Email

Email Print

Print

Mining Services Market – By Mining Type, By Services, By Geography - Opportunity Analysis & Industry Forecast, 2024-2030

Mining Services Market Overview:

The Mining Services Market size is estimated to reach $ 389169.7 Million by 2030, growing at a CAGR of 5.5% during the forecast period 2024-2030. Mining services are increasingly focused on sustainability as companies seek to reduce their carbon footprints. Implementing renewable energy solutions, improving energy efficiency, and minimizing waste are central to this shift. This trend is driven by regulatory pressures and rising stakeholder demand for greener operations, reshaping the mining sector towards more responsible and eco-friendly practices.

The mining services market is embracing digitalization through automation, AI, and data analytics to enhance efficiency and reduce operational costs. Advanced technologies like autonomous vehicles, drones, and sensors streamline operations, enabling real-time monitoring and predictive maintenance, which improves safety and productivity across mining projects. These factors positively influence the Mining Services industry outlook during the forecast period.

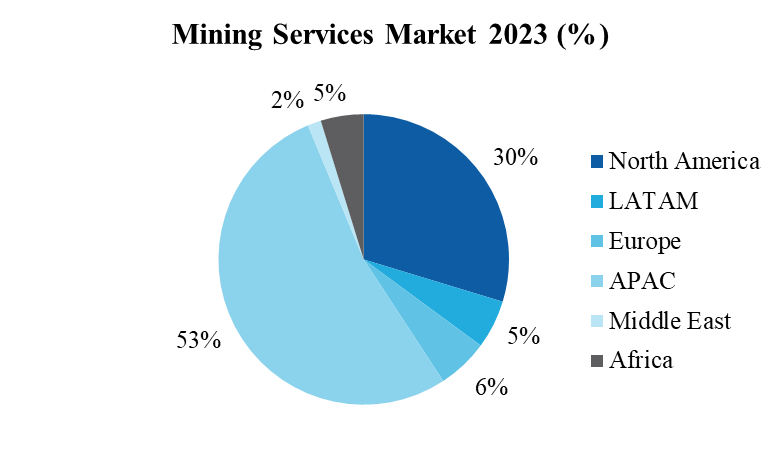

Market Snapshot:

Mining Services Market - Report Coverage:

The “Mining Services Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Mining Services Market.

| Attribute | Segment |

|---|---|

|

By Mining Type |

|

|

By Services |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic disrupted global mining services by causing delays in operations, supply chain bottlenecks, and labor shortages. This led to project delays and increased costs as companies adjusted to new health regulations and workforce restrictions. Additionally, digital transformation accelerated as firms sought automation solutions to maintain productivity while minimizing human contact. Despite these challenges, the sector showed resilience through adaptability and a focus on innovation to sustain service offerings.

- The Ukraine crisis impacted mining services by exacerbating supply chain challenges, particularly in securing critical materials and fuel supplies. This increased operational costs and forced companies to reassess sourcing strategies and energy dependencies. Additionally, heightened uncertainty led to cautious investment strategies and disruptions in project timelines. To counter these effects, mining services firms focused on operational efficiency, exploring alternative supply routes, and diversifying partnerships to mitigate potential risks.

Key Takeaways:

Middle East Region is Projected as Fastest Growing Region

Middle East is projected as the fastest growing region in Mining Services Market with CAGR of 7.1% during the forecast period 2024-2030. The Middle East's demand for mining services is growing as countries diversify their economies. Saudi Arabia estimates its mineral wealth at $2.5 trillion as per Saudi Arabian Government, highlighting significant reserves of phosphates, metals, and other resources. Specialized services in exploration, drilling, and maintenance are increasingly needed. Technological innovations like digitalization and automation are improving efficiency, while sustainable practices are being prioritized. Governments are supporting this growth through favorable regulations and infrastructure development. As a result, the region is becoming a hub for mining services, contributing to economic diversification beyond oil.

