Email

Email Print

Print

Smart Harvest Market - By Type, By Site, By Crop Type and By Geography - Global Opportunity Analysis & Industry Forecast, 2024-2030

Smart Harvest Market Overview

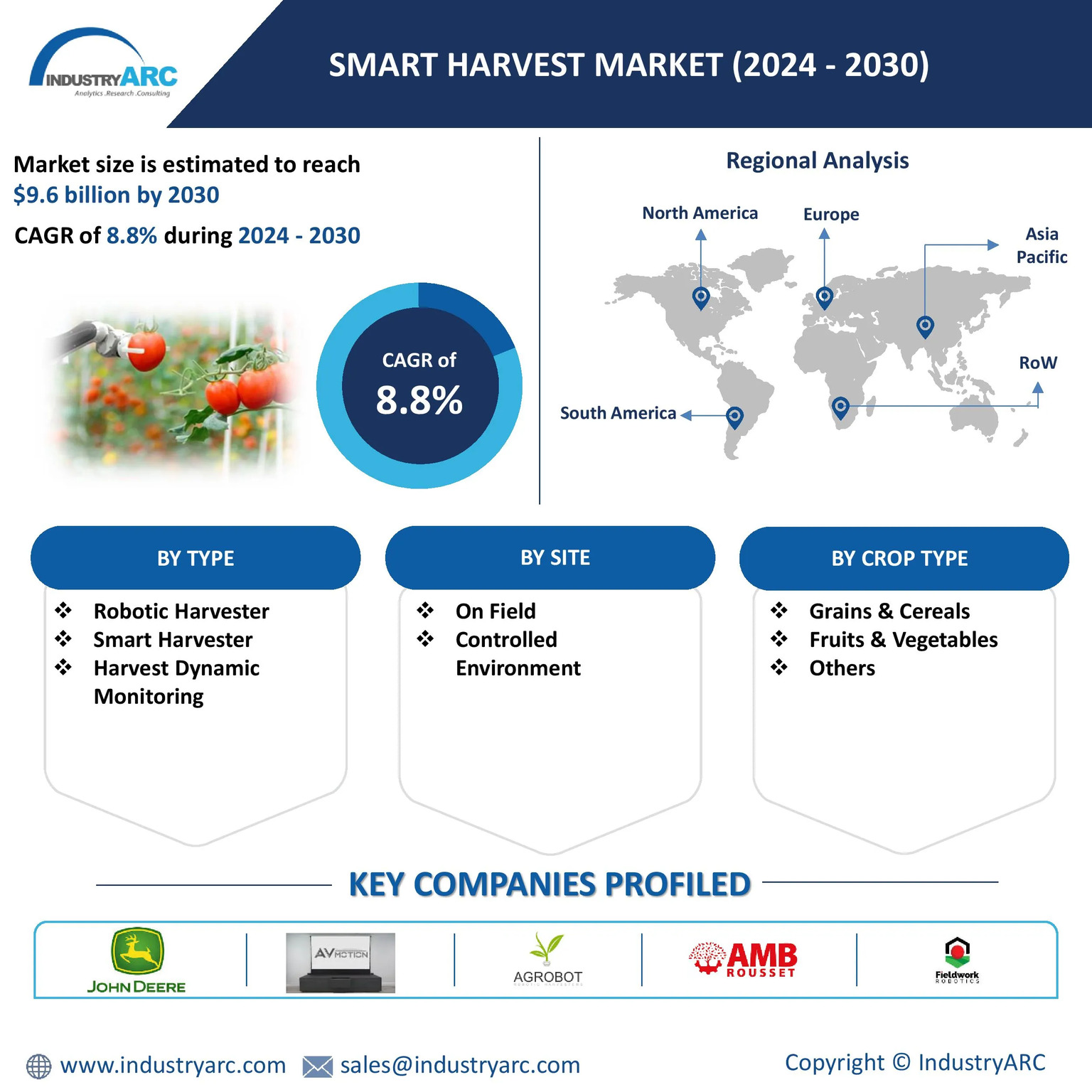

Smart Harvest market size is forecast to reach US$9.6 billion by 2030, after growing at a CAGR of 8.8% during 2024-2030. A major driver is the growing demand for increased agricultural efficiency to meet the rising global food demand. Smart harvesting technologies such as autonomous harvesting robots and drones help farmers optimize crop yields, reduce labor costs and improve harvest timing leading to better quality produce. Additionally, the rising labor shortages in agriculture accelerated the adoption of automated harvesting systems. Government initiatives promoting agricultural mechanization further fuel the market growth.

