Email

Email Print

Print

Carbon Capture and Storage (CCS) Market - Forecast(2025 - 2031)

Carbon Capture and Storage (CCS) Market Overview:

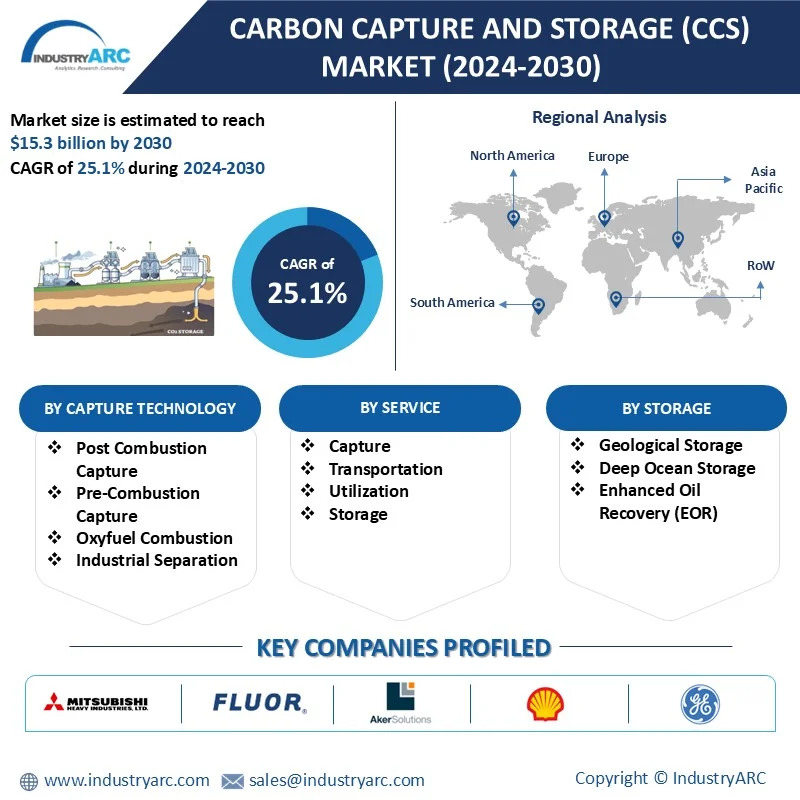

The Carbon Capture and Storage (CCS) Market size is estimated to reach $15.3 Billion by 2030, growing at a CAGR of 25.1% during the forecast period 2024-2030. The CCS market is attracting significant investments, bolstered by government subsidies and private sector funding. In the United States, the Inflation Reduction Act of 2022 enhanced tax credits for carbon capture projects, leading to substantial financial commitments from major institutions. For example, Bank of America invested $205 million in Harvestone Low Carbon Partners' ethanol plant in North Dakota, anticipating substantial tax credits over the next decade. Such financial incentives are pivotal in accelerating the deployment of CCS technologies across various industries.

Governments worldwide are implementing policies to facilitate CCS adoption as part of broader climate strategies. In the UK, the government approved the country's first commercially viable carbon storage facility, led by BP and Equinor, marking a significant step toward achieving net-zero emissions. This project is expected to capture millions of tonnes of CO₂ and store it under the North Sea, demonstrating strong policy support for CCS initiatives. Such regulatory developments are essential for providing the necessary framework and confidence for large-scale CCS investments. These factors positively influence the Carbon Capture and Storage (CCS) industry outlook during the forecast period.

Market Snapshot:

Carbon Capture and Storage (CCS) Market - Report Coverage:

The “Carbon Capture and Storage (CCS) Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Carbon Capture and Storage (CCS) Market.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

COVID-19 / Ukraine Crisis - Impact Analysis:

• The COVID-19 pandemic disrupted global industries, including the CCS market. Lockdowns and economic slowdowns led to decreased industrial activities, reducing carbon emissions and diminishing the immediate demand for CCS technologies. Additionally, supply chain interruptions and deferred investments hindered project timelines. However, as economies recover, there's a renewed emphasis on sustainable practices, positioning CCS as a pivotal component in achieving long-term carbon neutrality goals.

