Wafer Level Packaging Market Overview:

Wafer Level Packaging Market size is estimated to reach $19.6 billion by 2030, growing at a CAGR of 15.4% during the forecast period 2024-2030. Rising adoption of IoT and AI technologies in the automotive sector, increasing demand for ultra-thin wafer and government initiatives to promote the adoption of advanced

packaging technologies are propelling the Wafer Level Packaging Market growth.

Additionally, Growing penetration of miniaturized semiconductor components in consumer electronics sectors is creating substantial growth opportunities for the Wafer Level Packaging Market. These factors positively influence the Wafer Level Packaging industry outlook during the forecast period.

Wafer Level Packaging Market - Report Coverage:

The “Wafer Level Packaging Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Wafer Level Packaging Market.

| Attribute |

Segment |

|

By Type

|

-

3D TSV WLP

-

2.5D TSV WLP

-

WLCSP

-

eWLB

-

Others

|

|

By Technology

|

|

|

By Integration

|

|

|

By End-Use

|

-

Consumer Electronics

-

IT and Telecommunication

-

Automotive

-

Healthcare

-

Others

|

|

By Geography

|

-

North America (U.S., Canada and Mexico)

-

Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe),

-

Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific),

-

South America (Brazil, Argentina, Chile, Colombia and Rest of South America)

-

Rest of the World (Middle East and Africa).

|

COVID-19 / Ukraine Crisis - Impact Analysis:

● The COVID-19 pandemic significantly impacted the wafer level packaging market. The initial outbreak disrupted the global supply chain and led to a temporary decline in demand. However, the market quickly recovered as digital infrastructure and remote connectivity became more critical during the pandemic. Lockdowns fueled the demand for electronic devices like smartphones, laptops, and gaming consoles, driving the need for efficient packaging solutions like wafer level packaging. Additionally, the pandemic accelerated trends such as remote work, online learning, and e-commerce, further boosting the demand for semiconductor devices and contributing to the market's recovery.

● The conflict between Russia and Ukraine significantly impacted the wafer level packaging (WLP) market. Geopolitical tensions and economic instability in the region affected the WLP industry, resulting in uncertainties and disruptions in global supply chains. The industry heavily relied on a vast network of suppliers and manufacturers, facing significant challenges due to disruptions in the flow of raw materials and components. These disruptions adversely affected production capabilities, leading to delays in deliveries. Furthermore, the crisis created an atmosphere of uncertainty and caution among investors, leading to cautious investment decisions and potentially hampering market growth.

Key Takeaways:

● Fastest Growth Asia-Pacific Region

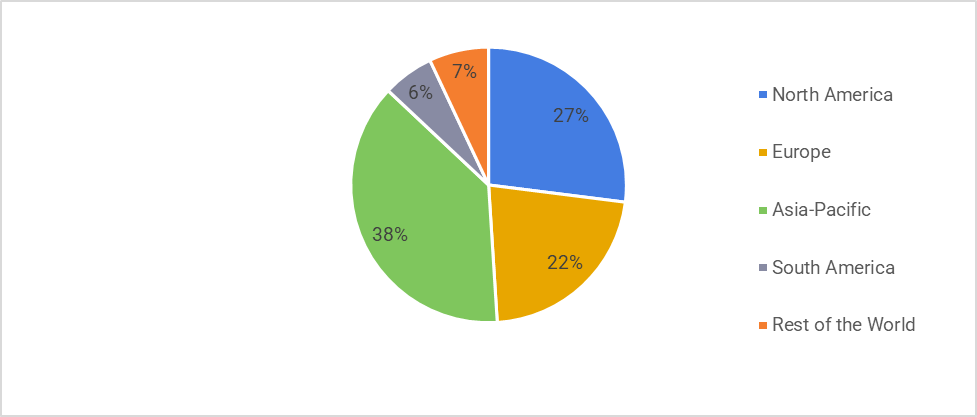

Geographically, Asia Pacific is expected to grow with the highest CAGR of around 17.1% during the forecast period 2024-2030 owing to the increasing adoption of consumer electronics, automotive electronics, and IoT devices in the region is further fueling the demand for advanced packaging technologies. The availability of skilled labor, favorable government initiatives, and investments in research and development also contribute to the region's rapid growth in the WLP market.

