Email

Email Print

Print

Space Propulsion System Market - By Propulsion Type , By Component , By Class of Orbit , By Application , By End-User and By Geography Analysis - Global Opportunity Analysis & Industry Forecast, 2024-2030

Space Propulsion System Market Overview:

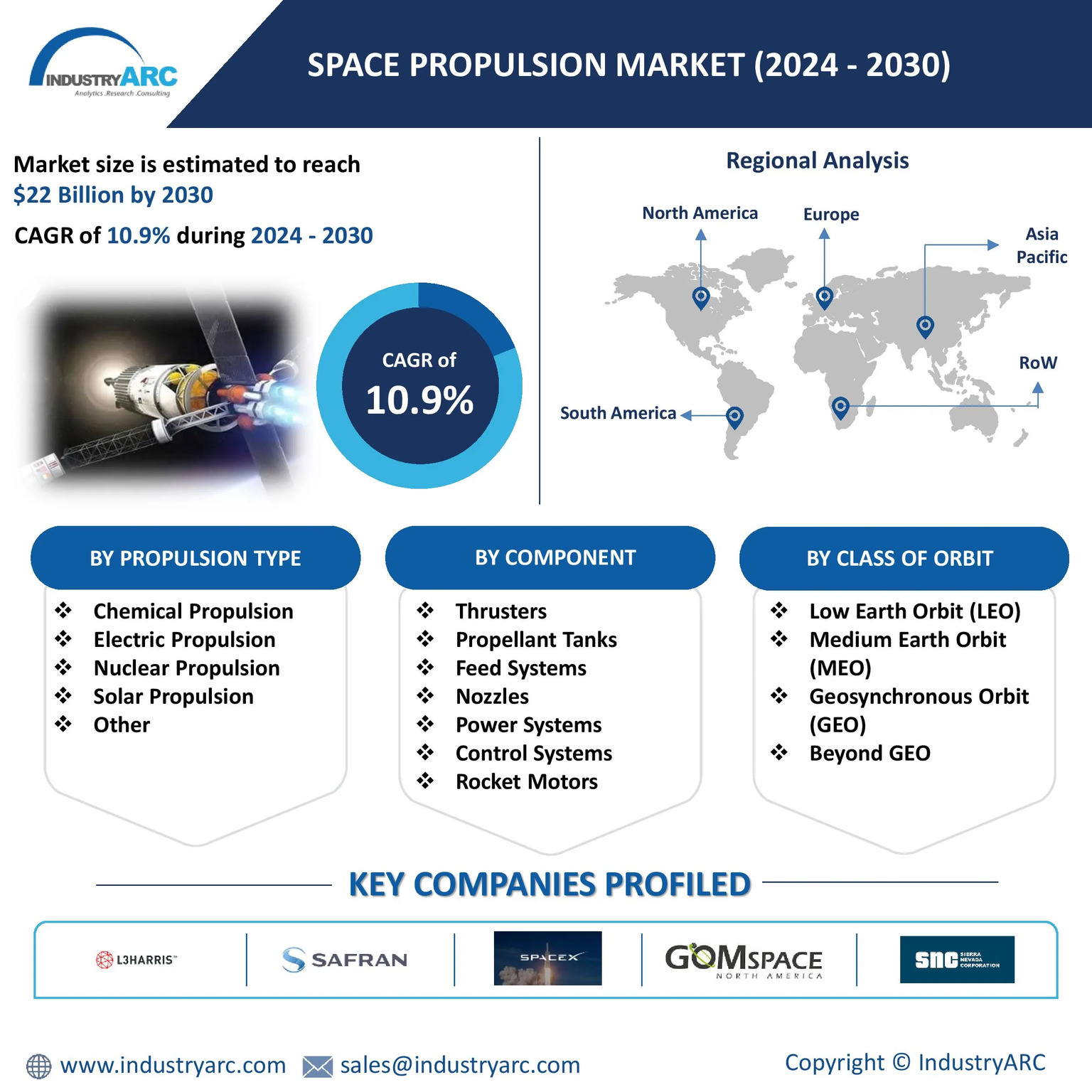

Space Propulsion System Market size is estimated to reach $22 billion by 2030, growing at a CAGR of 10.9% during the forecast period 2024-2030. The space propulsion system market is experiencing significant growth driven by several key factors. Increasing investments in space exploration and commercialization from both governments and private companies are fuelling demand for advanced propulsion systems. The deployment of large satellite constellations for telecommunications and Earth observation requires sophisticated systems for orbit maintenance and manoeuvring. Additionally, the need to address space debris is prompting the development of propulsion systems for satellite deorbiting and debris removal. Technological advancements in electric propulsion and materials have enhanced the performance and efficiency of these systems, further stimulating market growth. Rising government and private sector investments are accelerating the development and adoption of advanced propulsion technologies.

Innovations in electric propulsion, such as ion and Hall effect thrusters by offering exceptional fuel efficiency and precise control for long-duration operations. These systems use electric fields to accelerate ions thus enabling spacecraft to achieve high velocities with minimal fuel consumption. Such advancements are ideal for deep-space exploration, satellite station-keeping and orbital adjustments, where efficiency outweighs the need