A major trend in the market is the integration of artificial intelligence (AI) and machine learning (ML). These technologies enable more accurate crop monitoring, allowing robots and drones to identify the optimal time for harvesting and ensuring minimal damage to crops during the process. AI-powered machines also help analyze real-time data, providing actionable insights for farmers. For instance, John Deere introduced innovative AI-powered solutions like Combine Advisor to revolutionize the capabilities of John Deere Combines. Combine Advisor is a comprehensive suite of technologies designed to optimize harvesting operations and maximize yield while minimizing waste and downtime. Another trend is advancements in sensor technology and Internet of Things (IoT) devices are becoming more prevalent in smart harvesting systems. These innovations enable real-time monitoring of environmental factors such as soil moisture, temperature and crop health allowing for precision based decision making and further enhancing overall farm productivity.

Market Snapshot:

Smart Harvest Market - Report Coverage:

The “Smart Harvest Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Smart Harvest Market.

| Attribute | Segment |

|---|---|

|

By Type |

|

|

By Site |

|

|

By Crop Type |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- Due to COVID the agricultural sector was heavily impacted. On account of the closing of restaurants and schools and COVID-19 outbreaks at processing facilities, the agricultural supply chain faced major challenges. The shortage of agricultural labor led to investments in smart harvest that doesn’t require human intervention.

- The Russia-Ukraine conflict impacted the Smart Harvest market. The conflict led to further supply chain issues. Additionally, the war also led to inflation, further straining the market for smart harvest.

Key Takeaways

Grains & Cereals the Largest Segment

Grains and cereals represent the largest segment in the smart harvest market due to their essential role in global food production. Staple crops like wheat, maize and rice are vital to feeding the world’s population making their efficient and timely harvest crucial. The adoption of smart harvesting technologies for grains and cereals is particularly significant in regions with large-scale agriculture where automation can greatly enhance productivity and reduce labor costs. A notable example is Cognitive Agro Pilot, an autonomous AI-based driving system for farming equipment which was designed by Sber and its ecosystem member Cognitive Pilot. With the help of Cognitive Agro Pilot as many as 590,000 metric tonn of grain crops such as wheat, soybeans, barley, oats, sorghum, buckwheat, among others were harvested over 130,000 hectares in Russia. Using smart harvesters, farmers can optimize yield, reduce waste and ensure timely harvesting, which is particularly important for preventing crop losses during critical harvest windows. The growing demand for grains and cereals reinforces this segment’s dominance in the market.

Controlled Environment is the Fastest Growing Segment

Controlled environment agriculture (CEA) that includes greenhouse and indoor farming is the fastest growing segment in the smart harvest market. These systems provide optimal conditions for plant growth by regulating factors such as temperature, humidity and light allowing year-round cultivation. Smart harvesting technologies in these environments like robotic pickers and automated monitoring systems maximize yield and reduce labor needs. The rise of urban agriculture and the demand for fresh and locally grown produce are driving the adoption of CEA methods. As per data from Statistics Canada, greenhouses specializing in fruits and vegetables in Canada have increased in farm gate value for the 11th consecutive year, up 9.2% to $2.5 billion in 2023. Additionally, the ability to control pest and disease outbreaks more effectively than in open fields further boosts their appeal. With increasing investments in vertical and greenhouse farming this segment is expected to continue its rapid growth.

