Email

Email Print

Print

Fungicidal Seed Treatment Market - By Type , By Source , By Form , By Mode of Action , By Crop Type , By Application By Geography - Opportunity Analysis & Industry Forecast, 2024-2030”.

Fungicidal Seed Treatment Market Overview:

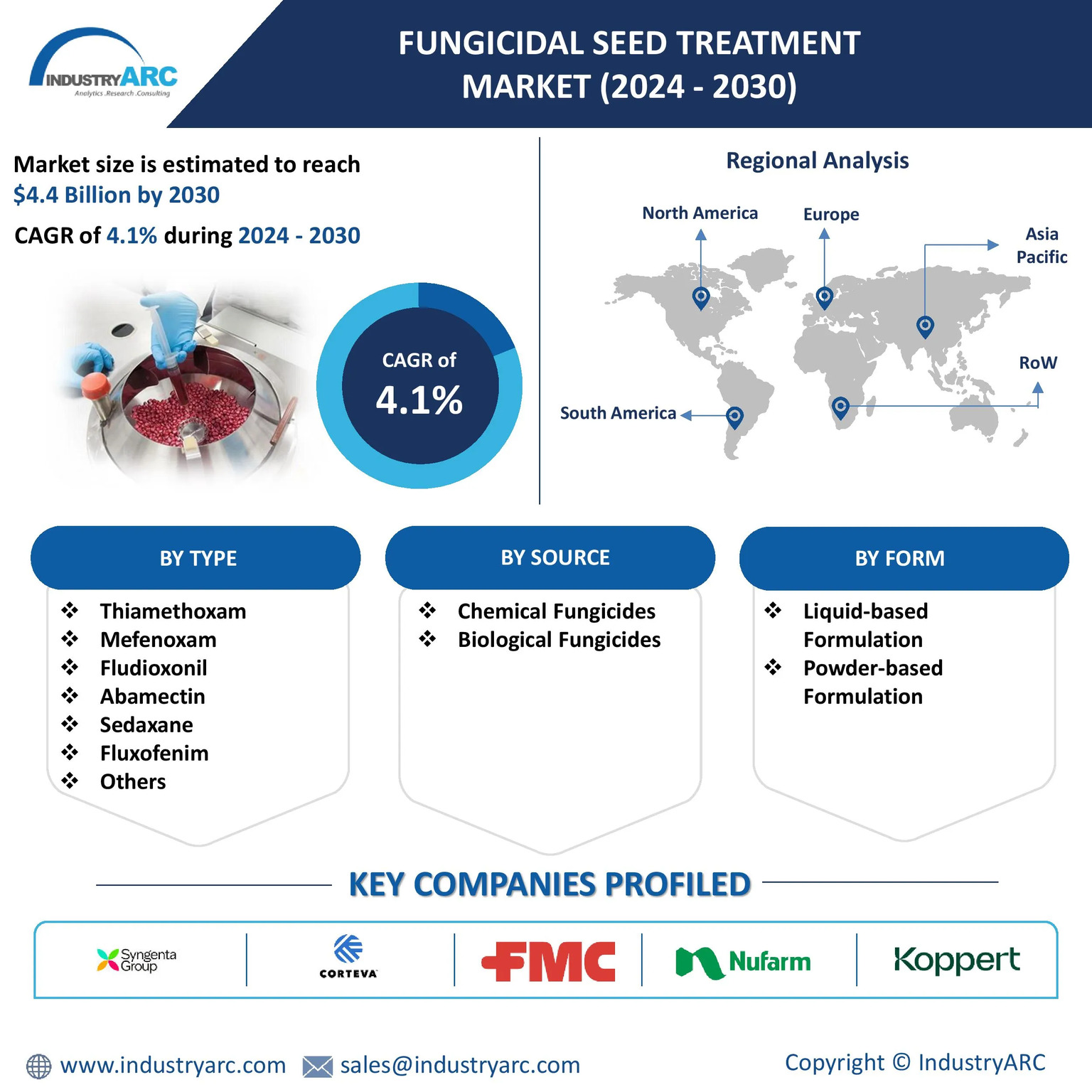

The Fungicidal Seed Treatment Market size is estimated to reach $4.4 Billion by 2030, growing at a CAGR of 4.1% during the forecast period 2024-2030. The market for fungicidal seed treatments is expanding significantly as a result of the rising incidence of fungal infections and the rising demand for crops with high yields. Additionally, advancements in biotechnology and microbiology and rising awareness of crop protection because of government initiatives drives the market growth of fungicidal seed treatment.

