Email

Email Print

Print

Marine Decarbonization Market - By Potential Addressable (TAM, SAM, SOM), By Sector (Marine Fuel {Liquefied Natural Gas (LNG), Biofuels, Hydrogen, Ammonia, Methanol, Synthetic Fuels}, Engine Manufacturing , Ship Building {Energy – Efficient Hull Designs, Lightweight Materials, Advanced Propulsion Systems}, MRO Port Operation), By Technology Addressable , By Risk Assessment ) and By Geography - Opportunity Analysis & Industry Forecast, 2024-2030

Marine Decarbonization Market Overview:

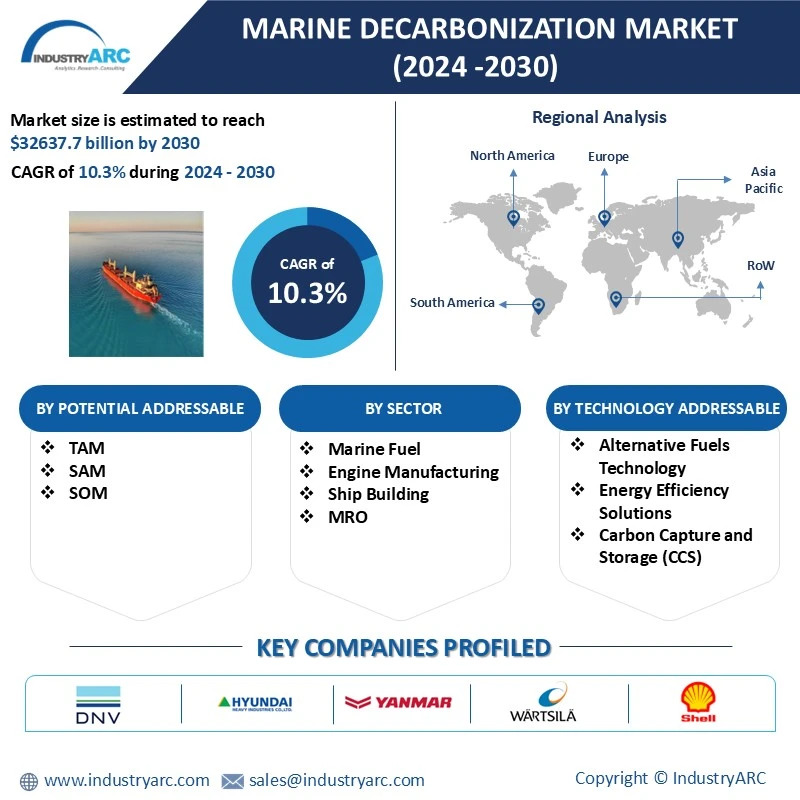

The Marine Decarbonization Market size is estimated to reach $32637.7 Billion by 2030, growing at a CAGR of 10.3% during the forecast period 2024-2030. Rising regulatory pressure to reduce carbon emissions, coupled with the adoption of sustainable shipping practices and alternative fuels, is driving significant growth in the Marine Decarbonization market. Technological advancements such as energy-efficient propulsion systems, carbon capture technologies, and hybrid-electric engines, as well as increasing investments in green shipping infrastructure and renewable energy solutions, further contribute to this market's expansion.

Integration of Carbon Capture and Storage (CCS) Technology

The increasing focus on reducing greenhouse gas (GHG) emissions in the maritime sector increased the adoption of carbon capture and storage (CCS) technology as a viable solution. CCS systems capture emissions directly from ship exhausts, preventing them from entering the atmosphere, and storing them securely to minimize environmental impact. Advancements in compact and energy-efficient CCS systems have made them suitable for maritime applications, encouraging their integration into new and existing vessels. Additionally, government initiatives, financial incentives, and pilot projects are accelerating the deployment of CCS technology. As the shipping industry seeks innovative methods to comply with global emission regulations, the growing use of CCS technology drives the demand for the maritime decarbonization market. For Instance, in December 2024, Langh Tech launched its onboard carbon capture system, featuring efficient CO₂ capture from ship exhaust, to cater to the rising demand for Carbon Capture and Storage (CCS) Technology.

Market Snapshot:

Marine Decarbonization Market - Report Coverage:

The “Marine Decarbonization Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Marine Decarbonization Market.

|

Attribute |

Segment |

|

By Potential Addressable |

|

|

By Sector |

|

|

By Technology Addressable

|

|

|

By Application Addressable

|

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

The COVID-19 pandemic had a profound impact on the global maritime and shipping industry, significantly affecting the Marine Decarbonization market. The sudden disruption in international trade led to a reduction in shipping activities, delaying investments and progress in green technologies and decarbonization initiatives. Supply chain interruptions and the closure of shipyards hindered the development and installation of energy-efficient solutions and alternative fuels. Additionally, the financial strain caused by the pandemic led to a temporary slowdown in the adoption of carbon-reduction technologies. However, the recovery phase has seen a resurgence in sustainability efforts, with the industry now focused on accelerating decarbonization goals to align with global environmental targets.