for high thrust. Simultaneously, the developments in reusable launch vehicles, exemplified by SpaceX’s Falcon 9, are revolutionizing the economics of space access. By recovering and reusing boosters, these systems significantly lower launch costs while increasing launch frequencies. This shift is enabling more frequent missions, expanding access for commercial ventures and fostering sustainable practices in the space industry.

Market Snapshot:

Space Propulsion System Market- Report Coverage:

The “Space Propulsion System Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Space Propulsion System Market.

| Attribute | Segment |

|---|---|

|

By Propulsion Type |

|

|

By Component |

|

|

By Class of Orbit |

|

|

By Application |

|

|

By End User |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- During COVID- 19 pandemic, factory shutdowns due to lockdowns led to delays in the production and testing of critical components for space propulsion systems. Additionally, many space agencies and private companies faced difficulties in securing the necessary materials and labor for propulsion technology development, which slowed down mission timelines and increased costs.

- The ongoing Russia-Ukraine conflict has further influenced the space propulsion market, particularly in the context of European space programs. The war has led to a re- evaluation of Europe's dependence on Russian-made rocket engines, which have traditionally been used for launching both commercial and governmental satellites. With sanctions placed on Russia and the disruption of partnerships with entities such as the Russian space agency Roscosmos, European companies have been forced to expedite the development of alternative propulsion solutions.

Key Takeaways:

-

North America Dominates the Market

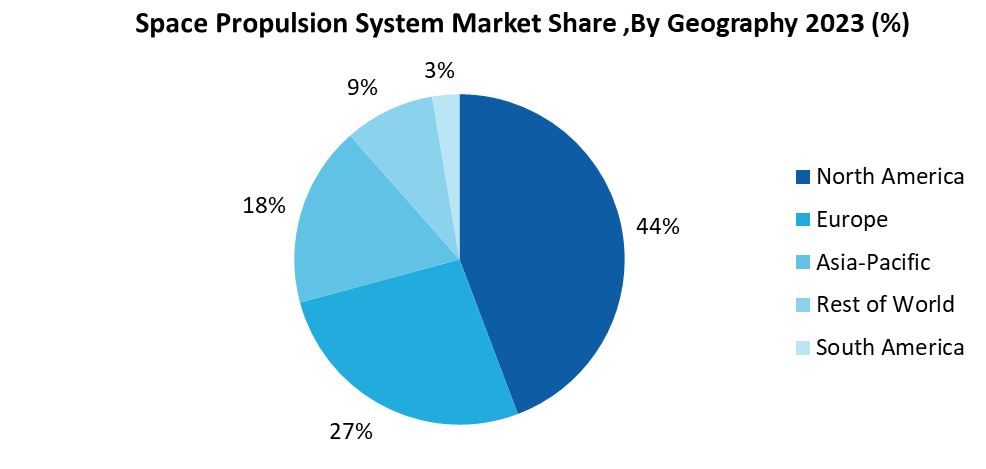

North America is the dominant region in the space propulsion system market largely due to the presence of major industry players and substantial investments. The United States, in particular, leads with companies such as SpaceX, Blue Origin, and United Launch Alliance (ULA) which drive innovation in space propulsion technologies. SpaceX’s advancements, including the Falcon 9 and Falcon Heavy rockets, highlight the region’s technological leadership. Government investments from NASA including projects like the Space Launch System (SLS) and Artemis missions, further bolster North America’s position. Significant investments from both government entities, such as NASA’s Space Launch System (SLS) and Artemis program, and private sector players further fuel this growth. The region’s high frequency of launches and a thriving private sector contribute to its dominance. Additionally, North America's extensive launch infrastructure and high frequency of space missions support ongoing demand for advanced propulsion technologies. The supportive regulatory environment and strategic focus on expanding space exploration and commercialization also contribute to the region's competitive edge. As the space economy continues to grow, encompassing satellite communications, Earth observation, and space tourism, North America’s robust framework positions it to retain its leading role in the global space propulsion market.

-

Chemical Propulsion is the Largest Segment

In the space propulsion system market, chemical propulsion remains the dominant type due to its high thrust capabilities and established reliability. Chemical propulsion systems, including liquid and solid rocket engines, are essential for launch vehicles and provide the powerful thrust needed to escape Earth's atmosphere. Their high thrust-to-weight ratios and proven performance make them indispensable for various space missions, from satellite launches to crewed spaceflights. The technology behind chemical propulsion is well-developed and has a long track record, contributing to its continued dominance in the market. SpaceX’s Falcon 9 and Falcon Heavy rockets, which are dominant players in the launch vehicle market, use chemical propulsion systems. The Falcon 9, for example, employs Merlin engines powered by RP-1 (a refined form of kerosene) and liquid oxygen (LOX). This chemical propulsion setup is central to the rocket’s ability to deliver payloads to low Earth orbit (LEO) and beyond. Also, NASA’s Space Launch System (SLS) which was designed for deep space missions including crewed missions to the Moon and Mars, relies on chemical propulsion. The SLS employs RS-25 engines and solid rocket boosters, both of which use chemical propellants. This highlights the continued reliance on chemical propulsion for high-performance, heavy-lift missions.

-

Launch Vehicles are the Largest Segment

In the space propulsion system market, launch vehicles dominate due to their fundamental role in deploying satellites and other payloads into space. These rockets, which use chemical propulsion systems, are essential for overcoming Earth's gravity and reaching various orbits. The market for launch vehicles is driven by the increasing frequency of satellite launches, fueled by the rise of satellite constellations and commercial space missions. Technological advancements have further solidified the dominance of launch vehicles. Innovations such as reusable rocket stages have significantly reduced the cost of space access. SpaceX’s Falcon 9 features a reusable first stage that has been successfully landed and reused multiple times, contributing to a decrease in launch costs and an increase in launch frequency. Similarly, NASA’s Space Launch System (SLS), designed for deep-space missions, represents a significant investment in heavy-lift capabilities, essential for missions to the Moon and Mars. Moreover, the expansion of satellite constellations, such as SpaceX’s Starlink and OneWeb, which aim to provide global internet coverage, underscores the growing need for frequent and reliable launches. The deployment of these constellations requires a steady stream of launches, further cementing the dominance of launch vehicles in the space propulsion market.

-

Expansion of Satellite Constellations Boosts the Market

The deployment of large satellite constellations, exemplified by initiatives such as SpaceX's Starlink and Amazon's Project Kuiper, is a major driver of market growth. As of mid-2024, SpaceX has launched over 4,500 Starlink satellites with plans to deploy up to 12,000 satellites in its first phase and potentially up to 42,000 in total. This sheer number of satellites requires continuous advancements and reliable propulsion systems for deployment, maintenance and end-of-life management. In February 2023, Amazon has received FCC approval to deploy up to 3,236 satellites for its Project Kuiper constellation, aimed at providing global broadband coverage and to support the deployment and operation of such extensive satellite networks. These constellations aim to provide global high-speed internet coverage and other services, necessitating advanced propulsion systems for a range of functions. These include the initial deployment of satellites into their designated orbits, ongoing orbit maintenance, adjustments, and end-of-life deorbiting to manage space debris and maintain orbital slots. The Space Foundation’s 2024 Space Report notes that commercial satellite constellations are expected to drive significant investments in space infrastructure, including propulsion systems. The report highlights that companies investing in these constellations will need robust propulsion solutions to ensure the successful deployment and operation of their satellite networks. The scale and complexity of these constellations drive continuous demand for sophisticated propulsion technologies, as they require precise and reliable systems to ensure effective operation and longevity of the satellite networks.