Nanotechnology is also one of the current important trends in fungicidal seed treatment, answering the need for precision and efficiency in disease prevention, yield enhancement, and sustainability in agriculture. The approach involves nanoparticles in developing newer and more effective fungicide formulations, enabling finer particles to help provide better penetration and controlled release of active ingredients. Nanotechnology has made it possible to create liquid formulations that are more effective and have a smaller environmental impact. These formulations contain fungicides that are released gradually and under control, giving seeds long-lasting protection and lowering the likelihood of resistance development. Nano-fungicidal formulations will be expected to capture more market share as agricultural industries move toward greener solutions, impelled by their capability to provide enhanced disease control with the least ecological footprint.

Market Snapshot:

Fungicidal Seed Treatment Market - Report Coverage:

The “Fungicidal Seed Treatment Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Fungicidal Seed Treatment Market.

| Attribute | Segment |

|---|---|

|

|

|

By Source |

|

|

By Form |

|

|

By Mode of Action |

|

|

By Crop Type |

|

|

By Application |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic significantly disrupted global supply chains and economic activities, impacting various industries, including agriculture. The fungicidal seed treatment market was not immune to these disruptions. Lockdowns and economic uncertainty led to a decline in agricultural activities and a corresponding decrease in demand for fungicidal seed treatments. However, disruptions in supply chains and increased transportation costs led to higher prices for raw materials and finished products.

- The ongoing Russia-Ukraine war had a significant impact on global commodity markets, including agricultural products such as fungicidal seed treatment market. The conflict disrupted the supply of key agricultural commodities, such as wheat, corn, and sunflower oil, leading to a surge in prices and putting pressure on farmer’s profit margins and reducing their spending on inputs like fungicidal seed treatments.

Key Takeaways:

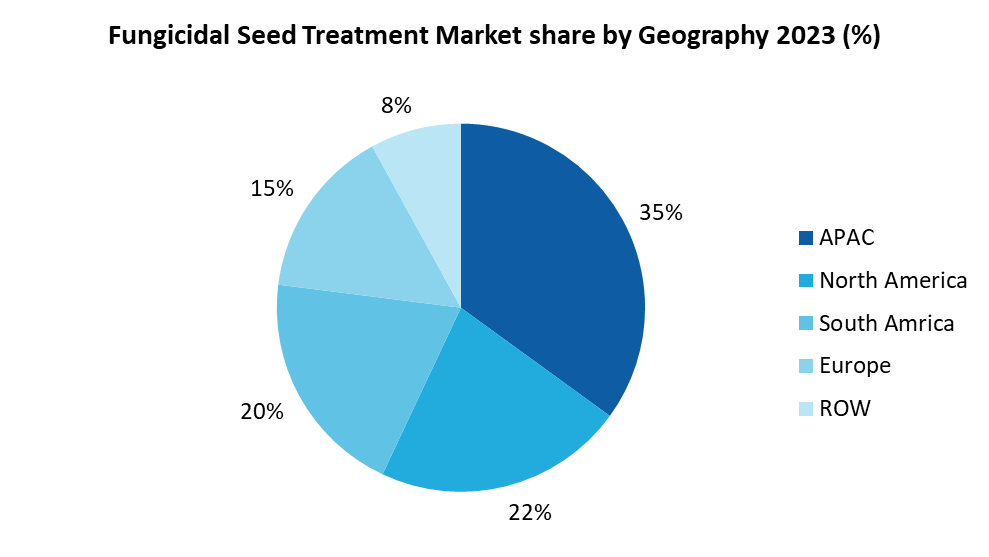

North America is leading the market

North America holds a market share of 38% in Fungicidal seed treatment market. North America’s dominance in the fungicidal seed treatment market can be attributed to several key factors such as ranging from the region’s agricultural practices to its technological advancements and government initiatives. These factors work together to create an environment where fungicidal seed treatments are not only necessary but also well-supported by infrastructure, research, and investment. Most of the commercial farming enterprises are located throughout North America, especially in the United States and Canada. The large-scale cultivation of important crops including corn, soybeans, and wheat generates a sizable need for crop protection chemicals, such as fungicidal seed treatments. The highly established agricultural infrastructure in North America, which includes access to equipment and facilities for seed treatment, guarantees that fungicidal seed treatments are done accurately and consistently, maximizing their effectiveness.

Chemical Fungicides dominates the market

Chemical Fungicidal seed treatment fungicides continue to hold the majority share in the global fungicidal seed treatment market. These fungicides are primarily composed of synthetic chemicals, including triazoles, strobilurins, and dithiocarbonates, which have been effective in controlling a broad spectrum of fungal pathogens. They offer a quick and cost-effective solution for farmers, particularly in large-scale agricultural operations. For instance, Corteva Agriscience introduced LumiTre, a new fungicide seed treatment designed specifically for soybeans. This product combines three active ingredients (oxathiapiprolin, ipconazole, and picoxystrobin) targeting key diseases such as Phytophthora sojae, which is notorious for causing yield losses in North American soybean crops. Chemical fungicides are widely used for crops like wheat, corn, and soybeans, which are prone to seed and soil-borne fungal diseases like Rhizoctonia, Fusarium, and Phytophthora. They are effective in managing fungal diseases in early growth stages, which has led to their widespread use across high-value crops. Therefore, the trend in the fungicidal seed treatment market clearly indicates a strong reliance on chemical solutions, as these products not only enhance disease resistance but also contribute to improved agricultural productivity.

