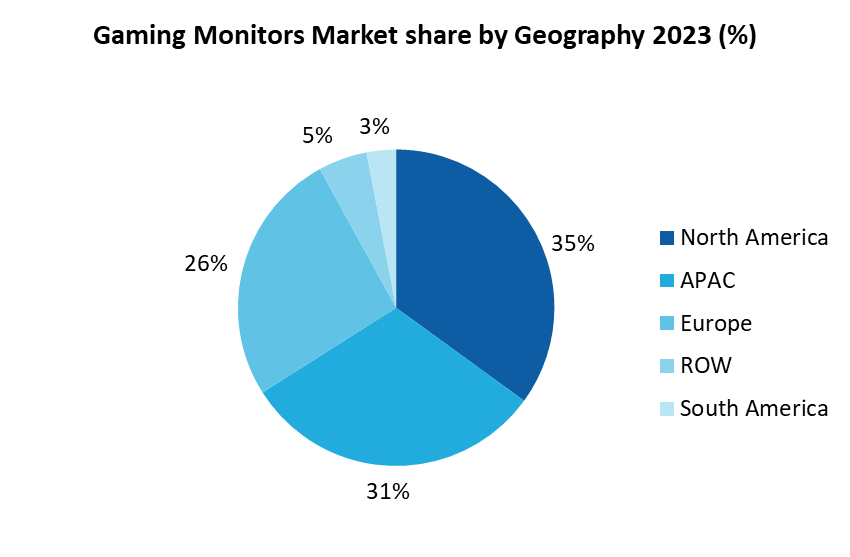

North America dominates the market

North America holds the largest share of the global gaming monitor market with a market share of 35% in 2023. This dominance is attributed to several factors like well-established gaming culture and a large base of avid gamers. According to Entertainment Software Association’s 2024 Essential Facts About the U.S. Video Game Industry Report, Americans who play video games represent 190.6 million of the population. North America is also a hub for technological innovation, leading to early adoption of advanced gaming monitor features. Along with that, major gaming hardware manufacturers are based in North America, driving the demand for high-performance gaming monitors. According to a report in Newzoo, in 2023, the top 10 markets and countries by revenue were the United States, China, Japan, South Korea, Germany, the United Kingdom, France, Canada, Italy, and Mexico.

Full HD Segment Dominated the Market

Full HD is the largest segment in the U.S. Computer Monitor market in terms of resolution. With this resolution, more than two million pixels come together to produce crisp, detailed images. From web browsing to streaming movies or playing games, it is ideal for a wide range of applications. It is a great option for both work and play because of its high pixel density, which ensures that text is clear and images are vivid. Additionally, it generally provides good visual quality at a lower cost than greater resolutions. Additionally, full HD monitor supports multitasking effectively. Its resolution allows users to open multiple windows simultaneously without feeling cramped, making it easier to juggle tasks like research, writing, and video conferencing. Thus, Full HD remains the most widely adopted resolution in the U.S. computer monitor market due to its balance of price, performance, and compatibility.

24–32 inch monitors dominates the market

24–32 inch monitors are a top choice for most users due to their versatility and suitability for most games while remaining ergonomically manageable. These monitors, particularly 24-25 inches, are favoured by competitive gamers who prioritize high refresh rates, low input lag, and affordability. They are compact, fit small desks, and offer focused gameplay without requiring significant hardware power for high performance. However, they may lack the immersive experience larger monitors provide. In November 2024, BenQ launched its new gaming monitor, the Zowie XL2566X+ gaming monitor in India. The Zowie XL2566X+ monitor is also available with various other refresh rate options, such as 540Hz, 360Hz, and 240Hz. It is also available in different screen sizes, including 24-inch and 27-inch. The 24–32inch range tends to be the most popular, striking a balance between screen space, resolution and usability for both gaming and work.

Demand for Larger and High-Resolution Monitors to Boost the Market

The demand for larger and high-resolution gaming monitors has been steadily increasing, driven by the growing preference for immersive and high-quality gaming experiences. Larger screens, typically 27 inches or more, provide a more immersive gaming experience. Ultrawide and curved monitors, often above 32 inches, enhance field-of-view (FOV) in games, making them particularly appealing for simulation and adventure genres. While smaller monitors are favoured in some competitive gaming scenarios for focus and speed, larger monitors with high refresh rates are becoming more prevalent among enthusiasts. In August 2024, Acer released the Predator X39 OLED gaming monitor. The rapid adoption of higher resolution is driven by its ability to support high-definition displays and advanced features such as HDR (High Dynamic Range), which significantly enhances the gaming experience.

High Competition from Alternative Gaming Solutions to Hamper the Market

The rise of handheld gaming devices, cloud gaming, and VR technologies presents alternatives to traditional gaming setups, potentially reducing the demand for gaming monitors. IDC forecasts the gaming market for PCs and monitors will recover in 2024, after unit contractions in both 2022 and 2023. Gaming volume is expected to hit 69.3 million in 2024, or 9% higher than 2023. Gaming desktops, a key segment for high-end gaming and monitors, is expected to recover in 2025 as new GPUs land in stores. Gaming penetration is also expected to take an increased share going forward, with gaming taking 20% of the total PC and Monitor market by 2028.

For more details on this report - Request for Sample

Key Market Players

Global Gaming Monitors top 10 companies include:

- Samsung Electronics Co. Ltd.

- Dell Inc.

- ASUSTeK Computer Inc.

- LG Electronics

- Lenovo Group Limited

- Acer Inc.

- MICRO-STAR INTERNATIONAL CO. LTD.

- Koninklijke Philips N.V.

- HP Inc.

- ViewSonic Corporation

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

6.1% |

|

Market Size in 2030 |

$35 billion |

|

Segments Covered |

By Display Technology, By Screen Size, By Price Range, By Geography |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Netherlands, Belgium and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Indonesia, Malaysia, Thailand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

For more Electronics Market reports, please click here

The Gaming Monitors Market is projected to grow at 6.1% CAGR during the forecast period 2024-2030.

The Gaming Monitors Market size is estimated to be $23.3 billion in 2023 and is projected to reach $35 billion by 2030

The leading players in the Gaming Monitors Market are Samsung Electronics Co. Ltd., Dell Inc., ASUSTeK Computer Inc., LG Electronics, Lenovo Group Limited and others.

Mini-LED Backlighting and ultra-high refresh rates are the major trends that will shape the market in the future.

Increasing interest in gaming, advancements in technology, and the growing popularity of eSports are the driving factors