Email

Email Print

Print

Powered Surgical Instrument Market - By Product Type , By Power Source , By Application , By End User , By Geography - Opportunity Analysis & Industry Forecast, 2024-2030.

Powered Surgical Instrument Market Overview:

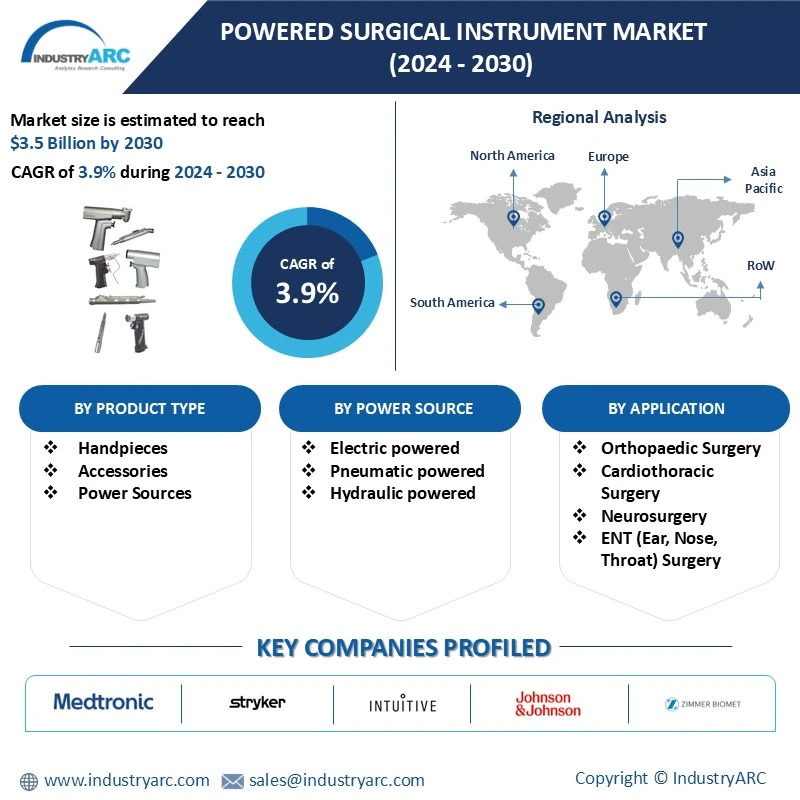

The Powered Surgical Instrument Market size is estimated to reach $3.5 billion by 2030, growing at a CAGR of 3.9% during the forecast period 2024-2030. The powered surgical instrument market is a growing sector within the broader medical device industry, driven by Technological advancements leading to more efficient and precise instruments, rising prevalence of chronic diseases and trauma injuries and increasing surgical procedures worldwide. Additionally, expanding healthcare investments also drives the powered surgical instrument market.

The growing use of robotic-assisted surgery is reshaping the powered surgical instruments market. This trend is driven because the robotic surgery systems offer precision, control, and are minimally invasive in nature. For example, the da Vinci Surgical System facilitates surgeons in performing complex procedures with enhanced accuracy, thus minimizing complications and improving patient outcomes. Robotic-assisted surgeries promise faster recovery times with smaller, less debilitating incisions and, as such, their indications are on the rise within prostatectomies, hysterectomies, and cardiac surgeries. Many new healthcare facilities have invested in advanced technologies, leading to an increased demand for powered surgical instruments compatible with robotic systems, further driving innovation within the market.

Market Snapshot:

Powered Surgical Instrument Market - Report Coverage:

The “Powered Surgical Instrument Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Powered Surgical Instrument Market.

| Attribute | Segment |

|---|---|

|

|

|

By Power Source |

|

|

By Application |

|

|

By End User |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic had a great effect on the powered surgical instrument market due to postponement of elective surgeries and disruptions to the global supply chain. Various hospitals postponed orthopedic, cardiovascular and dental surgeries in order to accommodate COVID-19 care, reducing demand for surgical instruments temporarily. Manufacturing delays and trade restrictions also weighed on supply.

- The Russia-Ukraine war significantly impacted the powered surgical instrument market by disrupting supply chains raising demand for trauma care instruments and brought economic challenges. The war agitated the manufacturing and distribution in Europe, particularly since many firms depend on Ukraine and Russia for raw materials and components.

