Email

Email Print

Print

Data Center Infrastructure Management Market - By Component, By Functionality , By Tier Standards , By Data Center Size , By Deployment Model , By Industry Vertical and By Geography - Opportunity Analysis & Industry Forecast, 2024-2030.

Data Center Infrastructure Management Market Overview:

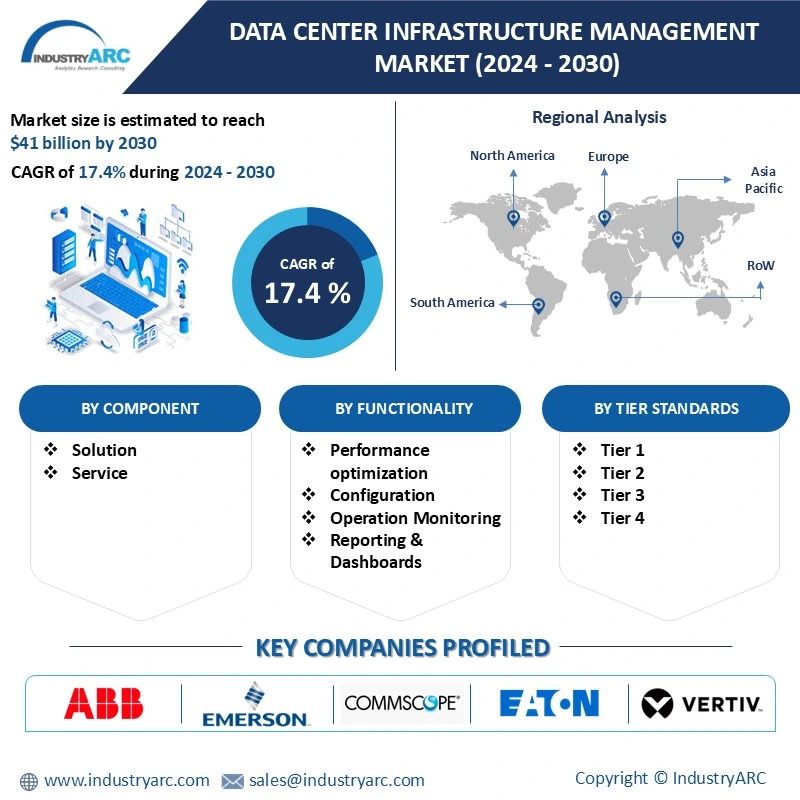

The Data Center Infrastructure Management Market size is estimated to reach $41 Billion by 2030, growing at a CAGR of 17.4% during the forecast period 2024-2030. Data Center Infrastructure Management (DCIM) refers to the integrated solution that helps manage and optimize the physical components and operations of data centers, such as servers, cooling systems, power supply and network infrastructure. It encompasses tools to monitor, control and analyze data center operations to ensure efficient energy usage, improve operational performance and reduce downtime. DCIM is essential for ensuring optimal resource utilization, minimizing operational costs, and maximizing the lifespan of critical infrastructure. The market for DCIM is driven by the increasing demand for data storage and processing power fueled by the growth of cloud computing, big data and IoT (Internet of Things). Additionally, the rising emphasis on energy efficiency and sustainability along with regulatory pressures to reduce carbon footprint is propelling the adoption of DCIM solutions. The growing complexity of data centers and the need for better management tools to handle scalability, security and uptime are further driving the market's expansion. As businesses increasingly rely on data-driven operations, DCIM solutions have become integral to ensuring efficient, cost-effective and secure data center operations.

Automation and remote management is a growing trend in the data center infrastructure market, with the increasing complexity of modern data centers, automation technologies such as AI-driven management systems, are becoming essential for managing vast amounts of data, optimizing energy usage and ensuring uptime. Remote management allows data centers to be monitored and controlled from anywhere, enabling operators to quickly address issues without needing on-site intervention. For example, in March 2024, Schneider Electric partnered with NVIDIA to optimize data center infrastructure by combining Schneider Electric's expertise in infrastructure management with NVIDIA's AI technologies. This collaboration aims to introduce the first publicly available AI data center reference designs which will allow for smarter, more automated management, improving performance, energy efficiency, and overall operational cost-effectiveness. Additionally, adoption of modular and scalable architectures is a also a growing trend in the data center infrastructure market as companies seek flexible and efficient solutions to support rapid growth in data demand. Hyperscale data centers, which are designed to accommodate massive amounts of data processing and storage, are increasingly adopting modular and scalable architectures that can be quickly expanded to meet evolving business needs without significant downtime or overhauling of existing infrastructure. For instance, in October 2024, data center firm Equinix formed a joint venture with Singapore's sovereign wealth fund GIC and the Canada Pension Plan Investment Board to raise over $15 billion in capital. This funding will be used to expand the U.S. footprint of hyperscale data centers which are characterized by their ability to scale quickly and offer immense networking capacity.

