Email

Email Print

Print

Smart Weapons Market – By Type , By Platform , By Functionality , By Technology , By Application , By Geography - Opportunity Analysis & Industry Forecast, 2024-2030

Smart Weapons Market Overview:

The Smart Weapons Market size is estimated to reach $85 billion by 2030, growing at a CAGR of 11.0% during the forecast period 2024-2030. The Smart Weapons Market is propelled by technological progressions focusing on improving weapon precision, targeting and dependability. With rising defense expenditure and ongoing military modernization, there is an increased demand for funding allocation towards innovative technologies, driving a stronger push for smart weapons. In response to the escalating requirement for precision strikes to reduce unwanted collateral in ongoing global conflicts, the use of these weapons has been seeing an uptick. A growing risk to worldwide security and the requirements of counter-terrorism undertakings compel the development of unambiguous defense systems that can accomplish rapid and focused action. Also, the market is impacted by improvements in autonomous and UAV systems that commonly employ accurate smart weaponry during missions. The functioning of network-centric warfare and coordinated systems between different military units is facilitated by the indispensable role of smart weapons.

Smart guns with facial recognition and drones for precision strikes are key trends in the security and defense markets, reflecting advances in controlled access and remote engagement. Biofire Tech began accepting orders for its facial recognition-enabled smart gun on April, 2023. This technology limits firearm use to verified users, a significant shift aimed at enhancing firearm security, despite occasional prototype challenges. Meanwhile, drone technology is gaining prominence in military strategies; a recent example occurred on October, 2024, when a drone strike targeted the Russian Special Forces University in Chechnya, emphasizing the strategic precision drones bring to complex conflict zones. Together, these trends demonstrate an increasing reliance on high-tech solutions for improved control, safety, and situational adaptability in modern defense strategies.

Market Snapshot:

Smart Weapons Market - Report Coverage:

The “Smart Weapons Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Smart Weapons Market.

| Attribute | Segment |

|---|---|

|

By Type |

|

|

By Platform |

|

|

By Functionality |

|

|

By Technology |

|

|

By Application |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The smart weapons creation and acquisition were affected due to supply chain delays caused by the COVID-19 pandemic. Considering that countries were focusing on healthcare and economic revival, there were adjustments made to their defense budgets. An increase in remote work and technological flexibility resulted in enhanced innovation, but the issues related to logistics hampered the progress of R&D and deliveries of weapon systems.

- The rising demand for precision weapons in the Ukraine-Russia conflict highlighted the critical importance of innovation and advanced defense systems. Specifically, in countries that are part of NATO, there is a rise in spending on advanced weapons that support Ukraine along with preparation for possible threats. This situation highlighted the importance of smart munitions, drones, and missile systems, fueling quick market growth in spite of still-occurring supply chain difficulties.

Key Takeaways:

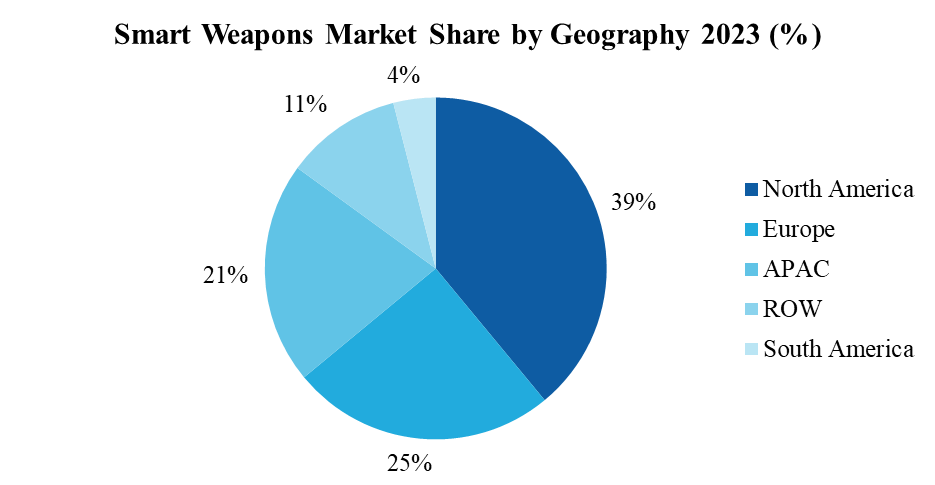

North America Dominates the Market

North America is projected as the leading region in Smart Weapons Market with a market share of 39% in 2023. North America leads the market for smart weapons globally on account of its major military spending and cutting-edge technology. In its role as the foremost champion of technology, the United States is completely focused on developing systems such as guided munitions, advanced missile platforms, as well as a collection of tools and AI. The Stockholm International Peace Research Institute (SIPRI) reports that the share of military spending in North America, accounting for 38.6% of global spending in 2023, is mostly invested in local defense. North America accounts for $943.2 billion of the global defense spending, which totals $2,443.4 billion. The required funding is used to support the ongoing upgrades and modernizations of its military strength. In addition, the presence of important defense contractors, such as Lockheed Martin, RTX, and Northrop Grumman, validates North America’s number one position because these companies are at the forefront of smart defense technology development. The impetus behind the region's dominance is primarily its support for domestic and foreign sources of advanced weaponry.

Military Segment Leads the Market

The Military segment is considered the largest in the Smart Weapons Market when it comes to application, primarily due to substantial government support and domestic purchasing strategies.

Smart Missiles are Leading the Market

The smart weapons market is typically led by the missile segment due to the high demand for precision-strike capabilities. South Korea is advancing its defense by investing $271 million in smart weapons for its F-35 fleet. Approved by the U.S. on December 1, 2023, and pending final congressional authorization, this deal includes a range of advanced munitions. Among these are AIM-120 AMRAAM radar-guided missiles and several GPS- and laser-guided bombs like the GBU-31 JDAM and GBU-54 LJDAM. These upgrades will enhance South Korea’s ability to address regional threats and support seamless interoperability with U.S. forces. The Defense Security Cooperation Agency (DSCA) emphasized that the sale aligns with U.S. foreign policy goals, strengthening South Korea’s defense capabilities and contributing to regional stability.

Technological Advancements to Drive the Market

The latest technological developments that improve weapon accuracy, targeting, and reliability are main motivators in the smart weapons' market. For instance, In September 2024, NATO awarded a $133-million contract to RTX for the supply of laser guidance and GPS kits. This deal seeks to upgrade bombs without guidance systems into controlled munitions through the use of RTX’s Paveway kits. The integration of traditional laser-guided precision with the weather-defiant attributes of GPS ensures that strikes are more reliable across changing conditions. Improved targeting accuracy is made possible through enhanced versions that incorporate inertial navigation systems. Such accuracy decreases the quantity of sorties and the entire weapon inventory, enhancing mission efficiency and raising success rates.

Cybersecurity Risks to Hamper the Market

The smart weapons market faces significant challenges due to cybersecurity risks, as sophisticated weapons systems are increasingly vulnerable to cyberattacks. In July 2024, hackers leaked internal documents from Leidos Holdings Inc., a major IT services provider for the U.S. government, underscoring the risks within defense networks. Additionally, the Pentagon’s Office of the Director, Operational Test and Evaluation (DOT&E) has noted growing threats from radio frequency (RF)-enabled cyberattacks. These RF-based cyber incursions can compromise weapons systems by exploiting wireless channels, posing unique risks to data buses and control systems essential for aircraft, ships and other military vehicles. The increasing frequency and cost of cyberattacks reinforce the urgency for strong cybersecurity measures within the smart weapons sector.

For more details on this report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Smart Weapons Market. The top 10 companies in this industry are listed below:

- Lockheed Martin Corporation

- RTX

- Northrop Grumman Corporation

- BAE Systems plc

- Thales Group

- Saab

- MBDA Systems

- Elbit Systems Ltd.

- Rafael Advanced Defense Systems

- Leonardo S.p.A.