Key Takeaways:

North America dominates the market

North America dominated the Powered Surgical Instrument Market in 2023. North America remained as a significant contributor to the powered surgical instrument market, followed by the United States. The region has several mature healthcare systems with a number of hospitals, clinics and surgery centers that generate more demand because of their focus on innovation and patient care. With the greying of the population in North America, joint replacement surgeries, cardiac surgeries, and other invasive surgeries with the help of powered surgical instruments are on the rise. As per the U.S. Department of Labour, the forecasted American population aged 65 and over will rise to 82 million by 2050- a 47% boost; similarly, the 65-and-over percent of the overall population is anticipated to increase to 23%. The rising prevalence of diseases such as cancer, diabetes, and cardiovascular disorders has driven significant investments. In September 2023, the White House announced a $240 million investment to fight cancer, the money will go to researchers working on cancer prevention, detection, treatment and survival projects. Thus, chronic diseases necessitate surgery in some cases which drives the demand for powered surgical instruments.

Handpieces dominates the market

The handpieces dominate the powered surgical instrument market due to their central role in the procedures for which powered instruments exist. These are motor-driven devices and find primary applications in dental and surgical procedures. There exist universal devices and those employed for specific applications. Both electric and air-powered handpieces exist, and these instruments find primary application in dentistry. Their characteristics vary depending on dental specialties for which they are intended. Handpieces can be divided based on speed: High-speed generally have speeds between 200.000 and 450.000 revolutions per minute. They are used for removing cavities, preparing crowns, removing old or damaged restorations, preparing contour and retention groves for new restorations, or finishing and polishing restorations. Low-speed can be either electric or air-driven. The maximum speed for electric motors is 50,000 rpm and for air motors, it is 20,000 rpm. They are used for removing decayed soft tissue, preparing cavities, and polishing and finishing restorations.

Electric-powered dominates the market

Electric-powered segment dominates among the other powered surgical instrument markets due to their high degree of precision, portability, and wide adoption in surgical settings. The electric-powered surgical instruments are characterized by a high degree of accuracy and versatility. These are known to be precision instruments with fine control, which is imperative in sensitive surgeries such as orthopedic, neurosurgery, dental surgery, and ENT. They provide very consistent power output, thereby enabling surgeons to conduct very intricate operations with a great deal of accuracy. They are offered with variable speeds that are necessary for different types of procedures. For example, in orthopaedic surgeries, the possibility of adjusting the speed and hence the power of the handpiece will ensure safety and effectiveness for the bone-cutting or drilling procedure. Besides, they are battery-operated handpieces that guarantee very good portability. Because of this, these instruments are deployable by surgeons without the constraints of hoses or air compressors, making them easier to handle in complicated surgical environments.

Aging population and chronic diseases Drives the market

The aging population worldwide has resulted in an increase in chronic diseases, thus creating huge demand for the powered surgical instrument market. As populations in the rest of the world are aging, there is a significant need for surgical treatments against various age-related health problems. Due to age factors, older adults easily become prone to chronic conditions such as cardiovascular diseases, arthritis, cancer, and neurodegenerative disorders, where surgery is necessary. According to Continental United States information from the National Center for Health Statistics, diseases of the heart are the leading causes of death for deaths arising within the US-that is, within one year-amounting to 702,880 deaths. The second leading category is neoplasms or cancer, accounting for 608,371 deaths. This information is available through May 2024. In addition, chronic diseases are common among the younger generation as well, which has increased them in surgical operations such as orthopaedic, cardiac, and neurological surgeries. In a nutshell, the growing elderly population and increased burden of chronic diseases are now creating a good opportunity for innovation and growth to take place in the powered surgical instruments market.

High upfront cost of devices to Hamper the Market

High equipment costs are one of the main reasons affecting the growth of the powered surgical instruments market. This factor severely limits its adoption in cost-sensitive healthcare systems or developing regions. The cost of powered surgical instruments, especially advanced robotic systems, can initially be high, and their maintenance and calibration usually require professional services, further increasing the overall cost of ownership with regular servicing, software updates, and replacement parts. This does not make it easy to justify in smaller health facilities. What's more, powered surgical instruments may call for substantial infrastructural development in terms of area facilitation, special operation theaters, and high-efficiency ventilation and IT support, which add a lot of extra cost to healthcare. Overcoming these will surely involve new financing concepts, readily affordable solutions, and enhanced reimbursement schemes for procedures involving such technologies.

