Email

Email Print

Print

Automated Guided Vehicle Market – Forecast, 2024-2030

Automated Guided Vehicle Market Overview:

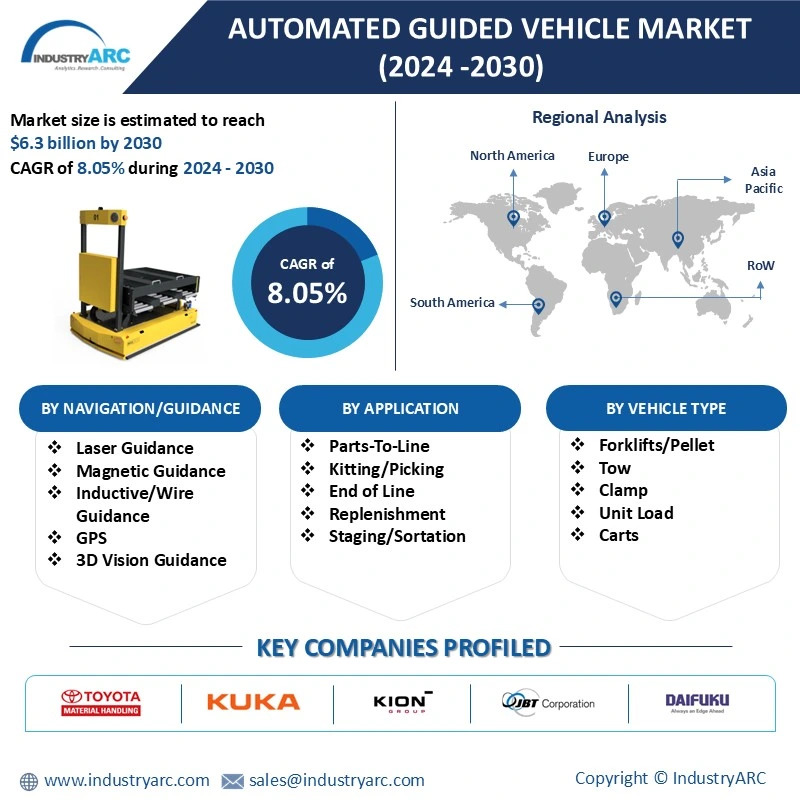

Automated Guided Vehicle Market Size is valued at $5900 Million by 2030, and is anticipated to grow at a CAGR of 7% during the forecast period 2024 -2030. Automated Guided Vehicles (AGVs) are innovative, self-operating machines that utilize predefined routes or cutting-edge technologies such as lasers and GPS for navigation. These vehicles are increasingly utilized in warehousing, manufacturing, and logistics, significantly enhancing material handling and inventory management processes.

Current trends highlight their integration with Industry 4.0 technologies, a surge in e-commerce demand, and their growing adoption in sectors like retail and pharmaceuticals that prioritize efficiency and labor cost reduction. As businesses strive for operational excellence, AGVs play a crucial role in streamlining workflows and improving productivity across various industries.

Market Snapshot:

Automated Guided Vehicle Market - Report Coverage:

The “Automated Guided Vehicle Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Automated Guided Vehicle Market.

|

Attribute |

Segment |

|

By Navigation/Guidance |

|

|

By Application |

|

|

By Vehicle Type |

|

|

By Application |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic significantly accelerated the adoption of Automated Guided Vehicles (AGVs) as industries grappled with labor shortages and surging e-commerce demands. AGVs facilitated social distancing by automating tasks in warehouses and production environments, ensuring continuous operations. However, the market faced temporary setbacks due to supply chain disruptions and halted manufacturing activities. As businesses emerged from the pandemic, there was a renewed focus on resilience, further driving AGV demand, particularly in logistics and healthcare sectors. This shift underscores the critical role of automation in enhancing operational efficiency and addressing workforce challenges in a post-pandemic landscape.