• The geopolitical tensions arising from the Ukraine crisis have significantly influenced the global energy landscape. Europe's efforts to reduce dependence on Russian energy sources have accelerated investments in alternative energy solutions, including CCS technologies. This shift aims to enhance energy security and meet climate objectives. Consequently, there's an increased focus on developing CCS infrastructure to support a diversified and resilient energy system.

Key Takeaways:

Asia Pacific is Projected as Fastest Growing Region

Asia Pacific is projected as the fastest growing region in Carbon Capture and Storage (CCS) Market with CAGR of 28.7% during the forecast period 2024-2030. The Asia-Pacific region is actively advancing Carbon Capture and Storage (CCS) technologies, driven by several key factors. Rapid industrialization has led to increased carbon emissions, prompting governments to implement stringent environmental regulations and adopt sustainable technologies. For instance, Japan has set ambitious net-zero emissions targets, fostering the development of CCS projects to meet these goals. The international collaborations are enhancing the development and deployment of CCS technologies. For instance, in 2024, Indonesia has signed agreements with neighboring countries to facilitate cross-border CO₂ storage, aiming to accelerate the growth of its CCS industry.

Oxyfuel Combustion Segment to Register the Fastest Growth

Oxyfuel Combustion segment is projected as the fastest growing segment in Carbon Capture and Storage (CCS) Market with CAGR of 26.1% during the forecast period 2024-2030. Oxyfuel combustion is a pivotal technology in the Carbon Capture and Storage (CCS) market, driven by several key factors. Primarily, it offers a more concentrated CO₂ stream, facilitating efficient capture and storage. Additionally, it reduces nitrogen oxide emissions, addressing environmental concerns. The technology's adaptability to existing power plants enhances its appeal, enabling retrofitting and reducing implementation costs. Furthermore, its potential for integration with other CCS technologies, such as chemical looping combustion, presents opportunities for improved efficiency and cost-effectiveness. These drivers collectively position oxyfuel combustion as a promising solution for mitigating greenhouse gas emissions.

Power Generation is Leading the Market

Power Generation held the largest market valuation in 2023. Governments worldwide are implementing stringent environmental regulations to meet climate goals. CCS technologies enable power plants to reduce carbon emissions, aligning with national and international commitments to mitigate climate change. For instance, the UK's commitment to achieving net-zero emissions by 2050 has spurred investments in CCS projects, such as the Teesside gas-fired power station, which aims to capture and store CO₂ emissions. These factors collectively contribute to the growing adoption of CCS technologies in the power generation sector, facilitating the transition to a more sustainable energy landscape.

Environmental and Climate Commitments

Environmental and climate commitments are pivotal drivers in the Carbon Capture and Storage (CCS) market. Governments worldwide are implementing stringent regulations and policies to reduce greenhouse gas emissions, thereby incentivizing industries to adopt CCS technologies. For instance, the U.S. Department of Energy announced a $3.5 billion program to create large-scale regional direct air capture hubs, underscoring the nation's dedication to climate goals. Similarly, the European Union aims to capture and store at least 450 million tons of CO₂ annually by 2050, highlighting the critical role of CCS in achieving decarbonization objectives. These initiatives reflect a global consensus on the necessity of CCS in mitigating climate change impacts.

High Operational Costs

Implementing Carbon Capture and Storage (CCS) technology entails substantial financial investment, encompassing the installation of capture systems, transportation infrastructure, and secure storage facilities. These significant expenses often deter companies from adopting CCS solutions, especially in the absence of robust financial incentives or regulatory mandates. The International Energy Agency (IEA) notes that the high costs associated with CCS are a primary factor limiting its widespread deployment. Without sufficient economic support mechanisms, such as tax credits or subsidies, the financial burden remains a formidable barrier to the integration of CCS technologies into industrial operations.