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Powered Surgical Instrument Market. The top 10 companies in this industry are listed below:

- Medtronic

- Intuitive Surgical

- Johnson & Johnson

- Stryker Corporation

- Zimmer Biomet

- Olympus Corporation

- Conmed Corporation

- Terumo Corporation

- Accuray Incorporated

- Smith & Nephew

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

3.9% |

|

Market Size in 2030 |

$3.5 billion |

|

Segments Covered |

By Product Type, By Power Source, By Application, By End User and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

Related Reports

LIST OF TABLES

1.Global POWERED SURGICAL INSTRUMENT MARKET, BY PRODUCT Market 2023-2030 ($M)

1.1 Handpieces Market 2023-2030 ($M) - Global Industry Research

1.1.1 Drill Systems Market 2023-2030 ($M)

1.1.2 Reamers Systems Market 2023-2030 ($M)

1.1.3 Saws Systems Market 2023-2030 ($M)

1.1.4 Stapler Market 2023-2030 ($M)

1.1.5 Shavers Market 2023-2030 ($M)

1.2 Power Source Controls Market 2023-2030 ($M) - Global Industry Research

1.2.1 Batteries Market 2023-2030 ($M)

1.2.2 Electric Consoles Market 2023-2030 ($M)

1.2.3 Pneumatic Regulators Market 2023-2030 ($M)

1.3 Accessories Market 2023-2030 ($M) - Global Industry Research

1.3.1 Surgical Accessories Market 2023-2030 ($M)

1.3.2 Electrical Accessories Market 2023-2030 ($M)

2.Global POWERED SURGICAL INSTRUMENT MARKET, BY POWER SOURCE Market 2023-2030 ($M)

2.1 Battery-powered instruments Market 2023-2030 ($M) - Global Industry Research

2.2 Pneumatic instruments Market 2023-2030 ($M) - Global Industry Research

2.3 Electric instruments Market 2023-2030 ($M) - Global Industry Research

3.Global POWERED SURGICAL INSTRUMENT MARKET, BY PRODUCT Market 2023-2030 (Volume/Units)

3.1 Handpieces Market 2023-2030 (Volume/Units) - Global Industry Research

3.1.1 Drill Systems Market 2023-2030 (Volume/Units)

3.1.2 Reamers Systems Market 2023-2030 (Volume/Units)

3.1.3 Saws Systems Market 2023-2030 (Volume/Units)

3.1.4 Stapler Market 2023-2030 (Volume/Units)

3.1.5 Shavers Market 2023-2030 (Volume/Units)

3.2 Power Source Controls Market 2023-2030 (Volume/Units) - Global Industry Research

3.2.1 Batteries Market 2023-2030 (Volume/Units)

3.2.2 Electric Consoles Market 2023-2030 (Volume/Units)

3.2.3 Pneumatic Regulators Market 2023-2030 (Volume/Units)

3.3 Accessories Market 2023-2030 (Volume/Units) - Global Industry Research

3.3.1 Surgical Accessories Market 2023-2030 (Volume/Units)

3.3.2 Electrical Accessories Market 2023-2030 (Volume/Units)

4.Global POWERED SURGICAL INSTRUMENT MARKET, BY POWER SOURCE Market 2023-2030 (Volume/Units)

4.1 Battery-powered instruments Market 2023-2030 (Volume/Units) - Global Industry Research

4.2 Pneumatic instruments Market 2023-2030 (Volume/Units) - Global Industry Research

4.3 Electric instruments Market 2023-2030 (Volume/Units) - Global Industry Research

5.North America POWERED SURGICAL INSTRUMENT MARKET, BY PRODUCT Market 2023-2030 ($M)

5.1 Handpieces Market 2023-2030 ($M) - Regional Industry Research

5.1.1 Drill Systems Market 2023-2030 ($M)

5.1.2 Reamers Systems Market 2023-2030 ($M)

5.1.3 Saws Systems Market 2023-2030 ($M)

5.1.4 Stapler Market 2023-2030 ($M)

5.1.5 Shavers Market 2023-2030 ($M)

5.2 Power Source Controls Market 2023-2030 ($M) - Regional Industry Research

5.2.1 Batteries Market 2023-2030 ($M)

5.2.2 Electric Consoles Market 2023-2030 ($M)

5.2.3 Pneumatic Regulators Market 2023-2030 ($M)

5.3 Accessories Market 2023-2030 ($M) - Regional Industry Research

5.3.1 Surgical Accessories Market 2023-2030 ($M)

5.3.2 Electrical Accessories Market 2023-2030 ($M)

6.North America POWERED SURGICAL INSTRUMENT MARKET, BY POWER SOURCE Market 2023-2030 ($M)

