Email

Email Print

Print

Automotive Data Monetization Market – By Provider Type , By Solution , By Type , By License Model , By Deployment , By Application , By End User , By Geography – Global Opportunity Analysis & Industry Forecast, 2024-2030

Automotive Data Monetization Market Overview:

Automotive Data Monetization Market Size is valued at $19.148 Billion by 2030, and is anticipated to grow at a CAGR of 62.9% during the forecast period 2024 -2030. This growth is primarily driven by advancements in AI, machine learning, and data analytics, enabling automotive companies to extract valuable insights from extensive datasets. As vehicles become increasingly interconnected, the demand for data-driven products and services rises, presenting opportunities for new revenue streams and operational efficiencies within the automotive sector.

The automotive industry is undergoing a transformative shift as data monetization becomes a strategic focus. Connected vehicles generate vast amounts of data, which can be leveraged for predictive maintenance, usage-based insurance, and targeted advertising. However, challenges such as cybersecurity concerns and high implementation costs persist. To capitalize on this opportunity, automotive manufacturers must enhance their digital capabilities and adopt innovative business models, transitioning from traditional hardware sales to software-as-a-service offerings. By doing so, they can unlock new profit pools and ensure long-term sustainability in an increasingly data-driven market.

Market Snapshot:

Automotive Data Monetization Market - Report Coverage:

The “Automotive Data Monetization Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Automotive Data Monetization Market.

| Attribute | Segment |

|---|---|

|

By Provider Type |

|

|

By Solution |

|

|

By Type |

|

|

By License Model |

|

|

By Deployment |

|

|

By Application |

|

|

By End User |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic significantly disrupted the automotive data monetization market. The global supply chain faced severe challenges, including factory shutdowns and reduced workforce availability, leading to delays in the development and deployment of connected vehicle technologies. This situation hindered automotive manufacturers' ability to launch data-driven services. For instance, in 2021, Toyota Motor Corporation temporarily halted production at two factories in Japan due to semiconductor shortages, impacting their data monetization initiatives and overall market growth during the pandemic.

- The Russia-Ukraine war significantly impacted the automotive data monetization market by disrupting supply chains and exacerbating semiconductor shortages. With Ukraine being a key supplier of wire harnesses and other critical components, production halts occurred across major European automakers. Consequently, the inability to procure essential parts delayed the rollout of connected vehicle technologies necessary for data monetization initiatives. This disruption hindered manufacturers' ability to leverage data analytics and advanced technologies, ultimately stalling their progress in monetizing automotive data and realizing potential revenue streams during a critical growth phase in the industry.

Key Takeaways:

-

OEM Holds the Largest Market Share

Based on provider type, OEM held the highest segmental market share of around 56.3% in 2023. As vehicles become increasingly interconnected, OEMs are uniquely positioned to leverage vast amounts of data generated by connected vehicles. This data encompasses vehicle performance, driver behavior, and diagnostics, which can be monetized through innovative business models. By adopting data-driven strategies, OEMs can enhance customer experiences, optimize operations, and create new revenue streams. The market is driven by advancements in artificial intelligence and machine learning. OEMs face challenges in effectively monetizing this data, necessitating robust partnerships and technological integration. As the automotive landscape evolves, OEMs must prioritize data management and security to build consumer trust and comply with regulatory standards. Ultimately, the OEM provider type is essential for unlocking the full potential of automotive data monetization, transforming vehicles into valuable data assets that drive business growth.

-

Platform Solution to Retain the Largest Market Share

Based on the solution, Platform held the highest segmental market share of around 63.9% in 2023. By leveraging advanced data management systems, OEMs can securely capture, analyze, and monetize vast amounts of data from connected vehicles. This platform facilitates seamless data exchange among stakeholders, ensuring compliance with privacy regulations while enhancing service offerings. Furthermore, it enables the development of innovative business models, such as subscription services and data-as-a-service (DaaS), tailored to various market needs. Through strategic partnerships and robust analytics, companies can derive actionable insights that drive operational efficiency and customer engagement. The integration of blockchain technology enhances transaction transparency and security, making data sharing more efficient. Ultimately, this platform not only supports revenue generation but also fosters a collaborative ecosystem that enhances the overall value proposition for automakers and consumers alike, positioning them competitively in a rapidly evolving market landscape.