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Carbon Capture and Storage (CCS) Market. The top 10 companies in this industry are listed below:

1. General Electric Company

2. Royal Dutch Shell PLC

3. Aker Solutions ASA

4. Fluor Corporation

5. Mitsubishi Heavy Industries, Ltd

6. Halliburton Company

7. Siemens AG

8. Equinor ASA

9. Exxon Mobil Corporation

10. Schlumberger NV

Scope of the Report:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For more Chemicals and Materials Market reports, please click here

1.1 Definitions and Scope

2. Carbon Capture and Storage (CCS) Market - Executive Summary

2.1 Key Trends by Capture Technology

2.2 Key Trends by Storage Technology

2.3 Key Trends by End Use Industry

2.4 Key Trends by Geography

3. Carbon Capture and Storage (CCS) Market – Comparative analysis

3.1 Market Share Analysis- Major Companies

3.2 Product Benchmarking- Major Companies

3.3 Top 5 Financials Analysis

3.4 Patent Analysis- Major Companies

3.5 Pricing Analysis (ASPs will be provided)

4. Carbon Capture and Storage (CCS) Market - Startup companies Scenario Premium

4.1 Major startup company analysis:

4.1.1 Investment

4.1.2 Revenue

4.1.3 Product portfolio

4.1.4 Venture Capital and Funding Scenario

5. Carbon Capture and Storage (CCS) Market – Industry Market Entry Scenario Premium

5.1 Regulatory Framework Overview

5.2 New Business and Ease of Doing Business Index

5.3 Successful Venture Profiles

5.4 Customer Analysis – Major companies

6. Carbon Capture and Storage (CCS) Market - Market Forces

6.1 Market Drivers

6.2 Market Constraints

6.3 Porters Five Force Model

6.3.1 Bargaining Power of Suppliers

6.3.2 Bargaining Powers of Buyers

6.3.3 Threat of New Entrants

6.3.4 Competitive Rivalry

6.3.5 Threat of Substitutes

7. Carbon Capture and Storage (CCS) Market – Strategic Analysis

7.1 Value/Supply Chain Analysis

7.2 Opportunity Analysis

7.3 Product/Market Life Cycle

7.4 Distributor Analysis – Major Companies

8. Carbon Capture and Storage (CCS) Market – By Capture Technology (Market Size -$Million/Billion)

8.1 Post Combustion Capture

8.2 Pre-Combustion Capture

8.3 Oxyfuel Combustion

8.4 Industrial Separation

9. Carbon Capture and Storage (CCS) Market – By Storage Technology (Market Size -$Million/Billion)

9.1 Geological Storage

9.2 Deep Ocean Storage

9.3 Enhanced Oil Recovery (EOR)

10. Carbon Capture and Storage (CCS) Market – By End Use Industry (Market Size -$Million/Billion)

10.1 Power Generation

10.2 Iron and Steel

10.3 Oil and Gas

10.4 Chemicals

10.5 Cement and Concrete

10.6 Biofuels

10.7 Fertilizers

10.8 Textiles

10.9 Food and Beverages

10.10 Pulp and Paper

10.11 Others

11. Carbon Capture and Storage (CCS) Market - By Geography (Market Size -$Million/Billion)

11.1 North America

11.1.1 USA

11.1.2 Canada

11.1.3 Mexico

11.2 Europe

11.2.1 UK

11.2.2 Germany

11.2.3 France

11.2.4 Italy

11.2.5 Netherlands

11.2.6 Spain

11.2.7 Russia

11.2.8 Belgium

11.2.9 Rest of Europe

11.3 Asia-Pacific

11.3.1 China

11.3.2 Japan

11.3.3 India

11.3.4 South Korea

11.3.5 Australia and New Zeeland

11.3.6 Indonesia

11.3.7 Taiwan

11.3.8 Malaysia

11.3.9 Rest of APAC

11.4 South America

11.4.1 Brazil

11.4.2 Argentina

11.4.3 Colombia

11.4.4 Chile

11.4.5 Rest of South America

11.5 Rest of the World

11.5.1 Middle East

11.5.1.1 Saudi Arabia

11.5.1.2 UAE

11.5.1.3 Israel

11.5.1.4 Rest of the Middle East

11.5.2 Africa

11.5.2.1 South Africa