-

High Cost of Development and Implementation to Hamper the Market

Developing advanced propulsion technologies, such as those required for deep-space missions or complex satellite constellations, involves substantial financial investment. This includes the costs of research and development, testing, and manufacturing of high-performance propulsion systems. For instance, technologies like nuclear propulsion and advanced electric thrusters require significant investment to ensure they meet safety and performance standards. Additionally, the intricate nature of these technologies means that achieving economies of scale is challenging. The high costs can be a barrier for new entrants and can limit the ability of companies to innovate and adopt cutting-edge propulsion systems. This financial strain is compounded by the need for rigorous testing and certification processes, which further increase costs. For example, NASA’s Space Launch System (SLS) and SpaceX's Raptor engines, despite their advanced capabilities, have required billions of dollars in investment to develop and test. The substantial costs associated with these projects highlight the broader challenge facing the space propulsion market: balancing innovation and cost-effectiveness to drive growth while managing financial constraints.

For More Details on This Report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Space Propulsion System Market. The top 10 companies in this industry are listed below:

- L3Harris Technologies Inc.

- SpaceX

- Safran SA

- Thales Group

- Sierra Nevada Corporation

- IHI Corporation

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Ariane Group

- Honeywell Aerospace

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

10.9% |

|

Market Size in 2030 |

$22 Billion |

|

Segments Covered |

By Propulsion Type, By Component, By Class of Orbit By Application, By End-User and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, , Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

For more Aerospace and Defense Market reports, please click here

LIST OF TABLES

1.Global Space Propulsion System Market By Type) Market 2023-2030 ($M)

1.1 Satellite Market 2023-2030 ($M) - Global Industry Research

1.1.1 Chemical Propulsion System Market 2023-2030 ($M)

1.1.2 Electric Propulsion System Market 2023-2030 ($M)

1.1.3 Hybrid Propulsion System Market 2023-2030 ($M)

1.2 Launch Vehicle Market 2023-2030 ($M) - Global Industry Research

1.2.1 Solid Propulsion System Market 2023-2030 ($M)

1.2.2 Liquid Propulsion System Market 2023-2030 ($M)

1.2.3 Hybrid Propulsion System Market 2023-2030 ($M)

2.Global Space Propulsion System Market By End User) Market 2023-2030 ($M)

2.1 Commercial Market 2023-2030 ($M) - Global Industry Research

2.2 Government Military Market 2023-2030 ($M) - Global Industry Research

3.Global Space Propulsion System Market By Type) Market 2023-2030 (Volume/Units)

3.1 Satellite Market 2023-2030 (Volume/Units) - Global Industry Research

3.1.1 Chemical Propulsion System Market 2023-2030 (Volume/Units)

3.1.2 Electric Propulsion System Market 2023-2030 (Volume/Units)

3.1.3 Hybrid Propulsion System Market 2023-2030 (Volume/Units)

3.2 Launch Vehicle Market 2023-2030 (Volume/Units) - Global Industry Research

3.2.1 Solid Propulsion System Market 2023-2030 (Volume/Units)

3.2.2 Liquid Propulsion System Market 2023-2030 (Volume/Units)

3.2.3 Hybrid Propulsion System Market 2023-2030 (Volume/Units)

4.Global Space Propulsion System Market By End User) Market 2023-2030 (Volume/Units)

4.1 Commercial Market 2023-2030 (Volume/Units) - Global Industry Research

4.2 Government Military Market 2023-2030 (Volume/Units) - Global Industry Research

5.North America Space Propulsion System Market By Type) Market 2023-2030 ($M)

