Email

Email Print

Print

Hydrogen Fuel Cell Vehicle Market- By Vehicle Type , By Technology , By Operating Miles , By Power Output and By Geography - Opportunity Analysis & Industry Forecast, 2024-2030.

Hydrogen Fuel Cell Vehicle Market Overview:

The Hydrogen Fuel Cell Vehicle Market size is estimated to reach $15.2 billion by 2030, growing at a CAGR of 38.9% during the forecast period 2024-2030. The hydrogen fuel cell vehicle (FCV) market refers to the growing sector focused on the development, production and deployment of vehicles powered by hydrogen fuel cells which convert hydrogen into electricity to power the vehicle’s drivetrain. This technology is part of the broader shift toward zero-emission transportation, offering an alternative to traditional internal combustion engine (ICE) vehicles and battery electric vehicles (BEVs). The market is driven by the increasing demand for sustainable mobility solutions to meet global climate goals, the need to reduce air pollution and the rise of stringent emission regulations across key markets. Furthermore, the transition to clean energy solutions for heavy-duty applications, such as trucks, buses and material handling vehicles is further propelling the adoption of hydrogen FCVs as a viable alternative for sectors that require long range and fast refueling capabilities.

Environmental and emission reduction goals are driving significant growth in the hydrogen fuel cell vehicle (FCV) market as industries increasingly focus on decarbonization to combat climate change. Many sectors have integrated hydrogen and fuel cell technologies as part of their efforts to reduce greenhouse gas emissions. This is especially important for the transportation industry, where heavy-duty vehicles that are responsible for approximately 25% of transportation sector GHG emissions are seen as a major target for decarbonization. Hydrogen fuel cells have been identified as a promising, zero-emission alternative for these vehicles, offering long-range and quick refueling capabilities essential for commercial applications. Furthermore, the integration of hydrogen with renewable energy sources is amplifying the push toward cleaner transportation. As renewable energy production expands, hydrogen produced from these sources is becoming a critical component of the clean energy transition, supporting both fuel cell vehicle adoption and broader sustainability goals. This synergy between hydrogen fuel cell vehicles and renewable energy is positioning hydrogen as a key enabler of global efforts to achieve carbon neutrality.

Market Snapshot :

Hydrogen Fuel Cell Vehicle Market- Report Coverage:

The “Hydrogen Fuel Cell Vehicle Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Hydrogen Fuel Cell Vehicle Market.

| Attribute | Segment |

|---|---|

|

By Vehicle Type

|

|

|

By Technology

|

|

|

By Operating Miles

|

|

|

By Power Output

|

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

The Covid-19 pandemic also delayed the construction of hydrogen refueling stations. Many governments and private companies postponed investments in hydrogen infrastructure due to financial constraints or shifting priorities during the crisis.

The Russia-Ukraine war exacerbated the challenges of the hydrogen market including delays in production and rising costs of key materials like nickel and platinum, which are essential for fuel cell technology. The disruption of metals supply chains and the reallocation of resources to more urgent needs, such as defense and energy security, slowed the pace of development and deployment of hydrogen vehicles in some regions

Key Takeaways:

-

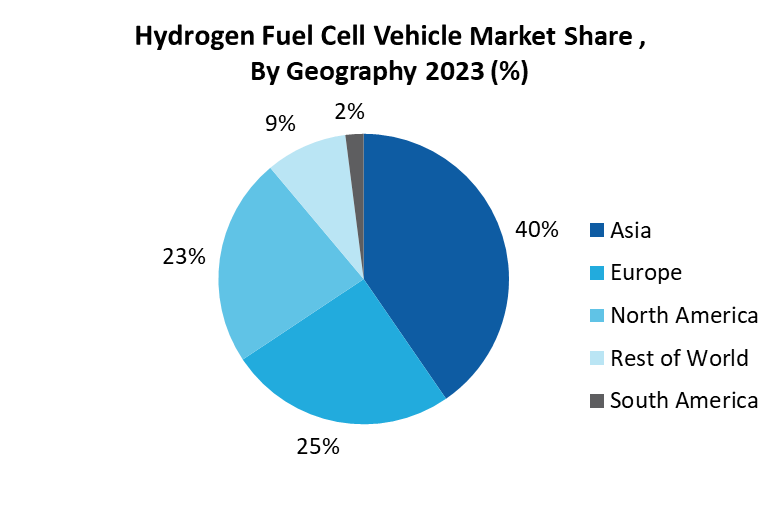

Asia is Leading the Market:

Asia accounted for largest market share in 2023, driven by technological advancements and increasing demand for sustainable transportation solutions along with fierce competition between India, Japan, and China driving rapid growth in the sector. According to a September 2024 report by Manufacturing Asia, the hydrogen fuel cell vehicle market in Asia is expected to expand from 23,000 units in 2024 to around 353,000 units by 2034. This growth is being fueled by the region's commitment to sustainable transportation and carbon reduction. A key development in this race is Japan’s strategic push in October 2024, as outlined by Hydrogen Central, where it unveiled plans to introduce a fleet of 6,000 hydrogen vehicles, positioning itself as a direct competitor to China’s massive electric vehicle (EV) market, dominated by giants like BYD. While China has aggressively pursued EV growth, Japan is betting on hydrogen as a viable alternative, aiming to carve out a leadership role in the hydrogen fuel cell space. As these countries race to secure a foothold in the future of sustainable mobility, the hydrogen fuel cell vehicle market is poised for substantial growth.

-

Commercial Vehicles to Register the Fastest Growth

Commercial vehicles are poised to register the fastest growth in the hydrogen fuel cell vehicle (FCV) market, largely driven by government policies aimed at reducing emissions in the transportation sector. Governments worldwide are implementing stricter regulations and offering incentives that favor the adoption of clean energy technologies in commercial fleets, including hydrogen fuel cells. In April 2024, the U.S. Environmental Protection Agency (EPA) introduced Phase 3 Greenhouse Gas (GHG) emission standards for heavy-duty vehicles (HDVs), which cover model years 2027 to 2032. These standards target significant reductions in CO2 emissions from trucks and buses, with goals of reducing emissions by up to 60% for vocational trucks and 40% for tractor trucks by 2032. The new regulations provide manufacturers with flexibility in how they achieve these goals, allowing for the continued development of zero-emission vehicles (ZEVs) like hydrogen fuel cell-powered trucks, without requiring the mandatory sale of ZEVs. This policy shift is highly beneficial for the commercial vehicle sector as it encourages manufacturers to explore alternative powertrains, such as hydrogen fuel cells, to meet these ambitious emissions reduction targets. Hydrogen FCVs offer distinct advantages for commercial applications, particularly in heavy-duty transport, where longer range and quick refueling times are essential.

-

Proton Exchange Membrane Fuel Cell is Leading the Market

Proton Exchange Membrane Fuel Cells (PEMFCs), also known as Polymer Electrolyte Membrane (PEM) fuel cells, are leading the market due to their high efficiency, compact size, and versatility, making them ideal for use in a variety of applications, especially in hydrogen fuel cell vehicles. PEM fuel cells offer several advantages, including rapid start-up times, low operating temperatures, and a relatively straightforward design, which have made them the preferred choice for automotive manufacturers and industries focused on reducing emissions. In November 2024, US electrolyzer manufacturer Electric Hydrogen announced that it would supply 200 MW of its PEM electrolysers for Uniper’s gigawatt-scale Wilhelmshaven green hydrogen project in northern Germany. The integration of PEM technology in both the production and utilization of hydrogen positions it as a critical enabler of the hydrogen economy. Additionally, major automotive companies are advancing the development of PEM fuel cell technology for commercial vehicles. In January 2024, Hyundai Motor, Kia Corporation, and W. L. Gore & Associates signed a partnership at the Mabuk Eco-Friendly R&D Center in Korea to collaborate on the development of advanced PEM for hydrogen fuel cell systems. The goal is to create next-generation PEMs for fuel cell electric commercial vehicles, which will offer enhanced performance, durability, and cost-effectiveness, further solidifying the position of PEM technology as the leading fuel cell solution in the market.

-

Reduction in Hydrogen Production Costs Drives the Market

As the cost of hydrogen continues to decrease, it becomes more accessible for a variety of applications including fuel cell vehicles. This trend is largely driven by technological advancements, economies of scale and supportive government incentives. For instance, a March 2024 article by the Institute for Energy Economics and Financial Analysis highlights that the levelized cost of green hydrogen in India is expected to fall by up to 40%, bringing the cost down to US$3-3.75/kg with the support of government incentives. This significant reduction in hydrogen production costs is crucial for making hydrogen fuel cell vehicles more economically viable, especially in emerging markets like India, where demand for clean transportation solutions is growing. Additionally, ZeroAvia announced in July 2024 that it has developed a revolutionary AI-driven, scalable smart microgrid optimization software designed to minimize the cost of hydrogen production. Such technological advancement will not only enhance the efficiency of hydrogen production but also contribute to further cost reduction enabling the widespread adoption of hydrogen as a clean energy source for both aviation and road transport.