Liquid-based fungicidal seed treatments dominate the market

The market is dominated by liquid-based fungicidal seed treatments due to their extensive application over a wide range of crops, consistent seed coverage efficacy and ease of use. Liquid formulations provide better adhesion to the seed surface, ensuring optimal protection against fungal pathogens with more uniform coverage of the seed, reducing the risk of untreated areas.. Liquid fungicidal formulations provide uniform coating on seeds which enhances protection against fungal pathogens during early growth stages. For instance, rice blast, caused by the fungus Pyricularia oryzae, can cause significant yield losses in rice plants during early growth stages. According to the IRRI, rice blast is one of the most destructive diseases of rice and can cause yield losses of about 10% to 30% annually. The liquid form allows for better adherence to the seed surface resulting in improved uptake and distribution of the fungicidal agents. Additionally, liquid treatments are compatible with other chemical seed treatments, such as insecticides or nutrients, allowing for an integrated approach to seed health. Liquid formulations are generally easier to apply compared to powders or dusts, reducing the potential for human error and exposure. In conclusion, liquid-based fungicidal seed treatments have gained significant market share due to their improved adhesion, coverage, ease of application, and compatibility with other seed treatments.

Need for Food Security Drives the Market

The current state of global food security is becoming more complicated due to factors including population expansion, climate change, and the emergence of new illnesses and pests. The current world population of over 8.18 billion is expected to reach 8.6 billion in 2030, 9.8 billion in 2050, and 11.2 billion in 2100, according to the United Nations. These difficulties have a significant impact on the market for fungicidal seed treatments since farmers wish to safeguard their crops against fungal infections and guarantee higher yields. Plant diseases are becoming more and more of a problem for the yield and loss of important crops, and this problem is particularly noticeable in developing nations. A primary factor in crop output losses is pests. According to the Food and Agriculture Organization estimates, plant diseases and pests cause between 20 and 40% of annual global crop yield losses. A growing demand for fungicidal seed treatments is being driven by issues related to global food security because the demand for these products will continue to grow as farmers work to protect their crops and guarantee food production.

Lack of Awareness

The major challenge for the market is unawareness among farmers about the benefits and use of fungicidal treatment in seeds. Most of the people who are involved in the agricultural field do not have any idea about the benefits that could be derived from such applications since it helps in successfully saving the crops from any type of soil-borne and seed-borne diseases, improves germination, and maximizes plant health. While some farmers have a general idea about the work of seed treatments, complete misinformation has been generated on the type of diseases the various pesticides target. For instance, metalaxyl and mefenoxam are effective in Pythium and Phytophthora but could be weak in Fusarium and Rhizoctonia among other types. This is where a knowledge gap on proper treatment selection and its application can lead to reduced efficacy, causing a poor crop yield.

For more details on this report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Fungicidal Seed Treatment Market. The top 10 companies in this industry are listed below:

- Syngenta Group

- Corteva Agriscience

- FMC Corporation

- Nufarm Limited

- Koppert

- Sumitomo Chemical Co., Ltd.

- Bayer CropScience AG

- BASF SE

- UPL Ltd.

- Novozymes

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

4.1% |

|

Market Size in 2030 |

$4.4 Billion |

|

Segments Covered |

By Source, By Type, By Form, By Mode of Action, By Crop Type, By Application and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

For more Agriculture Market reports, please click here

LIST OF TABLES

1.Global Market Segmentation Market 2023-2030 ($M)

1.1 By Application Market 2023-2030 ($M) - Global Industry Research

1.1.1 Chemical Market 2023-2030 ($M)

1.1.2 Non- Chemical Market 2023-2030 ($M)

2.Global Competitive landscape Market 2023-2030 ($M)

2.1 Most Active Companies Market 2023-2030 ($M) - Global Industry Research

3.Global Market Segmentation Market 2023-2030 (Volume/Units)

3.1 By Application Market 2023-2030 (Volume/Units) - Global Industry Research

3.1.1 Chemical Market 2023-2030 (Volume/Units)

3.1.2 Non- Chemical Market 2023-2030 (Volume/Units)

4.Global Competitive landscape Market 2023-2030 (Volume/Units)

4.1 Most Active Companies Market 2023-2030 (Volume/Units) - Global Industry Research

5.North America Market Segmentation Market 2023-2030 ($M)