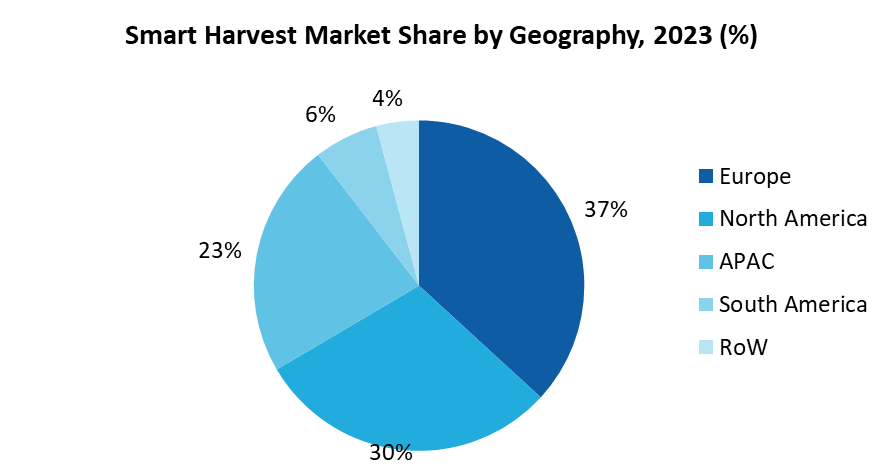

Europe Dominates the Market

Europe dominates the Smart Harvest market with a share of 37% in 2023 owing to its advanced agricultural infrastructure, labor shortages and government support for mechanized farming practices. The region has a strong focus on technological innovation in agriculture with significant investments in precision farming, automation and robotics. European countries also face labor shortages and needs to depend on immigrant workers which further drives the adoption of smart harvest technologies. According to an analysis by Coldiretti, Italy’s organization for agricultural business, migrant workers provide 32% of the total days of labor needed on Italian farms in 2023. According to the report, strawberry picking in Verona, fruit preparation in Friuli, apple harvesting in Trentino and grape harvesting in Piedmont are highly reliant on foreign workers. Owing to stricter immigration and rising labor charges, smart harvest is a better option to ensure that the produce does not go to waste. Additionally, the region’s emphasis on high-value crops such as fruits and vegetables accelerated the implementation of smart harvesting solutions.

Growing Demand for Agricultural Productivity to Drive the Market

According to the UNEP Food Waste Index Report 2024, one-fifth of food produced for human consumption is lost or wasted globally. With a significant portion of global food production lost due to spoilage and inefficient supply chains, there is growing need to prevent this. The need for increased agricultural efficiency is a major driver in the smart harvest market. With global population growth putting pressure on food production systems farmers are seeking ways to optimize yield and minimize waste. Smart harvest technologies such as automated harvesting systems, drones and robotic enable farmers to monitor when the crop is right for harvesting in real time and making data-driven decisions to prevent spoilage either due to damage or over ripeness. By automating the harvesting process these technologies reduce labor costs, minimize human error and allow for more precise harvesting. As a result, farmers can achieve higher productivity and meet the rising global food demand driving the adoption of smart harvest solutions.

Cybersecurity Concerns to Hamper Growth

Cybersecurity concerns pose a significant challenge in the smart harvest market as the increasing integration of IoT devices, drones and autonomous machinery in agriculture exposes farmers to data breaches and cyberattacks. Food and agriculture is the seventh most targeted by ransomware out of 11 critical sectors monitored by the Food and Ag-ISAC and IT-ISAC. 2023 saw more than 2,900 ransomware attacks against those sectors, with 5.5% hitting food and agriculture. The reliance on cloud-based systems for real-time monitoring and decision-making makes smart harvest systems vulnerable to hacking which could lead to disruption in farming operations or unauthorized access to sensitive farm data. Farmers must integrate cybersecurity software into their agricultural equipment. Downtime from operational inefficiencies and cyberattacks could lead to issues and revenue loss.