5.1 Satellite Market 2023-2030 ($M) - Regional Industry Research

5.1.1 Chemical Propulsion System Market 2023-2030 ($M)

5.1.2 Electric Propulsion System Market 2023-2030 ($M)

5.1.3 Hybrid Propulsion System Market 2023-2030 ($M)

5.2 Launch Vehicle Market 2023-2030 ($M) - Regional Industry Research

5.2.1 Solid Propulsion System Market 2023-2030 ($M)

5.2.2 Liquid Propulsion System Market 2023-2030 ($M)

5.2.3 Hybrid Propulsion System Market 2023-2030 ($M)

6.North America Space Propulsion System Market By End User) Market 2023-2030 ($M)

6.1 Commercial Market 2023-2030 ($M) - Regional Industry Research

6.2 Government Military Market 2023-2030 ($M) - Regional Industry Research

7.South America Space Propulsion System Market By Type) Market 2023-2030 ($M)

7.1 Satellite Market 2023-2030 ($M) - Regional Industry Research

7.1.1 Chemical Propulsion System Market 2023-2030 ($M)

7.1.2 Electric Propulsion System Market 2023-2030 ($M)

7.1.3 Hybrid Propulsion System Market 2023-2030 ($M)

7.2 Launch Vehicle Market 2023-2030 ($M) - Regional Industry Research

7.2.1 Solid Propulsion System Market 2023-2030 ($M)

7.2.2 Liquid Propulsion System Market 2023-2030 ($M)

7.2.3 Hybrid Propulsion System Market 2023-2030 ($M)

8.South America Space Propulsion System Market By End User) Market 2023-2030 ($M)

8.1 Commercial Market 2023-2030 ($M) - Regional Industry Research

8.2 Government Military Market 2023-2030 ($M) - Regional Industry Research

9.Europe Space Propulsion System Market By Type) Market 2023-2030 ($M)

9.1 Satellite Market 2023-2030 ($M) - Regional Industry Research

9.1.1 Chemical Propulsion System Market 2023-2030 ($M)

9.1.2 Electric Propulsion System Market 2023-2030 ($M)

9.1.3 Hybrid Propulsion System Market 2023-2030 ($M)

9.2 Launch Vehicle Market 2023-2030 ($M) - Regional Industry Research

9.2.1 Solid Propulsion System Market 2023-2030 ($M)

9.2.2 Liquid Propulsion System Market 2023-2030 ($M)

9.2.3 Hybrid Propulsion System Market 2023-2030 ($M)

10.Europe Space Propulsion System Market By End User) Market 2023-2030 ($M)

10.1 Commercial Market 2023-2030 ($M) - Regional Industry Research

10.2 Government Military Market 2023-2030 ($M) - Regional Industry Research

11.APAC Space Propulsion System Market By Type) Market 2023-2030 ($M)

11.1 Satellite Market 2023-2030 ($M) - Regional Industry Research

11.1.1 Chemical Propulsion System Market 2023-2030 ($M)

11.1.2 Electric Propulsion System Market 2023-2030 ($M)

11.1.3 Hybrid Propulsion System Market 2023-2030 ($M)

11.2 Launch Vehicle Market 2023-2030 ($M) - Regional Industry Research

11.2.1 Solid Propulsion System Market 2023-2030 ($M)

11.2.2 Liquid Propulsion System Market 2023-2030 ($M)

11.2.3 Hybrid Propulsion System Market 2023-2030 ($M)

12.APAC Space Propulsion System Market By End User) Market 2023-2030 ($M)

12.1 Commercial Market 2023-2030 ($M) - Regional Industry Research

12.2 Government Military Market 2023-2030 ($M) - Regional Industry Research

13.MENA Space Propulsion System Market By Type) Market 2023-2030 ($M)

13.1 Satellite Market 2023-2030 ($M) - Regional Industry Research

13.1.1 Chemical Propulsion System Market 2023-2030 ($M)

13.1.2 Electric Propulsion System Market 2023-2030 ($M)

13.1.3 Hybrid Propulsion System Market 2023-2030 ($M)

13.2 Launch Vehicle Market 2023-2030 ($M) - Regional Industry Research

13.2.1 Solid Propulsion System Market 2023-2030 ($M)

13.2.2 Liquid Propulsion System Market 2023-2030 ($M)

13.2.3 Hybrid Propulsion System Market 2023-2030 ($M)

14.MENA Space Propulsion System Market By End User) Market 2023-2030 ($M)