-

Direct Type to Maintain the Largest Market Share

Based on the type, Direct held the highest segmental market share of around 55.4% in 2023. The direct type in the automotive data monetization market involves the sale of raw vehicle data to third parties. This approach enables automakers to generate additional revenue by leveraging the vast amounts of data generated by connected cars, such as driving patterns, vehicle diagnostics, and location-based information. Direct data monetization presents a significant opportunity for automakers to diversify their revenue streams beyond traditional vehicle sales and services. By selling data to insurance companies, government agencies, and mobility service providers, automakers can create new value-added offerings and enhance customer experiences. However, direct data monetization also raises concerns about data privacy, security, and regulatory compliance. Automakers must navigate complex legal and ethical considerations to ensure that data is collected, stored, and shared responsibly. Effective data governance strategies and transparent communication with customers are crucial for building trust and maintaining brand reputation in the direct automotive data monetization market.

-

Subscription Model Dominates the Market

Based on the license model, the Subscription Model held the highest segmental market share of around 63.38% in 2023. The subscription model in automotive data monetization has transformed how automakers and data providers deliver vehicle data services. By allowing users to access specific datasets through recurring payments, this model ensures continuous availability of crucial information. With flexible payment options—monthly, quarterly, or annually—subscribers can choose tiered service levels, gaining access to more comprehensive data and advanced features at higher tiers. This approach not only provides predictable revenue streams for providers but also lowers upfront costs for customers. Moreover, the subscription model supports various applications, including fleet management, where real-time vehicle performance data enhances operational efficiency, and insurance, enabling usage-based policies through continuous driving data. The collaboration between Here Technologies and Daimler Truck in January 2024 exemplifies the model's potential, as it aims to develop advanced driver assistance systems, further illustrating how subscription-based access to data can drive innovation and improve safety in the automotive sector.

-

Cloud Deployment Leads the Market

Based on the deployment, the Cloud held the highest segmental market share of around 78.1% in 2023. The cloud deployment type in the automotive data monetization market is pivotal for leveraging vast amounts of vehicle-generated data. By utilizing cloud infrastructure, automotive manufacturers can efficiently store, process, and analyze data collected from connected vehicles. This approach enables real-time analytics and insights, driving innovative services such as predictive maintenance and personalized user experiences. Furthermore, cloud solutions facilitate scalability, allowing manufacturers to adapt to increasing data volumes without significant upfront investments in physical infrastructure. In addition to operational efficiency, cloud deployment enhances collaboration among stakeholders in the automotive ecosystem. By providing a centralized platform for data sharing, manufacturers can engage with third-party service providers, insurers, and urban planners, thereby creating new revenue streams and business models. This interconnectedness fosters a data-driven culture, essential for developing advanced applications like autonomous driving and smart city integration. Ultimately, cloud deployment not only optimizes data monetization but also positions automotive companies to remain competitive in an evolving market landscape.

-

Usage Based Insurance Holds the Largest Market Share

Based on the applications, Usage Based Insurance (UBI) held the highest segmental market share of around 26.1% in 2023. Usage-Based Insurance is a prime example of how automotive data monetization is transforming the insurance industry. By leveraging the wealth of data generated by connected vehicles, insurers can now offer personalized policies based on actual driving behavior rather than broad risk profiles. Insurers gain granular insights into driving patterns, enabling more accurate risk assessment and fraud detection. This leads to reduced claims costs and improved profitability. Policyholders enjoy fairer premiums that reflect their driving habits, incentivizing safer driving and potentially lowering their insurance costs. Moreover, UBI programs foster stronger customer engagement by providing drivers with feedback on their driving performance and opportunities to improve. As the adoption of connected car technologies continues to rise, UBI will become an increasingly important tool for insurers to stay competitive and deliver value to their customers in the evolving automotive data ecosystem.

-

Insurance Remains the Largest End Use Industry

Based on the end user, Insurance Companies held the highest segmental market share of around 25.2% in 2023. The automotive data monetization market presents significant opportunities for insurance end users, leveraging driver behavior analytics to refine risk assessment and pricing models. By adopting telematics, insurers can implement usage-based insurance (UBI) models, enhancing customer engagement through personalized premiums. Additionally, real-time data from connected vehicles enables insurers to streamline claims processing and fraud detection, reducing operational costs. Collaborations with telematics service providers facilitate access to comprehensive data sets, allowing insurers to develop innovative products. As the market evolves, integrating advanced analytics will be crucial for insurers to extract actionable insights, ultimately driving profitability and customer satisfaction. By prioritizing data-driven strategies, insurance companies can transform challenges into competitive advantages, positioning themselves as leaders in the rapidly changing automotive landscape. This proactive approach not only enhances risk management but also fosters long-term relationships with policyholders, ensuring sustained growth in the automotive data monetization sector.