For more details on this report - Request for Sample

Key Market Players

Global Smart Harvest top 10 companies include:

- John Deere

- AV Motion

- Agrobot

- AMB Rousset

- Fieldwork Robotics

- CNH Industrial

- Octinion

- Dogtooth Technologies Limited

- Green Robot Machinery

- FFRobotics

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

8.8% |

|

Market Size in 2030 |

$9.6 Billion |

|

Segments Covered |

By Type, By Site, By Crop Type and By Geography.

|

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Netherlands, Denmark, Belgium and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Thailand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

For more Agriculture Market reports, please click here

LIST OF TABLES

1.Global Smart Harvest Market, By Site of Operation Market 2023-2030 ($M)

1.1 On-Field Market 2023-2030 ($M) - Global Industry Research

1.1.1 Technological Advancements in Positioning Systems to Drive Growth for On-Field Applications Market 2023-2030 ($M)

1.2 Greenhouses Market 2023-2030 ($M) - Global Industry Research

1.2.1 Smart Greenhouses to Bolster Prospects for Smart Harvest Technologies Market 2023-2030 ($M)

1.3 Indoor Farming Market 2023-2030 ($M) - Global Industry Research

1.3.1 Shrinking Agricultural Land and Technological Innovations in Indoor Farming to Aid Market Growth Market 2023-2030 ($M)

2.Global Smart Harvest Market, By Crop Type Market 2023-2030 ($M)

2.1 Vegetables Market 2023-2030 ($M) - Global Industry Research

2.1.1 Equipment Availability to Drive Growth for Smart Vegetable Harvesting Market 2023-2030 ($M)

2.2 Fruits Market 2023-2030 ($M) - Global Industry Research

2.2.1 Labor Shortages and High Costs of Manual Harvesting to Drive Growth of Smart Harvest of Fruits Market 2023-2030 ($M)

3.Global Smart Harvest Market, By Component Market 2023-2030 ($M)

3.1 Hardware Market 2023-2030 ($M) - Global Industry Research

3.1.1 Advancements in Imaging Systems to Drive Growth for Hardware Components in Smart Harvest Robots Market 2023-2030 ($M)

3.2 Software Market 2023-2030 ($M) - Global Industry Research

3.2.1 Requirement of Optimum Functionality and Efficient Hardware Integration to Drive the Growth of Software Applications in Smart Harvest Systems Market 2023-2030 ($M)

4.Global Smart Harvest Market, By Site of Operation Market 2023-2030 (Volume/Units)

4.1 On-Field Market 2023-2030 (Volume/Units) - Global Industry Research

4.1.1 Technological Advancements in Positioning Systems to Drive Growth for On-Field Applications Market 2023-2030 (Volume/Units)

4.2 Greenhouses Market 2023-2030 (Volume/Units) - Global Industry Research

4.2.1 Smart Greenhouses to Bolster Prospects for Smart Harvest Technologies Market 2023-2030 (Volume/Units)

4.3 Indoor Farming Market 2023-2030 (Volume/Units) - Global Industry Research

4.3.1 Shrinking Agricultural Land and Technological Innovations in Indoor Farming to Aid Market Growth Market 2023-2030 (Volume/Units)

5.Global Smart Harvest Market, By Crop Type Market 2023-2030 (Volume/Units)

5.1 Vegetables Market 2023-2030 (Volume/Units) - Global Industry Research

5.1.1 Equipment Availability to Drive Growth for Smart Vegetable Harvesting Market 2023-2030 (Volume/Units)

5.2 Fruits Market 2023-2030 (Volume/Units) - Global Industry Research

5.2.1 Labor Shortages and High Costs of Manual Harvesting to Drive Growth of Smart Harvest of Fruits Market 2023-2030 (Volume/Units)

6.Global Smart Harvest Market, By Component Market 2023-2030 (Volume/Units)

6.1 Hardware Market 2023-2030 (Volume/Units) - Global Industry Research

6.1.1 Advancements in Imaging Systems to Drive Growth for Hardware Components in Smart Harvest Robots Market 2023-2030 (Volume/Units)

6.2 Software Market 2023-2030 (Volume/Units) - Global Industry Research

6.2.1 Requirement of Optimum Functionality and Efficient Hardware Integration to Drive the Growth of Software Applications in Smart Harvest Systems Market 2023-2030 (Volume/Units)

7.North America Smart Harvest Market, By Site of Operation Market 2023-2030 ($M)

7.1 On-Field Market 2023-2030 ($M) - Regional Industry Research

7.1.1 Technological Advancements in Positioning Systems to Drive Growth for On-Field Applications Market 2023-2030 ($M)

7.2 Greenhouses Market 2023-2030 ($M) - Regional Industry Research

7.2.1 Smart Greenhouses to Bolster Prospects for Smart Harvest Technologies Market 2023-2030 ($M)

7.3 Indoor Farming Market 2023-2030 ($M) - Regional Industry Research

7.3.1 Shrinking Agricultural Land and Technological Innovations in Indoor Farming to Aid Market Growth Market 2023-2030 ($M)