Market Snapshot:

Data Center Infrastructure Management Market- Report Coverage:

The “Data Center Infrastructure Management Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Data Center Infrastructure Management Market.

| Attribute | Segment |

|---|---|

|

By Component

|

|

|

By Functionality |

|

|

By Tier Standards |

|

|

By Data Centre Size |

|

|

By Deployment Model

|

|

|

By Industry Vertical

|

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

The COVID-19 pandemic caused disruptions in global supply chains, leading to delays in the procurement of hardware and software components for data centers. This slowed down the pace of DCIM adoption in some regions. Additionally, many companies faced budget constraints during the pandemic, leading to delayed investments in infrastructure management solutions. However, as remote work and digital services continued to be a norm, DCIM market experienced growth.

The geopolitical instability caused by the Russia-Ukraine war increased the need for robust data security, disaster recovery systems and redundancy in data center operations. With the ongoing uncertainty, companies are prioritizing the resilience of their IT infrastructure, pushing for more advanced DCIM solutions that can offer real-time monitoring, predictive analytics and enhanced security features. The conflict has also highlighted the vulnerability of centralized data centers leading to a shift toward distributed networks and hybrid cloud environments to mitigate risks.

Key Takeaways:

• North America Leads the Market:

North America accounted for largest market share in 2023 driven by the continued expansion of data center infrastructure, especially in the U.S. The demand for public cloud computing and associated services has been steadily increasing, further fueling the growth of data centers in the region. Additionally, the widespread adoption of cloud computing in North America, particularly in the U.S. led to a growing demand for efficient data center management solutions. According to a May 2024 article by Linklaters, North America maintained its lead in data center transaction values, accounting for 62% of the global total in 2023 and 69% of investments up to April 2024, with $15 billion invested, primarily driven by the U.S. Moreover, North America's ongoing digital transformation across various industries further boosts the need for high-performance data centers. Also, as per an October 2024 article by Blackstone, the U.S. is expected to see over $1 trillion invested in data centers over the next five years. This scale of investment underscores the region’s dominance, with the largest data center currently under construction expected to have an estimated 500 megawatts of capacity, equivalent to the power demand of 375,000 homes. With significant investments in data center expansion and modernization along with government and regulatory support for infrastructure and green energy initiatives, North America remains at the forefront of the DCIM market.

• Services to Register the Fastest Growth

The Services segment in the data center infrastructure market is expected to grow with the fastest CAGR during the forecast period driven by the increasing demand for cloud computing, artificial intelligence (AI) and machine learning technologies which require highly scalable and reliable infrastructure. As businesses increasingly shift to digital-first models, the need for comprehensive service solutions ranging from cloud hosting to interconnection services, is growing rapidly to ensure performance, flexibility, and efficiency. For instance, Amazon's $10 billion investment in Ohio data centers, announced in December 2024, reflects this trend. Amazon Web Services (AWS) announced that it will expand its cloud infrastructure to meet the growing demand for services that power AI, machine learning and data storage. This investment is particularly focused on providing the robust computing and networking capabilities necessary for the future of cloud services. Similarly, in September 2024, DE-CIX India launched its Data Center Interconnection Services which use high-speed packet-optical connectivity to link data centers across varying distances enabling more efficient and seamless data exchange. These services are crucial for businesses that require global connectivity and reliable data transmission across multiple data centers, which further highlights the rapid growth of service-driven solutions in the market.

• On-Premises Deployment is the Largest Segment

On-Premises Deployment continues to lead the data center infrastructure market due to enhanced control, security, customization and compliance with local regulations. For example, as per a september 2024 article by financial express, approximately 24% of organizations have indicated plans to move a portion of their data from the cloud to on-premise data centers within the next three years. This shift reflects growing concerns over data security, regulatory compliance, and the desire for more control over sensitive information and highlights the strong preference for on-premises infrastructure, despite the growing popularity of cloud services. Organizations particularly in industries like finance, government and healthcare continue to prioritize on-premises deployments due to stringent data privacy and regulatory requirements. Many organizations prefer on-premises solutions for critical workloads because they provide direct oversight of their IT systems ensuring that sensitive data is securely managed and operations are tailored to specific business needs. Furthermore, on-premises data centers are seen as more reliable for high-performance computing and mission-critical applications where any downtime could significantly impact business operations. For example, in December 2024, Sify Technologies launched a cutting-edge data center in New Delhi, built specifically for India’s Supreme Court. The facility, referred to as a futuristic on-premises data center, aims to bolster the court's IT infrastructure, ensuring that all IT services and computer applications remain highly available. The Supreme Court's investment in such a facility underscores the critical need for high-security, high-availability systems in government and legal sectors where data integrity and uninterrupted service are paramount.