The Russia-Ukraine war has had a profound impact on the global energy industry, particularly affecting the Marine Decarbonization market. Russia, a major supplier of fossil fuels, including natural gas and oil, plays a crucial role in global energy markets. The war has led to energy supply disruptions and price volatility, prompting shipping companies to reevaluate their fuel consumption and explore alternative, lower-carbon fuel options. This uncertainty has accelerated the interest in renewable energy and alternative fuels such as hydrogen and ammonia to reduce reliance on fossil fuels. Additionally, the war has intensified pressure on the shipping industry to enhance sustainability, driving growth in the marine decarbonization market.

Key Takeaways:

Europe Leads the Market

Europe’s dominance in the Marine Decarbonization market with a market share of 32.8%. Europe, particularly the Western Region, is home to major shipping and maritime companies like Maersk, CMA CGM, and Hapag-Lloyd, and key clean energy manufacturers such as Siemens Energy, a leader in sustainable power solutions. These companies have substantial research and development investments that position Europe as a central hub for green fuel production. Additionally, investment from government subsidies and incentives boost the sustainable maritime industry. In response to the European Union’s stringent environmental regulations and the Green Deal, maritime companies are accelerating their shift toward zero-emission shipping technologies. Therefore, these factors collectively make Europe the dominant region in the Marine Decarbonization market, ensuring it remains a global leader in advanced carbon capture, alternative fuels, and emission-reduction technologies.

Marine fuel sector dominates the market.

The marine fuel sector dominates the Marine Decarbonization market, primarily due to its widespread use in shipping and transport industries, where fuel is essential for powering vessels across global trade routes. The demand for marine fuels, particularly conventional fuels like heavy fuel oil (HFO) and marine diesel oil (MDO), remains high despite the push for decarbonization. However, as the industry faces mounting pressure to meet international emissions reduction targets, shifting toward alternative fuels such as liquefied natural gas (LNG), ammonia, hydrogen, and biofuels. These low-carbon and carbon-neutral alternatives are driving growth in the sector, as maritime operators seek to comply with regulations such as the IMO 2030 and IMO 2050 decarbonization goals. Therefore, the marine fuel sector remains the largest contributor to the market thus propelling the market.

Alternative fuels technology dominates the market

Alternative fuels technology has revolutionized the marine shipping industry, offering a sustainable solution to reduce greenhouse gas emissions and dependency on traditional fossil fuels. With the maritime sector being one of the largest contributors to global carbon emissions, the shift toward low-carbon and zero-emission fuels such as LNG, hydrogen, ammonia, and biofuels is crucial for meeting international climate goals. These alternative fuels significantly reduce CO2 emissions and support the transition to greener maritime operations. Additionally, advancements in fuel production technologies and the growing availability of green fuels are making them increasingly cost-effective and accessible for shipowners. As environmental regulations tighten, alternative fuel technology is driving innovation and growth in the marine decarbonization market.

Technological Advancements in Alternative Fuels

Advancements in alternative fuels such as LNG, hydrogen, ammonia, and biofuels are transforming the maritime industry by offering cleaner and more sustainable options compared to traditional marine fuels. These fuels significantly lower CO2 emissions, reducing the environmental impact of global shipping. Continuous research and development efforts are improving fuel production processes, storage systems, and integration technologies, making these alternatives more efficient and accessible for shipowners. Breakthroughs in green hydrogen production, alongside advancements in biofuel refinement, are also helping to drive down costs, making these sustainable options increasingly viable. As the shipping industry shifts toward greener solutions, the growing adoption of alternative fuels is playing a key role in the global marine decarbonization movement, propelling the transition to sustainable maritime operations.

High Cost of Transition

The high cost of transition to cleaner technologies is one of the most significant challenges in the marine decarbonization market. Shipowners face considerable expenses when retrofitting existing vessels with new, more sustainable fuel systems or when purchasing new vessels designed to run on alternative fuels such as hydrogen, ammonia, or LNG. The infrastructure required for producing, storing, and distributing these low-carbon fuels is still in its early stages and requires substantial investment. This makes it particularly difficult for smaller operators to adopt these green technologies, as they lack the resources to manage the high upfront costs. Without adequate financial incentives, government support, or subsidies, the transition to cleaner maritime practices may be delayed, limiting progress toward global decarbonization goals in the shipping industry.