8.North America Smart Harvest Market, By Crop Type Market 2023-2030 ($M)

8.1 Vegetables Market 2023-2030 ($M) - Regional Industry Research

8.1.1 Equipment Availability to Drive Growth for Smart Vegetable Harvesting Market 2023-2030 ($M)

8.2 Fruits Market 2023-2030 ($M) - Regional Industry Research

8.2.1 Labor Shortages and High Costs of Manual Harvesting to Drive Growth of Smart Harvest of Fruits Market 2023-2030 ($M)

9.North America Smart Harvest Market, By Component Market 2023-2030 ($M)

9.1 Hardware Market 2023-2030 ($M) - Regional Industry Research

9.1.1 Advancements in Imaging Systems to Drive Growth for Hardware Components in Smart Harvest Robots Market 2023-2030 ($M)

9.2 Software Market 2023-2030 ($M) - Regional Industry Research

9.2.1 Requirement of Optimum Functionality and Efficient Hardware Integration to Drive the Growth of Software Applications in Smart Harvest Systems Market 2023-2030 ($M)

10.South America Smart Harvest Market, By Site of Operation Market 2023-2030 ($M)

10.1 On-Field Market 2023-2030 ($M) - Regional Industry Research

10.1.1 Technological Advancements in Positioning Systems to Drive Growth for On-Field Applications Market 2023-2030 ($M)

10.2 Greenhouses Market 2023-2030 ($M) - Regional Industry Research

10.2.1 Smart Greenhouses to Bolster Prospects for Smart Harvest Technologies Market 2023-2030 ($M)

10.3 Indoor Farming Market 2023-2030 ($M) - Regional Industry Research

10.3.1 Shrinking Agricultural Land and Technological Innovations in Indoor Farming to Aid Market Growth Market 2023-2030 ($M)

11.South America Smart Harvest Market, By Crop Type Market 2023-2030 ($M)

11.1 Vegetables Market 2023-2030 ($M) - Regional Industry Research

11.1.1 Equipment Availability to Drive Growth for Smart Vegetable Harvesting Market 2023-2030 ($M)

11.2 Fruits Market 2023-2030 ($M) - Regional Industry Research

11.2.1 Labor Shortages and High Costs of Manual Harvesting to Drive Growth of Smart Harvest of Fruits Market 2023-2030 ($M)

12.South America Smart Harvest Market, By Component Market 2023-2030 ($M)

12.1 Hardware Market 2023-2030 ($M) - Regional Industry Research

12.1.1 Advancements in Imaging Systems to Drive Growth for Hardware Components in Smart Harvest Robots Market 2023-2030 ($M)

12.2 Software Market 2023-2030 ($M) - Regional Industry Research

12.2.1 Requirement of Optimum Functionality and Efficient Hardware Integration to Drive the Growth of Software Applications in Smart Harvest Systems Market 2023-2030 ($M)

13.Europe Smart Harvest Market, By Site of Operation Market 2023-2030 ($M)

13.1 On-Field Market 2023-2030 ($M) - Regional Industry Research

13.1.1 Technological Advancements in Positioning Systems to Drive Growth for On-Field Applications Market 2023-2030 ($M)

13.2 Greenhouses Market 2023-2030 ($M) - Regional Industry Research

13.2.1 Smart Greenhouses to Bolster Prospects for Smart Harvest Technologies Market 2023-2030 ($M)

13.3 Indoor Farming Market 2023-2030 ($M) - Regional Industry Research

13.3.1 Shrinking Agricultural Land and Technological Innovations in Indoor Farming to Aid Market Growth Market 2023-2030 ($M)

14.Europe Smart Harvest Market, By Crop Type Market 2023-2030 ($M)