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

11.0% |

|

Market Size in 2030 |

$85 billion |

|

Segments Covered |

By Type, By Platform, By Functionality, By Technology, By Application and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

For more Aerospace and Defense Market reports, please click here

LIST OF TABLES

1.Global MARKET SEGMENTATION Market 2023-2030 ($M)

1.1 Missiles Market 2023-2030 ($M) - Global Industry Research

1.3 Technology Market 2023-2030 ($M) - Global Industry Research

1.3.1 Satellite Guidance Market 2023-2030 ($M)

1.3.2 Radar Guidance Market 2023-2030 ($M)

1.3.3 Infrared Guidance Market 2023-2030 ($M)

1.3.4 Laser Guidance Market 2023-2030 ($M)

1.4 Platform Market 2023-2030 ($M) - Global Industry Research

1.4.1 Land Market 2023-2030 ($M)

1.4.2 Sea Market 2023-2030 ($M)

1.4.3 Air Market 2023-2030 ($M)

2.Global COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

2.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements Market 2023-2030 ($M) - Global Industry Research

3.Global MARKET SEGMENTATION Market 2023-2030 (Volume/Units)

3.1 Missiles Market 2023-2030 (Volume/Units) - Global Industry Research

3.3 Technology Market 2023-2030 (Volume/Units) - Global Industry Research

3.3.1 Satellite Guidance Market 2023-2030 (Volume/Units)

3.3.2 Radar Guidance Market 2023-2030 (Volume/Units)

3.3.3 Infrared Guidance Market 2023-2030 (Volume/Units)

3.3.4 Laser Guidance Market 2023-2030 (Volume/Units)

3.4 Platform Market 2023-2030 (Volume/Units) - Global Industry Research

3.4.1 Land Market 2023-2030 (Volume/Units)

3.4.2 Sea Market 2023-2030 (Volume/Units)

3.4.3 Air Market 2023-2030 (Volume/Units)

4.Global COMPETITIVE LANDSCAPE Market 2023-2030 (Volume/Units)

4.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements Market 2023-2030 (Volume/Units) - Global Industry Research

5.North America MARKET SEGMENTATION Market 2023-2030 ($M)

5.1 Missiles Market 2023-2030 ($M) - Regional Industry Research

5.3 Technology Market 2023-2030 ($M) - Regional Industry Research

5.3.1 Satellite Guidance Market 2023-2030 ($M)

5.3.2 Radar Guidance Market 2023-2030 ($M)

5.3.3 Infrared Guidance Market 2023-2030 ($M)

5.3.4 Laser Guidance Market 2023-2030 ($M)

5.4 Platform Market 2023-2030 ($M) - Regional Industry Research

5.4.1 Land Market 2023-2030 ($M)

5.4.2 Sea Market 2023-2030 ($M)

5.4.3 Air Market 2023-2030 ($M)

6.North America COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements Market 2023-2030 ($M) - Regional Industry Research

7.South America MARKET SEGMENTATION Market 2023-2030 ($M)

7.1 Missiles Market 2023-2030 ($M) - Regional Industry Research

7.3 Technology Market 2023-2030 ($M) - Regional Industry Research

7.3.1 Satellite Guidance Market 2023-2030 ($M)

7.3.2 Radar Guidance Market 2023-2030 ($M)

7.3.3 Infrared Guidance Market 2023-2030 ($M)

7.3.4 Laser Guidance Market 2023-2030 ($M)

7.4 Platform Market 2023-2030 ($M) - Regional Industry Research

7.4.1 Land Market 2023-2030 ($M)

7.4.2 Sea Market 2023-2030 ($M)

7.4.3 Air Market 2023-2030 ($M)

8.South America COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

8.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements Market 2023-2030 ($M) - Regional Industry Research

9.Europe MARKET SEGMENTATION Market 2023-2030 ($M)

9.1 Missiles Market 2023-2030 ($M) - Regional Industry Research

9.3 Technology Market 2023-2030 ($M) - Regional Industry Research

9.3.1 Satellite Guidance Market 2023-2030 ($M)

9.3.2 Radar Guidance Market 2023-2030 ($M)

9.3.3 Infrared Guidance Market 2023-2030 ($M)

9.3.4 Laser Guidance Market 2023-2030 ($M)

9.4 Platform Market 2023-2030 ($M) - Regional Industry Research

9.4.1 Land Market 2023-2030 ($M)

9.4.2 Sea Market 2023-2030 ($M)

9.4.3 Air Market 2023-2030 ($M)

10.Europe COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

10.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements Market 2023-2030 ($M) - Regional Industry Research