5.1 By Application Market 2023-2030 ($M) - Regional Industry Research

5.1.1 Chemical Market 2023-2030 ($M)

5.1.2 Non- Chemical Market 2023-2030 ($M)

6.North America Competitive landscape Market 2023-2030 ($M)

6.1 Most Active Companies Market 2023-2030 ($M) - Regional Industry Research

7.South America Market Segmentation Market 2023-2030 ($M)

7.1 By Application Market 2023-2030 ($M) - Regional Industry Research

7.1.1 Chemical Market 2023-2030 ($M)

7.1.2 Non- Chemical Market 2023-2030 ($M)

8.South America Competitive landscape Market 2023-2030 ($M)

8.1 Most Active Companies Market 2023-2030 ($M) - Regional Industry Research

9.Europe Market Segmentation Market 2023-2030 ($M)

9.1 By Application Market 2023-2030 ($M) - Regional Industry Research

9.1.1 Chemical Market 2023-2030 ($M)

9.1.2 Non- Chemical Market 2023-2030 ($M)

10.Europe Competitive landscape Market 2023-2030 ($M)

10.1 Most Active Companies Market 2023-2030 ($M) - Regional Industry Research

11.APAC Market Segmentation Market 2023-2030 ($M)

11.1 By Application Market 2023-2030 ($M) - Regional Industry Research

11.1.1 Chemical Market 2023-2030 ($M)

11.1.2 Non- Chemical Market 2023-2030 ($M)

12.APAC Competitive landscape Market 2023-2030 ($M)

12.1 Most Active Companies Market 2023-2030 ($M) - Regional Industry Research

13.MENA Market Segmentation Market 2023-2030 ($M)

13.1 By Application Market 2023-2030 ($M) - Regional Industry Research

13.1.1 Chemical Market 2023-2030 ($M)

13.1.2 Non- Chemical Market 2023-2030 ($M)

14.MENA Competitive landscape Market 2023-2030 ($M)

14.1 Most Active Companies Market 2023-2030 ($M) - Regional Industry Research

LIST OF FIGURES

1.US Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

2.Canada Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

3.Mexico Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

4.Brazil Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

5.Argentina Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

6.Peru Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

7.Colombia Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

8.Chile Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

9.Rest of South America Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

10.UK Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

11.Germany Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

12.France Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

13.Italy Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

14.Spain Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

15.Rest of Europe Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

16.China Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

17.India Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

18.Japan Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

19.South Korea Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

20.South Africa Global Fungicidal Seed Treatment Market Revenue, 2023-2030 ($M)

21.North America Global Fungicidal Seed Treatment By Application

22.South America Global Fungicidal Seed Treatment By Application

23.Europe Global Fungicidal Seed Treatment By Application

24.APAC Global Fungicidal Seed Treatment By Application

25.MENA Global Fungicidal Seed Treatment By Application

26.Adama Agricultural Solutions Ltd, Sales /Revenue, 2015-2018 ($Mn/$Bn)

27.BASF SE, Sales /Revenue, 2015-2018 ($Mn/$Bn)

28.Bayer Cropscience AG, Sales /Revenue, 2015-2018 ($Mn/$Bn)

29.Bioworks Inc., Sales /Revenue, 2015-2018 ($Mn/$Bn)

30.Brettyoung Limited, Sales /Revenue, 2015-2018 ($Mn/$Bn)

31.Chemtura Agrosolutions, Sales /Revenue, 2015-2018 ($Mn/$Bn)

32.Dupont, Sales /Revenue, 2015-2018 ($Mn/$Bn)

33.Monsanto Company, Sales /Revenue, 2015-2018 ($Mn/$Bn)

34.Novozymes A/S, Sales /Revenue, 2015-2018 ($Mn/$Bn)

35.Nufarm Ltd, Sales /Revenue, 2015-2018 ($Mn/$Bn)

36.Precision Laboratories LLC, Sales /Revenue, 2015-2018 ($Mn/$Bn)

37.Syngenta International AG, Sales /Revenue, 2015-2018 ($Mn/$Bn)

38.Valent USA Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

39.Verdesian Life Sciences, Sales /Revenue, 2015-2018 ($Mn/$Bn)

40.Wolf Trax Inc., Sales /Revenue, 2015-2018 ($Mn/$Bn)

The Fungicidal Seed Treatment Market is projected to grow at 4.1% CAGR during the forecast period 2024-2030.

The Fungicidal Seed Treatment Market size is estimated to be $3.5 billion in 2023 and is projected to reach $4.4 Billion by 2030

Leading players in the Fungicidal Seed Treatment Market are Syngenta, Corteva Agriscience, FMC Corporation, Nufarm Limited, Adama Agriculture Solutions and others.

Demand for biofungicidal seed treatment & nanotechnology are the major trends that will shape the market in the future.

The market for fungicidal seed treatments is expanding significantly due to several factors, including the rise in fungal infections, the need for higher-yielding crops, improvements in microbiology and biotechnology, and government efforts.