14.1 Vegetables Market 2023-2030 ($M) - Regional Industry Research

14.1.1 Equipment Availability to Drive Growth for Smart Vegetable Harvesting Market 2023-2030 ($M)

14.2 Fruits Market 2023-2030 ($M) - Regional Industry Research

14.2.1 Labor Shortages and High Costs of Manual Harvesting to Drive Growth of Smart Harvest of Fruits Market 2023-2030 ($M)

15.Europe Smart Harvest Market, By Component Market 2023-2030 ($M)

15.1 Hardware Market 2023-2030 ($M) - Regional Industry Research

15.1.1 Advancements in Imaging Systems to Drive Growth for Hardware Components in Smart Harvest Robots Market 2023-2030 ($M)

15.2 Software Market 2023-2030 ($M) - Regional Industry Research

15.2.1 Requirement of Optimum Functionality and Efficient Hardware Integration to Drive the Growth of Software Applications in Smart Harvest Systems Market 2023-2030 ($M)

16.APAC Smart Harvest Market, By Site of Operation Market 2023-2030 ($M)

16.1 On-Field Market 2023-2030 ($M) - Regional Industry Research

16.1.1 Technological Advancements in Positioning Systems to Drive Growth for On-Field Applications Market 2023-2030 ($M)

16.2 Greenhouses Market 2023-2030 ($M) - Regional Industry Research

16.2.1 Smart Greenhouses to Bolster Prospects for Smart Harvest Technologies Market 2023-2030 ($M)

16.3 Indoor Farming Market 2023-2030 ($M) - Regional Industry Research

16.3.1 Shrinking Agricultural Land and Technological Innovations in Indoor Farming to Aid Market Growth Market 2023-2030 ($M)

17.APAC Smart Harvest Market, By Crop Type Market 2023-2030 ($M)

17.1 Vegetables Market 2023-2030 ($M) - Regional Industry Research

17.1.1 Equipment Availability to Drive Growth for Smart Vegetable Harvesting Market 2023-2030 ($M)

17.2 Fruits Market 2023-2030 ($M) - Regional Industry Research

17.2.1 Labor Shortages and High Costs of Manual Harvesting to Drive Growth of Smart Harvest of Fruits Market 2023-2030 ($M)

18.APAC Smart Harvest Market, By Component Market 2023-2030 ($M)

18.1 Hardware Market 2023-2030 ($M) - Regional Industry Research

18.1.1 Advancements in Imaging Systems to Drive Growth for Hardware Components in Smart Harvest Robots Market 2023-2030 ($M)

18.2 Software Market 2023-2030 ($M) - Regional Industry Research

18.2.1 Requirement of Optimum Functionality and Efficient Hardware Integration to Drive the Growth of Software Applications in Smart Harvest Systems Market 2023-2030 ($M)

19.MENA Smart Harvest Market, By Site of Operation Market 2023-2030 ($M)

19.1 On-Field Market 2023-2030 ($M) - Regional Industry Research

19.1.1 Technological Advancements in Positioning Systems to Drive Growth for On-Field Applications Market 2023-2030 ($M)

19.2 Greenhouses Market 2023-2030 ($M) - Regional Industry Research

19.2.1 Smart Greenhouses to Bolster Prospects for Smart Harvest Technologies Market 2023-2030 ($M)

19.3 Indoor Farming Market 2023-2030 ($M) - Regional Industry Research

19.3.1 Shrinking Agricultural Land and Technological Innovations in Indoor Farming to Aid Market Growth Market 2023-2030 ($M)

20.MENA Smart Harvest Market, By Crop Type Market 2023-2030 ($M)

20.1 Vegetables Market 2023-2030 ($M) - Regional Industry Research

20.1.1 Equipment Availability to Drive Growth for Smart Vegetable Harvesting Market 2023-2030 ($M)

20.2 Fruits Market 2023-2030 ($M) - Regional Industry Research

20.2.1 Labor Shortages and High Costs of Manual Harvesting to Drive Growth of Smart Harvest of Fruits Market 2023-2030 ($M)

21.MENA Smart Harvest Market, By Component Market 2023-2030 ($M)

21.1 Hardware Market 2023-2030 ($M) - Regional Industry Research

21.1.1 Advancements in Imaging Systems to Drive Growth for Hardware Components in Smart Harvest Robots Market 2023-2030 ($M)