• Growing Demand for Green Cloud Computing and Data Storage Boosts the Market

Growing demand for green cloud computing and data storage is becoming a significant driver in the data center industry as businesses and governments aim to reduce their carbon footprint and embrace sustainability. Based on projections by Schnieder Electric, by 2040, total data center energy consumption will reach 2,700 TWh. Green cloud computing combines advanced cloud technologies with environmentally friendly practices contributing to both technological innovation and environmental conservation. For instance, in March 2024, G42, an Abu Dhabi-based AI and cloud computing firm, partnered with Kenyan technology company EcoCloud to develop a green data center in Kenya. This data center powered by geothermal energy is expected to have an initial capacity of 100 megawatts. This development aligns with the growing trend of utilizing renewable energy sources to power data centers, reducing their reliance on fossil fuels and minimizing their environmental impact.

Cost of Maintenance and Upgrades to Hamper the Market

Cost of maintenance and upgrades remains a significant challenge in the data center infrastructure market. As technology evolves rapidly, maintaining and upgrading existing data centers to keep up with new hardware, software and security requirements can be costly for businesses. These costs can include everything from replacing outdated equipment and optimizing infrastructure for better efficiency to ensure compliance with new regulatory standards. Additionally, the physical space, energy consumption and cooling requirements of modern data centers further add to the maintenance burden making it a complex and expensive endeavor for organizations to stay competitive in the market. For example, upgrading to energy-efficient systems, implementing cutting-edge security protocols or scaling up to accommodate growing data demands often requires substantial financial investments. Furthermore, the need to employ skilled technicians for regular maintenance and emergency repairs can also drive up operational expenses. These costs can be particularly challenging for smaller businesses or those with tight budgets potentially hindering their ability to adopt the latest technologies and maintain an optimized, high-performance data center. Thus, the rising expenses tied to regular maintenance and necessary upgrades continue to pose a significant challenge for companies operating in the data center space.

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Data Center Infrastructure Management Market. The top 10 companies in this industry are listed below:

1. ABB Ltd.

2. Emerson Electric Co

3. Commscope, Inc.

4. Eaton Corporation

5. Vertiv Group Corp.

6. Schneider Electric SE

7. Johnson Controls International PLC

8. IBM Corporation

9. Huawei

10. Cisco Systems Inc.

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

17.4% |

|

Market Size in 2030 |

$41 Billion |

|

Segments Covered |

By Component, By Functionality, By Tier Standards, By Data Center Size, By Deployment Model, By Industry Vertical and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, , Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

Relevant reports:

Data Center Market - Industry Analysis, Market Size, Share, Trends, Application Analysis, Growth and Forecast Analysis

Report Code: ITR 0306

Next Generation Data Center Market - Industry Analysis, Market Size, Share, Trends, Application Analysis, Growth and Forecast Analysis

Report Code: ESR 0216

Data Center As a Service Market - Industry Analysis, Market Size, Share, Trends, Application Analysis, Growth and Forecast Analysis