6.1 Battery-powered instruments Market 2023-2030 ($M) - Regional Industry Research

6.2 Pneumatic instruments Market 2023-2030 ($M) - Regional Industry Research

6.3 Electric instruments Market 2023-2030 ($M) - Regional Industry Research

7.South America POWERED SURGICAL INSTRUMENT MARKET, BY PRODUCT Market 2023-2030 ($M)

7.1 Handpieces Market 2023-2030 ($M) - Regional Industry Research

7.1.1 Drill Systems Market 2023-2030 ($M)

7.1.2 Reamers Systems Market 2023-2030 ($M)

7.1.3 Saws Systems Market 2023-2030 ($M)

7.1.4 Stapler Market 2023-2030 ($M)

7.1.5 Shavers Market 2023-2030 ($M)

7.2 Power Source Controls Market 2023-2030 ($M) - Regional Industry Research

7.2.1 Batteries Market 2023-2030 ($M)

7.2.2 Electric Consoles Market 2023-2030 ($M)

7.2.3 Pneumatic Regulators Market 2023-2030 ($M)

7.3 Accessories Market 2023-2030 ($M) - Regional Industry Research

7.3.1 Surgical Accessories Market 2023-2030 ($M)

7.3.2 Electrical Accessories Market 2023-2030 ($M)

8.South America POWERED SURGICAL INSTRUMENT MARKET, BY POWER SOURCE Market 2023-2030 ($M)

8.1 Battery-powered instruments Market 2023-2030 ($M) - Regional Industry Research

8.2 Pneumatic instruments Market 2023-2030 ($M) - Regional Industry Research

8.3 Electric instruments Market 2023-2030 ($M) - Regional Industry Research

9.Europe POWERED SURGICAL INSTRUMENT MARKET, BY PRODUCT Market 2023-2030 ($M)

9.1 Handpieces Market 2023-2030 ($M) - Regional Industry Research

9.1.1 Drill Systems Market 2023-2030 ($M)

9.1.2 Reamers Systems Market 2023-2030 ($M)

9.1.3 Saws Systems Market 2023-2030 ($M)

9.1.4 Stapler Market 2023-2030 ($M)

9.1.5 Shavers Market 2023-2030 ($M)

9.2 Power Source Controls Market 2023-2030 ($M) - Regional Industry Research

9.2.1 Batteries Market 2023-2030 ($M)

9.2.2 Electric Consoles Market 2023-2030 ($M)

9.2.3 Pneumatic Regulators Market 2023-2030 ($M)

9.3 Accessories Market 2023-2030 ($M) - Regional Industry Research

9.3.1 Surgical Accessories Market 2023-2030 ($M)

9.3.2 Electrical Accessories Market 2023-2030 ($M)

10.Europe POWERED SURGICAL INSTRUMENT MARKET, BY POWER SOURCE Market 2023-2030 ($M)

10.1 Battery-powered instruments Market 2023-2030 ($M) - Regional Industry Research

10.2 Pneumatic instruments Market 2023-2030 ($M) - Regional Industry Research

10.3 Electric instruments Market 2023-2030 ($M) - Regional Industry Research

11.APAC POWERED SURGICAL INSTRUMENT MARKET, BY PRODUCT Market 2023-2030 ($M)

11.1 Handpieces Market 2023-2030 ($M) - Regional Industry Research

11.1.1 Drill Systems Market 2023-2030 ($M)

11.1.2 Reamers Systems Market 2023-2030 ($M)

11.1.3 Saws Systems Market 2023-2030 ($M)

11.1.4 Stapler Market 2023-2030 ($M)

11.1.5 Shavers Market 2023-2030 ($M)

11.2 Power Source Controls Market 2023-2030 ($M) - Regional Industry Research

11.2.1 Batteries Market 2023-2030 ($M)

11.2.2 Electric Consoles Market 2023-2030 ($M)

11.2.3 Pneumatic Regulators Market 2023-2030 ($M)

11.3 Accessories Market 2023-2030 ($M) - Regional Industry Research

11.3.1 Surgical Accessories Market 2023-2030 ($M)

11.3.2 Electrical Accessories Market 2023-2030 ($M)

12.APAC POWERED SURGICAL INSTRUMENT MARKET, BY POWER SOURCE Market 2023-2030 ($M)