11.APAC MARKET SEGMENTATION Market 2023-2030 ($M)

11.1 Missiles Market 2023-2030 ($M) - Regional Industry Research

11.3 Technology Market 2023-2030 ($M) - Regional Industry Research

11.3.1 Satellite Guidance Market 2023-2030 ($M)

11.3.2 Radar Guidance Market 2023-2030 ($M)

11.3.3 Infrared Guidance Market 2023-2030 ($M)

11.3.4 Laser Guidance Market 2023-2030 ($M)

11.4 Platform Market 2023-2030 ($M) - Regional Industry Research

11.4.1 Land Market 2023-2030 ($M)

11.4.2 Sea Market 2023-2030 ($M)

11.4.3 Air Market 2023-2030 ($M)

12.APAC COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

12.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements Market 2023-2030 ($M) - Regional Industry Research

13.MENA MARKET SEGMENTATION Market 2023-2030 ($M)

13.1 Missiles Market 2023-2030 ($M) - Regional Industry Research

13.3 Technology Market 2023-2030 ($M) - Regional Industry Research

13.3.1 Satellite Guidance Market 2023-2030 ($M)

13.3.2 Radar Guidance Market 2023-2030 ($M)

13.3.3 Infrared Guidance Market 2023-2030 ($M)

13.3.4 Laser Guidance Market 2023-2030 ($M)

13.4 Platform Market 2023-2030 ($M) - Regional Industry Research

13.4.1 Land Market 2023-2030 ($M)

13.4.2 Sea Market 2023-2030 ($M)

13.4.3 Air Market 2023-2030 ($M)

14.MENA COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

14.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements Market 2023-2030 ($M) - Regional Industry Research

LIST OF FIGURES

1.US Smart Weapons Market Revenue, 2023-2030 ($M)

2.Canada Smart Weapons Market Revenue, 2023-2030 ($M)

3.Mexico Smart Weapons Market Revenue, 2023-2030 ($M)

4.Brazil Smart Weapons Market Revenue, 2023-2030 ($M)

5.Argentina Smart Weapons Market Revenue, 2023-2030 ($M)

6.Peru Smart Weapons Market Revenue, 2023-2030 ($M)

7.Colombia Smart Weapons Market Revenue, 2023-2030 ($M)

8.Chile Smart Weapons Market Revenue, 2023-2030 ($M)

9.Rest of South America Smart Weapons Market Revenue, 2023-2030 ($M)

10.UK Smart Weapons Market Revenue, 2023-2030 ($M)

11.Germany Smart Weapons Market Revenue, 2023-2030 ($M)

12.France Smart Weapons Market Revenue, 2023-2030 ($M)

13.Italy Smart Weapons Market Revenue, 2023-2030 ($M)

14.Spain Smart Weapons Market Revenue, 2023-2030 ($M)

15.Rest of Europe Smart Weapons Market Revenue, 2023-2030 ($M)

16.China Smart Weapons Market Revenue, 2023-2030 ($M)

17.India Smart Weapons Market Revenue, 2023-2030 ($M)

18.Japan Smart Weapons Market Revenue, 2023-2030 ($M)

19.South Korea Smart Weapons Market Revenue, 2023-2030 ($M)

20.South Africa Smart Weapons Market Revenue, 2023-2030 ($M)

21.North America Smart Weapons By Application

22.South America Smart Weapons By Application

23.Europe Smart Weapons By Application

24.APAC Smart Weapons By Application

25.MENA Smart Weapons By Application

The Smart Weapons Market is projected to grow at 11.0% CAGR during the forecast period 2024-2030.

The Smart Weapons Market size is estimated to be $40.94 billion in 2023 and is projected to reach $85 billion by 2030

The leading players in the Smart Weapons Market are Lockheed Martin Corporation, RTX, Northrop Grumman Corporation, BAE Systems plc, Thales Group and Others.

Smart guns with facial recognition and drones for precision strikes are some of the major Smart Weapons Market trends in the industry which will create growth opportunities for the market during the forecast period.

Advancements in artificial intelligence (AI), increased demand for precision-guided munitions, and growing adoption of autonomous systems are the driving factors of the Smart Weapons market.