-

Hydrogen Production and Storage to Hamper the Market

While hydrogen is a promising alternative fuel, its production, storage and transportation involve complex processes that require technological advancements and careful handling. One of the main challenges is the energy-intensive nature of hydrogen production, especially green hydrogen, which relies on renewable energy sources to split water into hydrogen and oxygen. Additionally, hydrogen storage poses a critical challenge due to the need for high-pressure tanks or cryogenic systems to store hydrogen safely and efficiently. These tanks must be able to withstand extreme conditions while maintaining the hydrogen at a pressure that allows it to be used effectively in fuel cell vehicles. An example of these storage challenges surfaced in September 2024, when Ecotias.com reported that many Hyundai Nexo cars in South Korea were found to have leaking hydrogen tanks. The Korean Transportation Safety Authority (KOTAS) reported approximately 2,277 incidents involving leaks between 2020 and September 2024. Such leaks are particularly dangerous because hydrogen is highly explosive and can lead to fires or explosions when contained in a sealed environment with a heat source.

For more details on this report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Hydrogen Fuel Cell Vehicle Market. The top 10 companies in this industry are listed below:

- Volkswagen Group

- Ballard Power System Inc

- BMW Group

- Mercedes-Benz Group AG

- Volvo AB

- General Motor Company

- Honda Motor Co, Ltd

- Hyundai Motor Group

- MAN SE

- Toyota Motor Corporation

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

38.9% |

|

Market Size in 2030 |

$15.2 billion |

|

Segments Covered |

By Vehicle Type, By Technology, By Operating Miles, By Power Output and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, , Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

For more Automotive Market reports, please click here

LIST OF TABLES

1.Global Hydrogen Fuel Cell Vehicle Market By Vehicle Type Market 2023-2030 ($M)

1.1 Passenger Vehicle Market 2023-2030 ($M) - Global Industry Research

1.1.1 And Opportunity Market 2023-2030 ($M)

1.2 Commercial Vehicle Market 2023-2030 ($M) - Global Industry Research

2.Global Hydrogen Fuel Cell Vehicle Market By Technology Market 2023-2030 ($M)

2.1 Proton Exchange Membrane Fuel Cell Market 2023-2030 ($M) - Global Industry Research

2.2 Phosphoric Acid Fuel Cell Market 2023-2030 ($M) - Global Industry Research

3.Global Hydrogen Fuel Cell Vehicle Market By Vehicle Type Market 2023-2030 (Volume/Units)

3.1 Passenger Vehicle Market 2023-2030 (Volume/Units) - Global Industry Research

3.1.1 And Opportunity Market 2023-2030 (Volume/Units)

3.2 Commercial Vehicle Market 2023-2030 (Volume/Units) - Global Industry Research

4.Global Hydrogen Fuel Cell Vehicle Market By Technology Market 2023-2030 (Volume/Units)

4.1 Proton Exchange Membrane Fuel Cell Market 2023-2030 (Volume/Units) - Global Industry Research

4.2 Phosphoric Acid Fuel Cell Market 2023-2030 (Volume/Units) - Global Industry Research

5.North America Hydrogen Fuel Cell Vehicle Market By Vehicle Type Market 2023-2030 ($M)

5.1 Passenger Vehicle Market 2023-2030 ($M) - Regional Industry Research

5.1.1 And Opportunity Market 2023-2030 ($M)

5.2 Commercial Vehicle Market 2023-2030 ($M) - Regional Industry Research

6.North America Hydrogen Fuel Cell Vehicle Market By Technology Market 2023-2030 ($M)

6.1 Proton Exchange Membrane Fuel Cell Market 2023-2030 ($M) - Regional Industry Research

6.2 Phosphoric Acid Fuel Cell Market 2023-2030 ($M) - Regional Industry Research

7.South America Hydrogen Fuel Cell Vehicle Market By Vehicle Type Market 2023-2030 ($M)

7.1 Passenger Vehicle Market 2023-2030 ($M) - Regional Industry Research

7.1.1 And Opportunity Market 2023-2030 ($M)

7.2 Commercial Vehicle Market 2023-2030 ($M) - Regional Industry Research

8.South America Hydrogen Fuel Cell Vehicle Market By Technology Market 2023-2030 ($M)

8.1 Proton Exchange Membrane Fuel Cell Market 2023-2030 ($M) - Regional Industry Research

8.2 Phosphoric Acid Fuel Cell Market 2023-2030 ($M) - Regional Industry Research

9.Europe Hydrogen Fuel Cell Vehicle Market By Vehicle Type Market 2023-2030 ($M)