Report Code: ITR 0129

1. Data Center Infrastructure Management Market- Market Overview

1.1 Definitions and Scope

2. Data Center Infrastructure Management Market- Executive Summary

2.1 Key trends by Component

2.2 Key trends by Functionality

2.3 Key trends by Tier Standards

2.4 Key trends by Data Center Size

2.5 Key trends by Deployment Model

2.6 Key trends by Industry Vertical

2.7 Key trends by Geography

3. Data Center Infrastructure Management Market– Landscape

3.1 Comparative analysis

3.1.1 Market Share Analysis- Major Companies

3.1.2 Product Benchmarking- Major Companies

3.1.3 Major 5 Financials Analysis

3.1.4 Patent Analysis- Top Companies

3.1.5 Pricing Analysis (ASPs will be provided)

4. Data Center Infrastructure Management Market- Startup companies Scenario Premium

4.1 Top startup company Analysis by

4.1.1 Investment

4.1.2 Revenue

4.1.3 Market Shares

4.1.4 Market Size and Application Analysis

4.1.5 Venture Capital and Funding Scenario

5. Data Center Infrastructure Management Market– Industry Market Entry Scenario Premium

5.1 Regulatory Framework Overview

5.2 New Business and Ease of Doing business index

5.3 Successful venture profiles

5.4 Customer Analysis – Major companies

6. Data Center Infrastructure Management Market- Market Forces

6.1 Market Drivers

6.2 Market Constraints

6.3 Porters Five Force Model

6.3.1 Bargaining Power of Suppliers

6.3.2 Bargaining Powers of Buyers

6.3.3 Threat of New Entrants

6.3.4 Competitive Rivalry

6.3.5 Threat of Substitutes

7. Data Center Infrastructure Management Market– Strategic Analysis

7.1 Value/Supply Chain Analysis

7.2 Opportunity Analysis

7.3 Product/Market Life Cycle

7.4 Distributor Analysis – Major Companies

8. Data Center Infrastructure Management Market- By Component (Market Size -$Million / $Billion)

8.1 Solution

8.1.1 Asset Management

8.1.2 Network Management

8.1.3 Cooling Management

8.1.4 Power Management

8.1.5 Security Management

8.1.6 Others

8.2 Service

8.2.1 Installation & Integration

8.2.2 Design & Consulting

8.2.3 Support & Maintenance

8.2.4 Others

9. Data Center Infrastructure Management Market- By Functionality (Market Size -$Million / $Billion)

9.1 Performance optimization

9.2 Configuration

9.3 Operation Monitoring

9.4 Reporting & Dashboards

9.5 Others

10. Data Center Infrastructure Management Market- By Tier Standards (Market Size -$Million / $Billion)

10.1 Tier 1

10.2 Tier 2

10.3 Tier 3

10.4 Tier 4

11. Data Center Infrastructure Management Market- By Data Center Size (Market Size -$Million / $Billion)

11.1 Small Data Center

11.2 Medium Data Center

11.3 Large Data Center

12. Data Center Infrastructure Management Market- By Deployment Model (Market Size -$Million / $Billion)

12.1 On-Premises

12.2 Cloud

13. Data Center Infrastructure Management Market- By Industry Vertical (Market Size -$Million / $Billion)

13.1 Banking, Financial Services and Insurance

13.2 Government and Public Sector

13.3 Healthcare and Life Sciences

13.4 IT and ITeS

13.5 Manufacturing

13.6 Telecommunications

13.7 Education

13.8 Media & Entertainment

13.9 Retail & Ecommerce

13.10 Others

14. Data Center Infrastructure Management Market- By Geography

14.1 North America

14.1.1 USA

14.1.2 Canada

14.1.3 Mexico

14.2 Europe

14.2.1 UK

14.2.2 Germany

14.2.3 France

14.2.4 Italy

14.2.5 Netherlands

14.2.6 Spain

14.2.7 Russia

14.2.8 Belgium

14.2.9 Rest of Europe

14.3 Asia-Pacific

14.3.1 China

14.3.2 Japan

14.3.3 India

14.3.4 South Korea

14.3.5 Indonesia

14.3.6 Taiwan

14.3.7 Malaysia

14.3.8 Australia and New Zealand

14.3.9 Rest of APAC

14.4 South America

14.4.1 Brazil

14.4.2 Argentina

14.4.3 Colombia

14.4.4 Chile

14.4.5 Rest of South America

14.5 Rest of the World

14.5.1 Middle East

14.5.2 Africa

15. Data Center Infrastructure Management Market– Entropy

15.1 New Product Launches

15.2 M&As, Collaborations, JVs and Partnerships

16. Data Center Infrastructure Management Market– Market Share Analysis

16.1 Market Share at Global Level - Major companies

16.2 Market Share by Key Region - Major companies

16.3 Market Share by Key Country - Major companies

16.4 Market Share by Key Application - Major companies

16.5 Market Share by Key Product Type/Product category - Major companies

17. Data Center Infrastructure Management Market– Key Company List by Country Premium

18. Data Center Infrastructure Management Market Company Analysis

18.1 ABB Ltd.

18.2 Emerson Electric Co

18.3 Commscope, Inc.

18.4 Eaton Corporation

18.5 Vertiv Group Corp.

18.6 Schneider Electric SE

18.7 Johnson Controls International PLC

18.8 IBM Corporation

18.9 Huawei

18.10 Cisco Systems Inc.

"Financials to the Private Companies would be provided on a best-effort basis."

Connect with our experts to get customized reports that best suit your requirements. Our

reports include global-level data, niche markets, and competitive landscape.

The Data Center Infrastructure Management Market is projected to grow at 17.4% CAGR during the forecast period 2024-2030.\\r\\n\\r\\n

The Data Center Infrastructure Management Market size is estimated to be $12.8 million in 2023 and is projected to reach $41 Billion by 2030.

The leading players in the market are ABB Ltd., Emerson Electric Co, Commscope, Inc., Eaton Corporation, Vertiv Group Corp and Others.\\r\\n\\r\\n

Automation and remote management are some of the major Data Center Infrastructure Management market trends in the industry which will create growth opportunities for the market during the forecast period.

Key driving factors include digital transformation across industries, the expansion of IoT and big data, the increasing demand for energy-efficient data management and the need for scalable, secure, and reliable data center infrastructure solutions.\\r\\n\\r\\n