Key Market Players:

The top 10 companies in this industry are listed below:

- Royal Dutch Shell PLC

- Wartsila Corporation

- Yanmar

- Hyundai Heavy Industries (HHI)

- DNV

- MAN Energy Solutions

- Rolls Royce Marine

- ABB Marine

- Chevron

- MHI

- Others

Scope of the Report:

|

Report Metric |

Details |

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

10.3% |

|

Market Size in 2030 |

$32637.7 Billion |

|

Segments Covered |

By Potential Addressable, By Sector, By Technology Addressable, By Application Addressable, and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Denmark, Netherlands and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Thailand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

1.Marine Decarbonization Market - Overview

1.1.Definitions and Scope

2.Marine Decarbonization Market - Executive Summary

2.2.Key trends by Sector

2.3.Key trends by Technology Addressable

2.1.Key trends by Potential Addressable

2.4.Key trends by Application

2.5.Key trends by Geography

3.Marine Decarbonization Market - Comparative Analysis

3.1.Company Benchmarking - Key Companies

3.2.Financial Analysis - Key Companies

3.3.Market Share Analysis - Key Companies

3.4.Patent Analysis

3.5.Pricing Analysis

4.Marine Decarbonization Market - Start-up Companies Scenario

4.1.Key Start-up Company Analysis by

4.1.1.Investment & Revenue

4.1.2.Venture Capital and Funding Scenario

5.Marine Decarbonization Market – Market Entry Scenario Premium

5.1.Regulatory Framework Overview

5.2.New Business and Ease of Doing Business Index

5.3.Case Studies of Successful Ventures

6.Marine Decarbonization Market - Forces

6.1.Market Drivers

6.2.Market Constraints

6.3.Market Challenges

6.4.Porter's Five Force Model

6.4.1.Bargaining Power of Suppliers

6.4.2.Bargaining Powers of Customers

6.4.3.Threat of New Entrants

6.4.4.Rivalry Among Existing Players

6.4.5.Threat of Substitutes

7.Marine Decarbonization Market – Strategic Analysis

7.1.Value Chain Analysis

7.2.Opportunities Analysis

7.3.Product Life Cycle/Market Life Cycle Analysis

7.4.Supplier/Distributor Analysis

8.Marine Decarbonization Market – By Potential Addressable (Market Size – $Million/$Billion)

8.1.TAM

8.2.SAM

8.3.SOM

9.Marine Decarbonization Market– By Sector (Market Size – $Million/$Billion)

9.1.Marine Fuel

9.1.1. Liquefied Natural Gas (LNG)

9.1.2. Biofuels

9.1.3. Hydrogen

9.1.4. Ammonia

9.1.5. Methanol

9.1.6. Synthetic Fuels

9.2.Engine Manufacturing

9.2.1. Duel – Fuel Engines

9.2.2. Electric Propulsion Systems

9.2.3. Hybrid Propulsion Systems

9.2.4. Fuel Cell Systems

9.3.Ship Building

9.3.1. Energy – Efficient Hull Designs

9.3.2. Lightweight Materials

9.3.3. Advanced Propulsion Systems

9.4.MRO

9.4.1. Predictive Maintenance

9.4.2. Retrofitting for Decarbonization

9.5.Vessel Operation

9.5.1. Predictive Maintenance

9.5.2. Energy Management Systems

9.6.Port Operation

9.6.1. Shore Power

9.6.2. Green Infrastructure

9.6.3. Digital Port Management

10.Marine Decarbonization Market– By Technology Addressable (Market Size – $Million/$Billion)

10.1.Alternative Fuels Technology

10.2.Energy Efficient Solutions

10.3.Carbon Capture and Storage (CCS)

10.4.Digital Solutions for Monitoring and Optimization

10.5.Battery Technology

10.6.Fuel Cell Technology

11.Marine Decarbonization Market– By Application Addressable (Market Size – $Million/$Billion)

11.1.Commercial Shipping

11.2.Offshore Support Vessels (OSVs)

11.3.Passenger and Cruise Ships

11.4.Naval and Defense Applications

11.5.Others

12.Marine Decarbonization Market – by Geography (Market Size – $Million/$Billion)

12.1.North America

12.1.1.U.S

12.1.2.Canada

12.1.3.Mexico

12.2.Europe

12.2.1.Germany

12.2.2.France

12.2.3.UK

12.2.4.Italy

12.2.5.Spain

12.2.6.Russia

12.2.7.Rest of Europe

12.3.Asia-Pacific

12.3.1.China

12.3.2.Japan

12.3.3.South Korea

12.3.4.India

12.3.5.Australia & New Zealand

12.3.6.Rest of Asia-Pacific

12.4. South America

12.4.1.Brazil

12.4.2.Argentina

12.4.3.Chile

12.4.4.Colombia

12.4.5.Rest of South America

12.5.Rest of The World

12.5.1.Middle East

12.5.2.Africa

13.Marine Decarbonization Market – Entropy

13.1.New product launches

13.2.M&A's, collaborations, JVs and partnerships

14.Marine Decarbonization Market – Industry/Segment Competition Landscape

14.1.Market Share Analysis

14.1.1.Market Share by Global

14.1.2.Market Share by Region

14.1.3.Market Share by Country

15.Marine Decarbonization Market – Key Company List by Country Premium

16.Marine Decarbonization Market – Company Analysis

16.1.A.P. Moller – Maersk

16.2.Wartsila Corporation

16.3.Royal Dutch Shell PLc

16.4.Hyundai Heavy Industries (HHI)

16.5.MAN Energy Solutions

16.6.Company 6

16.7.Company 7

16.8.Company 8

16.9.Company 9

16.10.Company 10