Email

Email Print

Print

KSA IT Distribution Market – Operating Model , By End Use Industry , By Mobility and Computing Solutions , By Productivity and Peripheral Solutions , By Network Solution , By Other Solutions

KSA IT Distribution Market Overview:

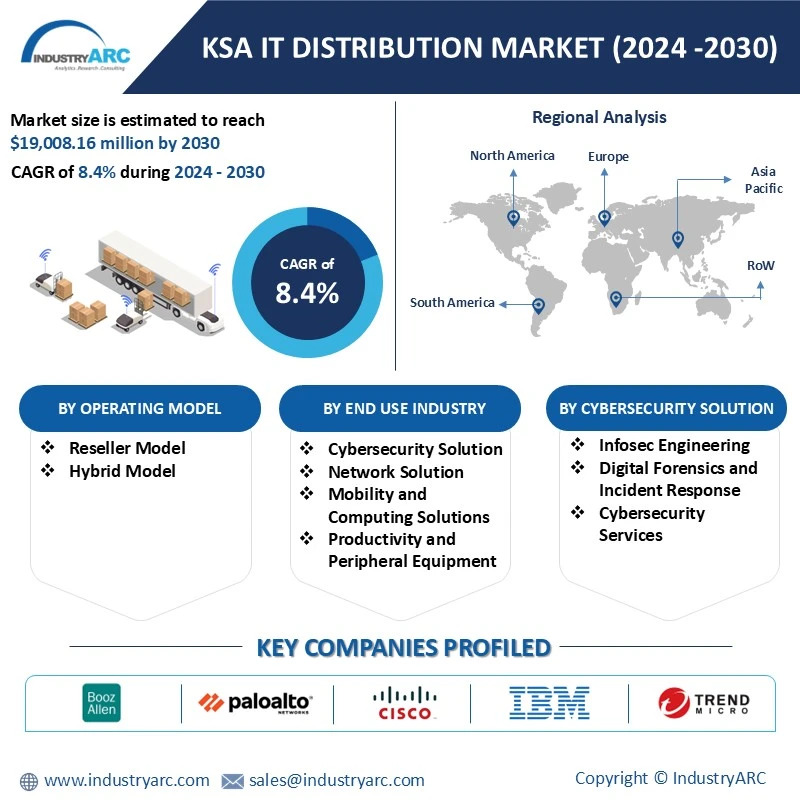

KSA IT Distribution Market size is estimated to reach $19,008.16 million by 2030, growing at a CAGR of 8.4% during the forecast period 2024-2030. The Kingdom of Saudi Arabia (KSA) IT Distribution Market is experiencing robust growth driven by digital transformation initiatives, government investments in technology, and the increasing demand for IT solutions across various sectors. As businesses and government entities prioritize technological advancements, the demand for hardware, software, and IT services is surging. Key players in the market include both local and international distributors, who are expanding their portfolios to include cutting-edge technologies such as cloud computing, cybersecurity, and artificial intelligence. The rise of e-commerce and remote work has further accelerated the adoption of IT products and services, creating lucrative opportunities for distributors. Moreover, the KSA government's Vision 2030 initiative aims to diversify the economy and enhance the digital infrastructure, providing a favorable environment for IT distribution. Challenges, however, include intense competition, evolving customer preferences, and the need for distributors to adapt to rapid technological changes. Overall, the KSA IT Distribution Market presents significant opportunities for growth and innovation, positioning itself as a pivotal player in the Middle East's technology landscape.

Market Snapshot:

KSA IT Distribution Market - Report Coverage:

The “KSA IT Distribution Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the KSA IT Distribution Market.

| Attribute | Segment |

|---|---|

|

By Operating Model |

|

|

By End Use Industry |

|

|

By Cybersecurity Solution |

|

|

By Mobility and Computing Solutions |

|

|

By Productivity and Peripheral Solutions |

|

|

By Network Solution |

|

|

By Other Solutions |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic significantly impacted the KSA IT Distribution Market, leading to supply chain disruptions and decreased demand from sectors like cosmetics and hospitality. However, the rise in personal care and hygiene awareness boosted petroleum jelly sales, particularly for its moisturizing and protective properties. The market is gradually recovering as economic activities resume and consumer preferences evolve.