- The Russia-Ukraine war has significantly impacted the Automated Guided Vehicle (AGV) market by disrupting global supply chains and limiting access to essential electronic components and raw materials. European markets, heavily reliant on trade routes through the affected region, faced delays in AGV production and deployment. Despite these challenges, the geopolitical tensions have heightened the demand for automated solutions as industries seek to enhance operational efficiency and address workforce shortages. This shift underscores the growing importance of AGVs in maintaining productivity and resilience amidst ongoing disruptions in logistics and manufacturing sectors.

Key Takeaways:

- Growing Demand of Automated Guided Vehicles (AGVs) in Warehousing & Distribution Sector

Automated Guided Vehicles (AGVs) are rapidly gaining traction across various industries, with material handling in warehouses and factories emerging as the most prominent application. This segment is expected to grow at a robust compound annual growth rate (CAGR) of 10.67% during the forecast period, driven by the increasing adoption of automation to reduce human errors and enhance operational efficiency. Automation is transforming industrial processes by minimizing manual intervention and streamlining tasks ranging from basic operations to complex workflows. Beyond material handling, AGVs are widely utilized for staging, sorting, cross-docking, replenishment, picking, and trash removal, all of which contribute significantly to the market's revenue growth. These diverse applications have created opportunities for AGV manufacturers to innovate and offer tailored solutions such as laser-guided vehicles (LGVs), Automated Guided Carts (AGCs), Fahrerlose Transport Systems (FTS), motorized roller conveyors, pallet trucks, and Assembly Line Vehicles (ALVs). The growing demand for specialized AGVs tailored to the unique needs of different industries underscores the importance of customization in driving the market forward.

- Rising Need for Automated Guided Vehicles Driven by Increased Production and Efficiency

Automated Guided Vehicles (AGVs) are transforming industrial production by performing repetitive tasks with exceptional precision while lowering operational costs. Unlike human workers, AGVs can operate continuously without fatigue, significantly increasing output and optimizing workflows. This relentless operation not only enhances productivity but also improves return on investment, allowing industries to scale their production capabilities without interruptions. Moreover, AGVs play a crucial role in optimizing labor allocation by taking over mundane tasks, enabling human workers to focus on more complex and value-added activities. This shift not only boosts overall industrial efficiency but also enhances competitiveness in a rapidly evolving market. As businesses increasingly adopt AGVs, they are better positioned to meet growing demands while maintaining high standards of quality and efficiency. The integration of AGVs into production processes represents a significant step towards achieving operational excellence in various sectors, including manufacturing, logistics, and warehousing.

- Negative Impact on the Automated Guided Vehicle Market Due to Safety Risks

Automated Guided Vehicles (AGVs) present safety challenges, particularly in environments where they share space with humans or other machinery. The risk of collisions can arise from inefficient programming or sensor malfunctions, leading to operational hazards that may deter businesses from adopting this technology. To ensure safe operations, it is essential to implement stringent safety protocols and utilize advanced navigation technologies that enhance the reliability of AGVs. These measures can significantly reduce the likelihood of accidents and promote a safer working environment. Additionally, continuous monitoring and regular maintenance of AGV systems are vital to address potential issues proactively. As companies seek to integrate AGVs into their workflows, addressing safety concerns will be crucial for achieving widespread market penetration. By prioritizing safety and investing in robust technological solutions, industries can harness the benefits of AGVs while ensuring the well-being of their workforce and operational integrity.

Key Market Players:

Product launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Automated Guided Vehicle Market. The top 10 companies in this industry are listed below:

- Daifuku

- JBT Corporation

- KION Group

- KUKA

- Toyota Material Handling

- Hyster-Yale Materials Handling

- Kollmorgen

- EK Automation

- Seegrid Corporation

- SSI Schaeffler

Scope of the Report:

|

Details |

|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024-2030 |

|

CAGR |

8.05% |

|

Market Size in 2030 |

$6.3 billion |

|

Segments Covered |

By Navigation/Guidance, By Application, By Vehicle Type, By End Use Industry, and By Region |

|

Regions Covered |

North America (USA, Canada, and Mexico), Europe (UK, Germany, France, Italy, Netherlands, Spain, Russia, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia, Indonesia, Malaysia, and Rest of APAC), South America (Brazil, Argentina, Colombia, Chile, and Rest of South America), and Rest of the World (Middle East, and Africa). |