14.1 Commercial Market 2023-2030 ($M) - Regional Industry Research

14.2 Government Military Market 2023-2030 ($M) - Regional Industry Research

LIST OF FIGURES

1.US Global Space Propulsion System Market Revenue, 2023-2030 ($M)

2.Canada Global Space Propulsion System Market Revenue, 2023-2030 ($M)

3.Mexico Global Space Propulsion System Market Revenue, 2023-2030 ($M)

4.Brazil Global Space Propulsion System Market Revenue, 2023-2030 ($M)

5.Argentina Global Space Propulsion System Market Revenue, 2023-2030 ($M)

6.Peru Global Space Propulsion System Market Revenue, 2023-2030 ($M)

7.Colombia Global Space Propulsion System Market Revenue, 2023-2030 ($M)

8.Chile Global Space Propulsion System Market Revenue, 2023-2030 ($M)

9.Rest of South America Global Space Propulsion System Market Revenue, 2023-2030 ($M)

10.UK Global Space Propulsion System Market Revenue, 2023-2030 ($M)

11.Germany Global Space Propulsion System Market Revenue, 2023-2030 ($M)

12.France Global Space Propulsion System Market Revenue, 2023-2030 ($M)

13.Italy Global Space Propulsion System Market Revenue, 2023-2030 ($M)

14.Spain Global Space Propulsion System Market Revenue, 2023-2030 ($M)

15.Rest of Europe Global Space Propulsion System Market Revenue, 2023-2030 ($M)

16.China Global Space Propulsion System Market Revenue, 2023-2030 ($M)

17.India Global Space Propulsion System Market Revenue, 2023-2030 ($M)

18.Japan Global Space Propulsion System Market Revenue, 2023-2030 ($M)

19.South Korea Global Space Propulsion System Market Revenue, 2023-2030 ($M)

20.South Africa Global Space Propulsion System Market Revenue, 2023-2030 ($M)

21.North America Global Space Propulsion System By Application

22.South America Global Space Propulsion System By Application

23.Europe Global Space Propulsion System By Application

24.APAC Global Space Propulsion System By Application

25.MENA Global Space Propulsion System By Application

26.Northrop Grumman Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

27.Aerojet Rocketdyne, Sales /Revenue, 2015-2018 ($Mn/$Bn)

28.Airbus S.A.S, Sales /Revenue, 2015-2018 ($Mn/$Bn)

29.Ariane Group GmbH, Sales /Revenue, 2015-2018 ($Mn/$Bn)

30.Blue Origin, Sales /Revenue, 2015-2018 ($Mn/$Bn)

31.IHI Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

32.Lockheed Martin Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

33.Mitsubishi Heavy Industries Ltd., Sales /Revenue, 2015-2018 ($Mn/$Bn)

34.Moog Inc., Sales /Revenue, 2015-2018 ($Mn/$Bn)

35.OHB System AG, Sales /Revenue, 2015-2018 ($Mn/$Bn)

36.Phase Four, Sales /Revenue, 2015-2018 ($Mn/$Bn)

37.Safran, Sales /Revenue, 2015-2018 ($Mn/$Bn)

38.Space Exploration Technologies Corp., Sales /Revenue, 2015-2018 ($Mn/$Bn)

39.Thales Group, Sales /Revenue, 2015-2018 ($Mn/$Bn)

The Space Propulsion System Market is projected to grow at 10.9% CAGR during the forecast period 2024-2030.

The Space Propulsion System Market size is estimated to be $X million in 2023 and is projected to reach $22 Billion by 2030.

The leading players in the Space Propulsion System Market are L3Harris Technologies Inc., SpaceX, Safran SA, Thales Group, Sierra Nevada Corporation and Others.

Innovations in electric propulsion , commercialization of space, including the burgeoning space tourism industry and emerging interests in space mining are some of the market trends in the industry which will create growth opportunities for the market during the forecast period.

Key driving factors include increasing investments in space exploration, commercialization from both governments and private companies and the deployment of large satellite constellations.