- The Ukraine crisis has affected the KSA IT Distribution Market by causing supply chain disruptions and increasing prices for IT products due to shortages of raw materials and components. Additionally, geopolitical tensions have heightened concerns around cybersecurity, leading to increased demand for security solutions. This situation has prompted distributors to diversify their sources and enhance their service offerings to mitigate risks.

Key Takeaways:

-

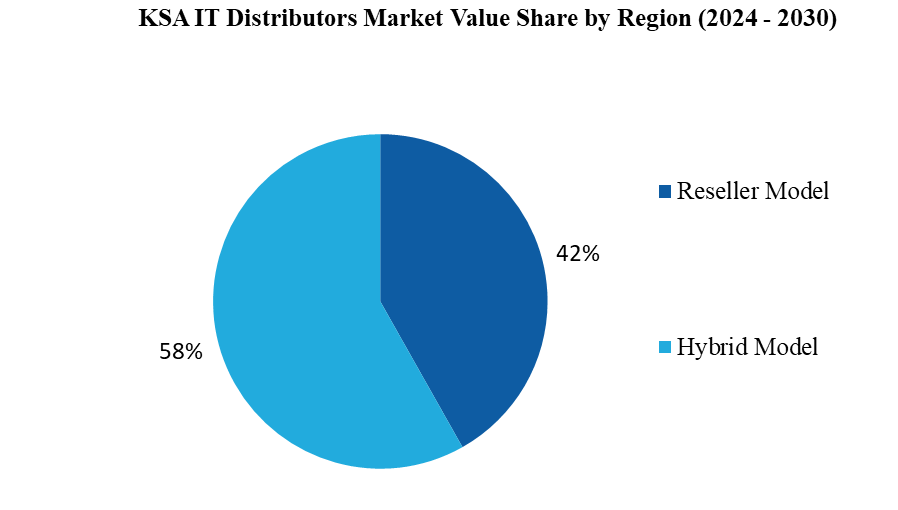

Hybrid Model Segment is Leading the Market

In the KSA IT Distributors Market, the Hybrid Model segment is currently dominating, capturing the majority of market share. This model combines elements of both traditional reseller and direct sales approaches, allowing distributors to effectively cater to a diverse range of customer needs. The hybrid strategy enables distributors to maintain strong relationships with vendors while also offering tailored solutions to end-users. One of the primary advantages of the Hybrid Model is its flexibility, which allows distributors to adapt to changing market demands and customer preferences. By leveraging both resale and direct sales, distributors can enhance their product offerings, streamline procurement processes, and improve customer service. This adaptability is particularly crucial in a rapidly evolving technological landscape, where businesses increasingly seek integrated solutions that align with their digital transformation goals. Moreover, the Hybrid Model facilitates a more efficient supply chain, enabling distributors to optimize inventory management and respond swiftly to market fluctuations. As the KSA government pushes for digitalization under Vision 2030, the Hybrid Model is well-positioned to support the growing demand for innovative IT solutions, thereby reinforcing its dominance in the market.

-

AI Segment to Register Highest Growth

In the segmentation of the KSA IT Distributors Market by end-use industry, the Artificial Intelligence (AI) sector is witnessing the fastest growth. This surge is primarily driven by the increasing adoption of AI technologies across various industries, including finance, healthcare, retail, and logistics. Organizations are recognizing the potential of AI to enhance operational efficiency, improve decision-making, and deliver personalized customer experiences. As businesses in Saudi Arabia embrace digital transformation, the demand for AI-driven solutions such as machine learning, natural language processing, and data analytics is rapidly increasing. This trend is supported by government initiatives aimed at fostering innovation and technological advancement as part of the Vision 2030 agenda. For instance, in February 2024, SAS, a global leader in data and AI, formed a strategic partnership with Redington, a multibillion-dollar technology distributor, to expand its presence in the Middle East, Africa, and Turkey. AI's ability to automate processes and analyze vast amounts of data positions it as a critical asset for organizations seeking competitive advantages. Consequently, IT distributors are prioritizing partnerships with AI technology providers to expand their offerings and meet the growing market demand. This focus on AI not only enhances distributors' value propositions but also aligns with the broader economic diversification efforts in the Kingdom, solidifying AI's position as a key growth driver in the KSA IT Distributors Market.