|

Key Market Players |

|

For more Automation and Instrumentation Market reports, please click here

1.1. Definitions and Scope

2. Automated Guided Vehicle Market - Executive summary

2.1. Market Revenue, Market Size and Key Trends by Company

2.2. Key Trends by type of Application

2.3. Key Trends segmented by Geography

3. Automated Guided Vehicle Market

3.1. Comparative analysis

3.1.1. Product Benchmarking - Top 10 companies

3.1.2. Top 5 Financials Analysis

3.1.3. Market Value split by Top 10 companies

3.1.4. Patent Analysis - Top 10 companies

3.1.5. Pricing Analysis

4. Automated Guided Vehicle Market – Startup companies Scenario Premium

4.1. Top 10 startup company Analysis by

4.1.1. Investment

4.1.2. Revenue

4.1.3. Market Shares

4.1.4. Market Size and Application Analysis

4.1.5. Venture Capital and Funding Scenario

5. Automated Guided Vehicle Market – Industry Market Entry Scenario Premium

5.1. Regulatory Framework Overview

5.2. New Business and Ease of Doing business index

5.3. Case studies of successful ventures

5.4. Customer Analysis – Top 10 companies

6. Automated Guided Vehicle Market Forces

6.1. Drivers

6.2. Constraints

6.3. Challenges

6.4. Porters five force model

6.4.1. Bargaining power of suppliers

6.4.2. Bargaining powers of customers

6.4.3. Threat of new entrants

6.4.4. Rivalry among existing players

6.4.5. Threat of substitutes

7. Automated Guided Vehicle Market - Strategic analysis

7.1. Value chain analysis

7.2. Opportunities analysis

7.3. Product life cycle

7.4. Suppliers and distributors Market Share

8. Automated Guided Vehicle Market – By Navigation/Guidance (Market Size -$Million / $Billion)

8.1. Market Size and Market Share Analysis

8.2. Application Revenue and Trend Research

8.3. Product Segment Analysis

8.3.1. Laser Guidance

8.3.2. Magnetic Guidance

8.3.3. Inductive/Wire Guidance

8.3.4. GPS

8.3.5. 3D Vision Guidance

8.3.6. Others

9. Automated Guided Vehicle Market – By Application (Market Size -$Million / $Billion)

9.1. Parts-To-Line

9.2. Kitting/Picking

9.3. End of Line

9.4. Replenishment

9.5. Staging/Sortation

9.6. Cross Docking

9.7. Trash Removal

9.8. Others

10. Automated Guided Vehicle Market – By Vehicle Type (Market Size -$Million / $Billion)

10.1. Forklifts/Pellet

10.2. Tow

10.3. Clamp

10.4. Unit Load

10.5. Carts

10.6. Heavy Burden Carrier

10.7. Others

11. Automated Guided Vehicle – By End Use Industry(Market Size -$Million / $Billion)

11.1. Segment type Size and Market Share Analysis

11.2. Application Revenue and Trends by type of Application

11.3. Application Segment Analysis by Type

11.3.1. Automotive Industry

11.3.2. Manufacturing Industry

11.3.3. Chemical and Pharmaceutical Industries

11.3.4. Aerospace Industry

11.3.5. Paper Industry

11.3.6. Food and Beverage Industry

11.3.7. Warehousing and distribution

11.3.8. Others

12. Automated Guided Vehicle - By Geography (Market Size -$Million / $Billion)

12.1. Automated Guided Vehicle Market - North America Segment Research

12.2. North America Market Research (Million / $Billion)

12.2.1. Segment type Size and Market Size Analysis

12.2.2. Revenue and Trends

12.2.3. Application Revenue and Trends by type of Application

12.2.4. Company Revenue and Product Analysis

12.2.5. North America Product type and Application Market Size

12.2.5.1. U.S.

12.2.5.2. Canada

12.2.5.3. Mexico

12.2.5.4. Rest of North America

12.3. Automated Guided Vehicle - South America Segment Research