21.2 Software Market 2023-2030 ($M) - Regional Industry Research

21.2.1 Requirement of Optimum Functionality and Efficient Hardware Integration to Drive the Growth of Software Applications in Smart Harvest Systems Market 2023-2030 ($M)

LIST OF FIGURES

1.US Smart Harvest Market Revenue, 2023-2030 ($M)

2.Canada Smart Harvest Market Revenue, 2023-2030 ($M)

3.Mexico Smart Harvest Market Revenue, 2023-2030 ($M)

4.Brazil Smart Harvest Market Revenue, 2023-2030 ($M)

5.Argentina Smart Harvest Market Revenue, 2023-2030 ($M)

6.Peru Smart Harvest Market Revenue, 2023-2030 ($M)

7.Colombia Smart Harvest Market Revenue, 2023-2030 ($M)

8.Chile Smart Harvest Market Revenue, 2023-2030 ($M)

9.Rest of South America Smart Harvest Market Revenue, 2023-2030 ($M)

10.UK Smart Harvest Market Revenue, 2023-2030 ($M)

11.Germany Smart Harvest Market Revenue, 2023-2030 ($M)

12.France Smart Harvest Market Revenue, 2023-2030 ($M)

13.Italy Smart Harvest Market Revenue, 2023-2030 ($M)

14.Spain Smart Harvest Market Revenue, 2023-2030 ($M)

15.Rest of Europe Smart Harvest Market Revenue, 2023-2030 ($M)

16.China Smart Harvest Market Revenue, 2023-2030 ($M)

17.India Smart Harvest Market Revenue, 2023-2030 ($M)

18.Japan Smart Harvest Market Revenue, 2023-2030 ($M)

19.South Korea Smart Harvest Market Revenue, 2023-2030 ($M)

20.South Africa Smart Harvest Market Revenue, 2023-2030 ($M)

21.North America Smart Harvest By Application

22.South America Smart Harvest By Application

23.Europe Smart Harvest By Application

24.APAC Smart Harvest By Application

25.MENA Smart Harvest By Application

26.Deere & Company, Sales /Revenue, 2015-2018 ($Mn/$Bn)

27.Robert Bosch GmbH, Sales /Revenue, 2015-2018 ($Mn/$Bn)

28.Panasonic Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

29.Energid Technologies Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

30.Smart Harvest Ltd., Sales /Revenue, 2015-2018 ($Mn/$Bn)

31.Harvest Automation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

32.Dogtooth Technologies, Sales /Revenue, 2015-2018 ($Mn/$Bn)

33.AVL Motion B.V., Sales /Revenue, 2015-2018 ($Mn/$Bn)

34.Abundant Robotics, Sales /Revenue, 2015-2018 ($Mn/$Bn)

35.Iron Ox, Sales /Revenue, 2015-2018 ($Mn/$Bn)

36.Ffrobotics, Sales /Revenue, 2015-2018 ($Mn/$Bn)

37.Vision Robotics Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

38.Metomotion, Sales /Revenue, 2015-2018 ($Mn/$Bn)

39.Agrobot, Sales /Revenue, 2015-2018 ($Mn/$Bn)

40.Harvest Croo, Sales /Revenue, 2015-2018 ($Mn/$Bn)

41.Root AI, Sales /Revenue, 2015-2018 ($Mn/$Bn)

42.Key Innovators, Sales /Revenue, 2015-2018 ($Mn/$Bn)

The Smart Harvest Market is projected to grow at 8.8% CAGR during the forecast period 2024-2030.

The Smart Harvest Market size is estimated to be $5.5 billion in 2023 and is projected to reach $9.6 billion by 2030

The leading players in the Smart Harvest Market are John Deere, AV Motion, Agrobot, AMB Rousset, Fieldwork Robotics and others

The integration of artificial intelligence (AI) and machine learning (ML) and the advancements in sensor technologies and IoT devices are some of the major Smart Harvest Market trends in the industry which will create growth opportunities for the market during the forecast period

The growing demand for increased agricultural efficiency, rising labor shortages and government initiatives promoting agricultural mechanization are the driving factors of the market.