● Fan Out Wafer Level Packaging to Register the Fastest Growth

The Gas segment is projected to grow with at highest CAGR during the forecast period. FOWLP offers higher integration density, improved electrical performance, and heterogeneous integration capabilities, making it a preferred choice for advanced packaging requirements. The demand for FOWLP has surged in applications such as 5G, artificial intelligence, and high-performance computing, driving its rapid growth in the market.

● IT and Telecommunication is Leading the Market

The IT and Telecommunication segment held a significant market share in 2023. The industry's constant demand for advanced electronic devices, such as smartphones, tablets, routers, and servers, drives the adoption of WLP solutions. The need for compact, high-performance components in telecommunications equipment and the increasing deployment of 5G networks further contribute to the industry's dominance.

● The Surging Demand for IoT and AI Technologies in the Automotive Sector

The automotive industry is increasingly integrating IoT and AI capabilities into vehicles for enhanced connectivity, advanced driver assistance systems, and autonomous driving. These technologies require high-performance and miniaturized electronic components, which are facilitated by WLP solutions. The demand for efficient packaging solutions that offer compactness, reliability and improved electrical performance to support IoT and AI functionalities in vehicles is fueling the growth of the WLP market in the automotive sector.

● The Escalating Trend of Ultra-Thin Wafers Adoption

Electronic devices are continuing to become smaller and more compact, driving the need for thinner wafers. Ultra-thin wafers offer advantages such as a reduced form factor, improved thermal performance, and enhanced electrical properties. WLP technology provides an ideal packaging solution for these thin wafers, enabling high-density integration and efficient thermal management. The trend towards ultra-thin wafer adoption across industries such as consumer electronics, automotive, and healthcare is fueling the growth of the WLP market, as manufacturers seek advanced packaging solutions to meet these demands.

● High Costs Hamper the Market Growth

The wafer level packaging (WLP) industry requires substantial investments in specialized equipment, materials, and technologies, which are expensive. These costs present challenges for companies, especially small and medium-sized enterprises, restricting their entry or expansion in the market. Additionally, the complexity of WLP processes and the need for skilled labor contribute to overall expenses. Consequently, the high costs associated with wafer level packaging hinder market growth and potentially limit its adoption in industries like consumer electronics, automotive, and telecommunications.

Wafer Level Packaging Market Share (%) By Region, 2023

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Wafer Level Packaging Market. The top 10 companies in this industry are listed below:

1. China Wafer Level CSP Co. Ltd.

2. Chipbond Technology Corporation

3. ChipMOS TECHNOLOGIES INC.

4. Deca Technologies Inc.

5. Fujitsu Limited

6. Advanced Semiconductor Engineering, Inc.

7. Taiwan Semiconductor Manufacturing Company Limited

8. Amkor Technology, Inc

9. JCET Group

10. Nepes Corporation

Scope of the Report:

| Report Metric |

Details |

|

Base Year Considered

|

2023

|

|

Forecast Period

|

2024–2030

|

|

CAGR

|

15.4%

|

|

Market Size in 2030

|

$19.6 billion

|

|

Segments Covered

|

Type, Technology, Integration, End-Use and Region

|

|

Geographies Covered

|

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa).

|

|

Key Market Players

|

● China Wafer Level CSP Co. Ltd.

● Chipbond Technology Corporation

● ChipMOS TECHNOLOGIES INC.

● Deca Technologies Inc.

● Fujitsu Limited

● Advanced Semiconductor Engineering, Inc.

● Taiwan Semiconductor Manufacturing Company Limited

● Amkor Technology, Inc

● JCET Group

● Nepes Corporation

|

For More Electronics Market Research and Consulting Services: Click Here

Email

Email Print

Print