Metal Segment to Register the Fastest Growth

Metal segment is projected as the fastest growing segment in Mining Services Market with CAGR of 6.9% during the forecast period 2024-2030. The metal sector within the mining services market is driven by rising demand from industries such as construction, automotive, and renewable energy. Innovations in extraction technologies, along with an emphasis on sustainable mining practices, further boost this demand. Additionally, increasing urbanization and infrastructure development contribute to a heightened need for various metals, encouraging mining services to expand. The adoption of digital technologies and automation in mining operations improves efficiency, making it a critical factor in meeting industry requirements.

Mine Development and Design is Leading the Market

Mine Development and Design held the largest market valuation of $83441.0 million in 2023. The key drivers for mine development and design in the mining services market include the increasing need for sustainable mining practices and the integration of advanced technologies. Companies are adopting environmentally-friendly solutions to minimize their ecological footprint, while digital tools like 3D modeling, data analytics, and automation enhance operational efficiency and safety. For instance, Saudi Arabia plans to invest up to $15 billion in securing minerals essential for solar panels and electric vehicles in 2023, as per the International Trade Administrations. This growing demand for metals, particularly from renewable energy and electric vehicle sectors, is stimulating significant investments in mine development. Consequently, mining services providers are optimizing their design and project planning processes to align with these evolving market needs.

Growth in Renewable Energy Sectors Driving Demand for Critical Minerals

The growth in renewable energy sectors is significantly driving demand for critical minerals in the mining services market. According to the International Energy Agency, global annual renewable capacity additions surged by nearly 50%, reaching approximately 510 gigawatts (GW) in 2023, marking the fastest growth rate in two decades. This shift towards sustainable energy solutions intensifies the need for essential minerals like lithium, cobalt, and rare earth elements. These minerals are vital for producing batteries, solar panels, and wind turbines. Consequently, mining service providers are increasingly focused on optimizing extraction processes and ensuring sustainable practices to meet this rising demand while adhering to environmental standards.

Fluctuating Commodity Prices

The Mining Services Market faces significant operational challenges, primarily due to fluctuating commodity prices. These price variations can create unpredictability in project budgeting and profitability. Mining companies often struggle to align their service offerings with market demand, resulting in potential underutilization of resources. Moreover, maintaining efficient supply chains and logistics can become increasingly difficult during periods of price volatility. As companies strive to optimize their operations, they must continuously assess and adapt their strategies to mitigate risks associated with these fluctuations, ensuring they remain competitive and can meet client expectations effectively.

For more details on this report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Mining Services Market. The top 10 companies in this industry are listed below:

- CIMIC Group

- Fluor Corporation

- WSP

- L&T Construction & Mining Machinery

- Bechtel Corporation

- SGS S.A.

- Worley Limited

- Perenti

- Kintetsu World Express, Inc. (KWE)

- John Wood Group

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

5.5% |

|

Market Size in 2030 |

$ 389169.7 Million |

|

Segments Covered |

By Mining Type, By Services and By Geography. |

|

Geographies Covered |

North America (U.S. and Canada), LATAM (Chile and Peru), Europe, APAC (India and Australia), Middle East (Saudi Arabia) and Africa (South Africa) |

|

Key Market Players |

|

For more Automation and Instrumentation Market reports, please click here

The Mining Services Market is projected to grow at 5.5% CAGR during the forecast period 2024-2030.\\\\\\\\\\\\\\\\r\\\\\\\\\\\\\\\\n\\\\\\\\\\\\\\\\r\\\\\\\\\\\\\\\\n

The Mining Services Market size is estimated to be $250420.1 million in 2023 and is projected to reach $389169.7 million by 2030

The leading players in the Mining Services Market are CIMIC Group, Fluor Corporation, WSP, L&T Construction & Mining Machinery, Bechtel Corporation, and Others.

Increasing automation and digitalization are enhancing operational efficiency and safety in mining services and Demand for critical minerals is rising due to the global shift towards renewable energy and electric vehicles are some of the major Mining Services Market trends in the industry which will create growth opportunities for the market during the forecast period.\\\\\\\\\\\\\\\\r\\\\\\\\\\\\\\\\n\\\\\\\\\\\\\\\\r\\\\\\\\\\\\\\\\n

Growth in renewable energy sectors driving demand for critical minerals and Investment in Green Mining Technologies to Minimize Ecological Disturbances are the driving factors of the market.