12.4. South America Market Research (Market Size -$Million / $Billion)

12.4.1. Segment type Size and Market Size Analysis

12.4.2. Revenue and Trends

12.4.3. Application Revenue and Trends by type of Application

12.4.4. Company Revenue and Product Analysis

12.4.5. South America Product type and Application Market Size

12.4.5.1. Brazil

12.4.5.2. Venezuela

12.4.5.3. Argentina

12.4.5.4. Ecuador

12.4.5.5. Peru

12.4.5.6. Colombia

12.4.5.7. Costa Rica

12.4.5.8. Rest of South America

12.5. Automated Guided Vehicle - Europe Segment Research

12.6. Europe Market Research (Market Size -$Million / $Billion)

12.6.1. Segment type Size and Market Size Analysis

12.6.2. Revenue and Trends

12.6.3. Application Revenue and Trends by type of Application

12.6.4. Company Revenue and Product Analysis

12.6.5. Europe Segment Product type and Application Market Size

12.6.5.1. U.K

12.6.5.2. Germany

12.6.5.3. Italy

12.6.5.4. France

12.6.5.5. Netherlands

12.6.5.6. Belgium

12.6.5.7. Spain

12.6.5.8. Denmark

12.6.5.9. Rest of Europe

12.7. Automated Guided Vehicle – APAC Segment Research

12.8. APAC Market Research (Market Size -$Million / $Billion)

12.8.1. Segment type Size and Market Size Analysis

12.8.2. Revenue and Trends

12.8.3. Application Revenue and Trends by type of Application

12.8.4. Company Revenue and Product Analysis

12.8.5. APAC Segment – Product type and Application Market Size

12.8.5.1. China

12.8.5.2. Australia

12.8.5.3. Japan

12.8.5.4. South Korea

12.8.5.5. India

12.8.5.6. Taiwan

12.8.5.7. Malaysia

13. Automated Guided Vehicle Market - Entropy

13.1. New product launches

13.2. M&A's, collaborations, JVs and partnerships

14. Automated Guided Vehicle Market – Industry / Segment Competition landscape Premium

14.1. Market Share Analysis

14.1.1. Market Share by Country- Top companies

14.1.2. Market Share by Region- Top 10 companies

14.1.3. Market Share by type of Application – Top 10 companies

14.1.4. Market Share by type of Product / Product category- Top 10 companies

14.1.5. Market Share at global level- Top 10 companies

14.1.6. Best Practices for companies

15. Automated Guided Vehicle Market – Key Company List by Country Premium

16. Automated Guided Vehicle Market Company Analysis

16.1. Market Share, Company Revenue, Products, M&A, Developments

16.2. ABB Ltd.

16.3. Siemens AG

16.4. Doerfer Corporation

16.5. Egemin Automation Inc.

16.6. Rockwell Automation, Inc.

16.7. Mitsubishi Corporation

16.8. Swisslog Holding AG(KUKA AG)

16.9. America In Motion, Inc.

16.10. SSI Schaefer

16.11. Transbotics, Inc

16.12. Kiva Systems, Inc.

16.13. KAMAG Transporttechnik GmbH & Co.

16.14. NDC Automation Pty., Ltd.

16.15. Komatsu Ltd.

16.16. John Bean Technologies Corporation

16.17. AGV Electronics Engelbert and Jarl AB

16.18. Seegrid Corporation

16.19. DS Automation GmbH

16.20. Ward Systems Inc.

16.21. KMH Systems Inc.

16.22. Company 21

16.23. Company 22

16.24. Company 23 and more

17. Automated Guided Vehicle Market - Appendix

17.1. Abbreviations

17.2. Sources

18. Automated Guided Vehicle Market - Methodology

18.1. Research Methodology

18.1.1. Company Expert Interviews

18.1.2. Industry Databases

18.1.3. Associations

18.1.4. Company News

18.1.5. Company Annual Reports

18.1.6. Application Trends

18.1.7. New Products and Product database

18.1.8. Company Transcripts

18.1.9. R&D Trends

18.1.10. Key Opinion Leaders Interviews

18.1.11. Supply and Demand Trends