-

Increasing Demand Digital Transformation Across Various Sectors is a Major Driver

A major driver of the KSA IT Distributors Market is the ongoing digital transformation across various sectors. As businesses and government entities in Saudi Arabia increasingly embrace technology to enhance operational efficiency and drive innovation, the demand for IT solutions is surging. This trend is bolstered by the Kingdom’s Vision 2030 initiative, which emphasizes economic diversification and the development of a robust digital infrastructure. The rising adoption of cloud computing, big data analytics, and cybersecurity solutions further fuels market growth. Organizations recognize the need for secure and scalable IT environments to support their operations and protect sensitive information. As a result, distributors are expanding their portfolios to include cutting-edge technologies and services that address these emerging needs. Moreover, the growing awareness of the importance of digitalization, particularly following the COVID-19 pandemic, has accelerated investments in IT. Companies are actively seeking innovative solutions to streamline processes and enhance customer engagement. This shift not only creates opportunities for IT distributors to expand their market share but also positions them as critical enablers of the Kingdom’s technological advancement and economic growth.

-

Intense Competition is a Major Challenge

A major challenge in the KSA IT Distributors Market is the intense competition among distributors. The market is characterized by a growing number of players, including both local distributors and established international firms. This heightened competition drives price wars and forces distributors to constantly innovate their service offerings to maintain market share. As companies increasingly seek comprehensive IT solutions, distributors must differentiate themselves not only through pricing but also through value-added services, such as technical support, consulting, and customized solutions. This demand for differentiation adds pressure on distributors to invest in training and development to enhance their technical expertise and customer service capabilities. Moreover, the rapid evolution of technology necessitates that distributors stay abreast of industry trends and emerging technologies. Failure to adapt to changing market dynamics can result in losing competitive advantage and potential market share. To thrive in this competitive landscape, IT distributors must prioritize strategic partnerships with technology providers, focus on customer relationships, and continuously innovate to meet the evolving needs of their clients, ensuring they remain relevant and competitive in the marketplace.

For more details on this report - Request for Sample

Key Market Players:

Product launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the KSA IT Distribution Market. The top 10 companies in this industry are listed below:

- TrendMicro

- IBM

- Cisco

- Palo Alto Network

- Booz Allen Hamilton

- Trellix

- Broadcom

- Darktrace

- SentinelOne

- Fortinet

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

8.4% |

|

Market Size in 2030 |

$19,008.16 million |

|

Segments Covered |

By Operating Model, By End Use Industry, By Cybersecurity Solution, By Mobility and Computing Solutions, By Productivity and Peripheral Solutions, By Network Solution, By Other Solutions. |

|

Key Market Players |

|

For more Information and Communications Technology Market reports, please click here

The KSA IT Distribution Market is projected to grow at 8.4% CAGR during the forecast period 2024-2030.

KSA IT Distribution Market size is estimated to surpass $19,008.16 million by 2030 from $10,797.7 million in 2023

The leading players in the KSA IT Distribution Market are TrendMicro, IBM, Cisco, Palo Alto Network, Booz Allen Hamilton and Others.

Major trends shaping the KSA IT Distributors Market include the rise of cloud computing and artificial intelligence, driving demand for innovative IT solutions. Additionally, increased focus on cybersecurity will push distributors to enhance their offerings. The adoption of e-commerce platforms and digital channels for sales and customer engagement will also play a crucial role in redefining distribution strategies in the region.

Driving factors in the KSA IT Distributors Market include government initiatives promoting digital transformation, increasing demand for advanced IT solutions, and the rapid adoption of cloud technologies. Opportunities lie in expanding cybersecurity services, catering to the growing AI sector, and leveraging e-commerce platforms for distribution. Additionally, partnerships with technology vendors can enhance service offerings and meet evolving customer needs.