12.1 Battery-powered instruments Market 2023-2030 ($M) - Regional Industry Research

12.2 Pneumatic instruments Market 2023-2030 ($M) - Regional Industry Research

12.3 Electric instruments Market 2023-2030 ($M) - Regional Industry Research

13.MENA POWERED SURGICAL INSTRUMENT MARKET, BY PRODUCT Market 2023-2030 ($M)

13.1 Handpieces Market 2023-2030 ($M) - Regional Industry Research

13.1.1 Drill Systems Market 2023-2030 ($M)

13.1.2 Reamers Systems Market 2023-2030 ($M)

13.1.3 Saws Systems Market 2023-2030 ($M)

13.1.4 Stapler Market 2023-2030 ($M)

13.1.5 Shavers Market 2023-2030 ($M)

13.2 Power Source Controls Market 2023-2030 ($M) - Regional Industry Research

13.2.1 Batteries Market 2023-2030 ($M)

13.2.2 Electric Consoles Market 2023-2030 ($M)

13.2.3 Pneumatic Regulators Market 2023-2030 ($M)

13.3 Accessories Market 2023-2030 ($M) - Regional Industry Research

13.3.1 Surgical Accessories Market 2023-2030 ($M)

13.3.2 Electrical Accessories Market 2023-2030 ($M)

14.MENA POWERED SURGICAL INSTRUMENT MARKET, BY POWER SOURCE Market 2023-2030 ($M)

14.1 Battery-powered instruments Market 2023-2030 ($M) - Regional Industry Research

14.2 Pneumatic instruments Market 2023-2030 ($M) - Regional Industry Research

14.3 Electric instruments Market 2023-2030 ($M) - Regional Industry Research

LIST OF FIGURES

1.US Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

2.Canada Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

3.Mexico Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

4.Brazil Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

5.Argentina Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

6.Peru Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

7.Colombia Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

8.Chile Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

9.Rest of South America Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

10.UK Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

11.Germany Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

12.France Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

13.Italy Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

14.Spain Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

15.Rest of Europe Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

16.China Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

17.India Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

18.Japan Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

19.South Korea Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

20.South Africa Powered Surgical Instrument Market Revenue, 2023-2030 ($M)

21.North America Powered Surgical Instrument By Application

22.South America Powered Surgical Instrument By Application

23.Europe Powered Surgical Instrument By Application

24.APAC Powered Surgical Instrument By Application

25.MENA Powered Surgical Instrument By Application

26.adeor Medical AG, Sales /Revenue, 2015-2018 ($Mn/$Bn)

27.AlloTech Co., Ltd., Sales /Revenue, 2015-2018 ($Mn/$Bn)

28.B. Braun Melsungen AG, Sales /Revenue, 2015-2018 ($Mn/$Bn)

29.CONMED Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

30.Johnson Johnson, Sales /Revenue, 2015-2018 ($Mn/$Bn)

31.Medtronic Plc., Sales /Revenue, 2015-2018 ($Mn/$Bn)

32.MicroAire Surgical Instruments, LLC., Sales /Revenue, 2015-2018 ($Mn/$Bn)

33.Smith Nephew Plc., Sales /Revenue, 2015-2018 ($Mn/$Bn)

34.Stryker Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

35.Zimmer Biomet Holdings, Inc., Sales /Revenue, 2015-2018 ($Mn/$Bn)

The Powered Surgical Instrument Market is projected to grow at 3.9% CAGR during the forecast period 2024-2030.

The Powered Surgical Instrument Market size is estimated to be $2.7 billion in 2023 and is projected to reach $3.5 billion by 2030.

The leading players in the Powered Surgical Instrument Market are Medtronic, Intuitive Surgical, Johnson & Johnson, Stryker Corporation, Zimmer Biomet, and others.

The aging population\\\\\\\'s increased risk of chronic diseases like cancer, cardiovascular disease, and orthopedic disorders, along with the development of more accurate, smaller instruments with robotic systems and rising healthcare spending on medical technology, are driving the market for powered surgical instruments.

The increasing prevalence of chronic diseases, advancements in minimally invasive surgery, rising healthcare spending, and innovations within the healthcare industry are collectively driving significant growth in the powered surgical instrument market.