9.1 Passenger Vehicle Market 2023-2030 ($M) - Regional Industry Research

9.1.1 And Opportunity Market 2023-2030 ($M)

9.2 Commercial Vehicle Market 2023-2030 ($M) - Regional Industry Research

10.Europe Hydrogen Fuel Cell Vehicle Market By Technology Market 2023-2030 ($M)

10.1 Proton Exchange Membrane Fuel Cell Market 2023-2030 ($M) - Regional Industry Research

10.2 Phosphoric Acid Fuel Cell Market 2023-2030 ($M) - Regional Industry Research

11.APAC Hydrogen Fuel Cell Vehicle Market By Vehicle Type Market 2023-2030 ($M)

11.1 Passenger Vehicle Market 2023-2030 ($M) - Regional Industry Research

11.1.1 And Opportunity Market 2023-2030 ($M)

11.2 Commercial Vehicle Market 2023-2030 ($M) - Regional Industry Research

12.APAC Hydrogen Fuel Cell Vehicle Market By Technology Market 2023-2030 ($M)

12.1 Proton Exchange Membrane Fuel Cell Market 2023-2030 ($M) - Regional Industry Research

12.2 Phosphoric Acid Fuel Cell Market 2023-2030 ($M) - Regional Industry Research

13.MENA Hydrogen Fuel Cell Vehicle Market By Vehicle Type Market 2023-2030 ($M)

13.1 Passenger Vehicle Market 2023-2030 ($M) - Regional Industry Research

13.1.1 And Opportunity Market 2023-2030 ($M)

13.2 Commercial Vehicle Market 2023-2030 ($M) - Regional Industry Research

14.MENA Hydrogen Fuel Cell Vehicle Market By Technology Market 2023-2030 ($M)

14.1 Proton Exchange Membrane Fuel Cell Market 2023-2030 ($M) - Regional Industry Research

14.2 Phosphoric Acid Fuel Cell Market 2023-2030 ($M) - Regional Industry Research

LIST OF FIGURES

1.US Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

2.Canada Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

3.Mexico Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

4.Brazil Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

5.Argentina Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

6.Peru Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

7.Colombia Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

8.Chile Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

9.Rest of South America Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

10.UK Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

11.Germany Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

12.France Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

13.Italy Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

14.Spain Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

15.Rest of Europe Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

16.China Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

17.India Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

18.Japan Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

19.South Korea Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

20.South Africa Hydrogen Fuel Cell Vehicle Market Revenue, 2023-2030 ($M)

21.North America Hydrogen Fuel Cell Vehicle By Application

22.South America Hydrogen Fuel Cell Vehicle By Application

23.Europe Hydrogen Fuel Cell Vehicle By Application

24.APAC Hydrogen Fuel Cell Vehicle By Application

25.MENA Hydrogen Fuel Cell Vehicle By Application

26.Audi Ag, Sales /Revenue, 2015-2018 ($Mn/$Bn)

27.Ballard Power System Inc, Sales /Revenue, 2015-2018 ($Mn/$Bn)

28.Bmw Group, Sales /Revenue, 2015-2018 ($Mn/$Bn)

29.Daimler Ag, Sales /Revenue, 2015-2018 ($Mn/$Bn)

30.General Motor Company, Sales /Revenue, 2015-2018 ($Mn/$Bn)

31.Honda Motor Co , Ltd, Sales /Revenue, 2015-2018 ($Mn/$Bn)

32.Hyundai Motor Group, Sales /Revenue, 2015-2018 ($Mn/$Bn)

33.Man Se, Sales /Revenue, 2015-2018 ($Mn/$Bn)

34.Toyota Motor Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

35.Volvo, Sales /Revenue, 2015-2018 ($Mn/$Bn)

The Hydrogen Fuel Cell Vehicle Market is projected to grow at 38.9% CAGR during the forecast period 2024-2030.

The Hydrogen Fuel Cell Vehicle Market size is estimated to be $1.5 billion in 2023 and is projected to reach $15.2 billion by 2030.

The leading players in the Hydrogen Fuel Cell Vehicle Market are Volkswagen Group, Ballard Power System Inc, BMW Group, Mercedes-Benz Group AG, Volvo AB and Others.

Hydrogen integration with renewable energy, environmental and emission reduction goals are some of the major hydrogen fuel cell vehicle market trends in the industry which will create growth opportunities for the market during the forecast period.

Key driving factors include rising demand for sustainable transportation, improvements in energy efficiency and driving range, government incentives and advancements in hydrogen production and infrastructure.