-

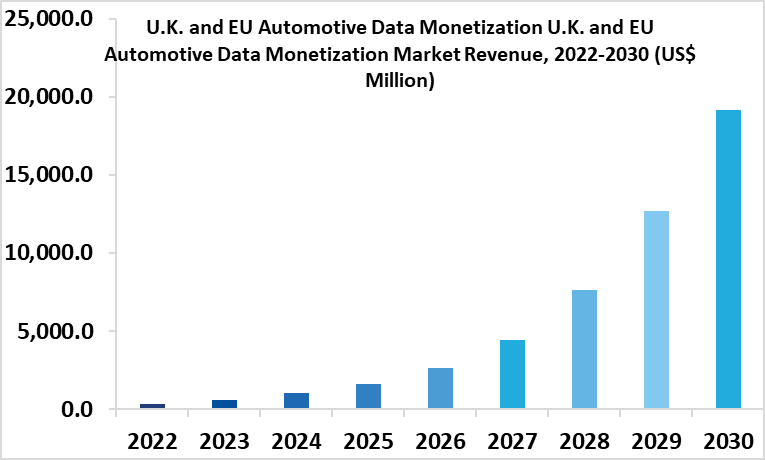

U.K. Region to Dominate the Market

Based on geography, U.K. held the highest segmental market share of around 23.2% in 2023. The U.K. automotive data monetization market has experienced significant growth due to the increasing integration of advanced technologies in vehicles. With the rise of connected cars and IoT, data generation surged, creating opportunities for predictive maintenance, usage-based insurance, and autonomous driving solutions. Strategic collaborations among automakers, tech firms, and telecom companies have enhanced data analytics capabilities, while adherence to GDPR has fostered consumer trust. The government's £4.5 billion investment in November 2023, including £150 million for Connected and Automated Mobility, further supports innovation in this sector. As electric and autonomous vehicles proliferate, the market is poised for continued expansion, driven by technological advancements and 5G adoption.

-

Growing Demand Due to Emergence of Mobility-as-a-Service (MaaS)

The emergence of Mobility-as-a-Service (MaaS) is a key driver of the automotive data monetization market. MaaS is a concept that integrates various modes of transportation, such as public transit, ride-sharing, and bike-sharing, into a single platform. MaaS relies on data from connected vehicles and other transportation modes to optimize routes, reduce congestion, and provide personalized recommendations to users. As MaaS becomes more widespread, the demand for automotive data will increase, driving the growth of the data monetization market.

-

Advancements in Vehicle-to-Everything (V2X) Communication Propels Market Demand

Advancements in V2X communication technologies, such as vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I), are driving the growth of the automotive data monetization market. V2X technologies enable vehicles to communicate with each other and with infrastructure, such as traffic lights and road sensors. This communication generates data that can be used for traffic management, accident prevention, and infrastructure optimization. As V2X technologies become more widespread, the amount of data generated will increase, providing more monetization opportunities.

-

Data Privacy and Cybersecurity Concerns Challenge Market Growth

As vehicles become increasingly connected, they generate vast amounts of sensitive data, including driver behavior, location, and personal preferences. This raises significant legal and ethical questions regarding data ownership and consent. Insurers and manufacturers must navigate complex regulations, such as GDPR, which impose strict guidelines on data usage and sharing. Moreover, the risk of cyberattacks targeting connected vehicles poses a direct threat to consumer safety and trust. A breach could not only compromise personal data but also lead to unauthorized access to vehicle systems, potentially endangering lives. Consequently, companies must invest heavily in robust cybersecurity measures and transparent data practices to build consumer confidence and comply with legal frameworks, which can strain resources and slow down the monetization process.

For more details on this report - Request for Sample

Key Market Players:

Product launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Automotive Data Monetization Market. The top 10 companies in this industry are listed below:

- BMW

- Volkswagen

- Ford Motor Company

- General Motors

- Honda Motor Co., Ltd.

- Daimler (Mercedes-Benz Group AG)

- Stellantis

- Toyota

- Hyundai

- Nissan

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024-2030 |

|

CAGR |

62.9% |

|

Market Size in 2030 |

$ 19.148 billion |

|

Segments Covered |

Provider Type, Solution, Type, License Model, Deployment, Application, End User and Region |

|

Regions Covered |

U.K. and EU (Germany, France, Spain, Italy, Belgium, Luxembourg, Netherlands, Switzerland and Rest of the European Union). |

|

Key Market Players |

|

For more Information and Communications Technology Market reports, please click here

The Automotive Data Monetization Market is projected to grow at 62.9% CAGR during the forecast period 2024-2030.

Automotive Data Monetization Market size is estimated to surpass $19.148 billion by 2030.

The leading players in the Automotive Data Monetization Market are BMW, Volkswagen, Ford Motor Company, General Motors, Honda Motor Co. Ltd., and others.

AI, Machine Learning, and Data-Driven Insights will shape the market in the future.

The growing demand for the Automotive Data Monetization market due to advancements in Vehicle to Everything Communication and increasing adoption of Mobility as a Service, which is expected to drive the market in the future.