11.5.2.2 Nigeria

11.5.2.3 Rest of Africa

12. Carbon Capture and Storage (CCS) Market – Entropy

12.1 New Product Launches

12.2 M&As, Collaborations, JVs and Partnerships

13. Carbon Capture and Storage (CCS) Market – Industry/Segment Competition Landscape

13.1 Company Benchmarking Matrix – Major Companies

13.2 Market Share at Global Level - Major companies

13.3 Market Share by Key Region - Major companies

13.4 Market Share by Key Country - Major companies

13.5 Market Share by Key Application - Major companies

13.6 Market Share by Key Product Type/Product category - Major companies

14. Carbon Capture and Storage (CCS) Market – Key Company List by Country Premium

15. Carbon Capture and Storage (CCS) Market Company Analysis - Business Overview, Product Portfolio, Financials, and Developments

15.1 Aker Carbon Capture

15.2 Equinor ASA

15.3 Shell Plc

15.4 Exxon Mobil Corporation

15.5 TotalEnergies

"*Financials would be provided on a best effort basis for private companies"

List of Tables

Table 1: Carbon Capture and Storage (CCS) Market Overview 2023-2030

Table 2: Carbon Capture and Storage (CCS) Market Leader Analysis 2023-2024 (US$)

Table 3: Carbon Capture and Storage (CCS) Market Product Analysis 2023-2024 (US$)

Table 4: Carbon Capture and Storage (CCS) Market End User Analysis 2023-2024 (US$)

Table 5: Carbon Capture and Storage (CCS) Market Patent Analysis 2021-2023* (US$)

Table 6: Carbon Capture and Storage (CCS) Market Financial Analysis 2023-2024 (US$)

Table 7: Carbon Capture and Storage (CCS) Market Driver Analysis 2023-2024 (US$)

Table 8: Carbon Capture and Storage (CCS) Market Challenges Analysis 2023-2024 (US$)

Table 9: Carbon Capture and Storage (CCS) Market Constraint Analysis 2023-2024 (US$)

Table 10: Carbon Capture and Storage (CCS) Market Supplier Bargaining Power Analysis 2023-2024 (US$)

Table 11: Carbon Capture and Storage (CCS) Market Buyer Bargaining Power Analysis 2023-2024 (US$)

Table 12: Carbon Capture and Storage (CCS) Market Threat of Substitutes Analysis 2023-2024 (US$)

Table 13: Carbon Capture and Storage (CCS) Market Threat of New Entrants Analysis 2023-2024 (US$)

Table 14: Carbon Capture and Storage (CCS) Market Degree of Competition Analysis 2023-2024 (US$)

Table 15: Carbon Capture and Storage (CCS) Market Value Chain Analysis 2023-2024 (US$)

Table 16: Carbon Capture and Storage (CCS) Market Pricing Analysis 2023-2030 (US$)

Table 17: Carbon Capture and Storage (CCS) Market Opportunities Analysis 2023-2030 (US$)

Table 18: Carbon Capture and Storage (CCS) Market Product Life Cycle Analysis 2023-2030 (US$)

Table 19: Carbon Capture and Storage (CCS) Market Supplier Analysis 2023-2024 (US$)

Table 20: Carbon Capture and Storage (CCS) Market Distributor Analysis 2023-2024 (US$)

Table 21: Carbon Capture and Storage (CCS) Market Trend Analysis 2023-2024 (US$)

Table 22: Carbon Capture and Storage (CCS) Market Size 2023 (US$)

Table 23: Carbon Capture and Storage (CCS) Market Forecast Analysis 2023-2030 (US$)

Table 24: Carbon Capture and Storage (CCS) Market Sales Forecast Analysis 2023-2030 (Units)

Table 25: Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Capture Technology, 2023-2030 ($)

Table 26: Carbon Capture and Storage (CCS) Market By Capture Technology, Revenue & Volume, By Post Combustion Capture, 2023-2030 ($)

Table 27: Carbon Capture and Storage (CCS) Market By Capture Technology, Revenue & Volume, By Pre-Combustion Capture, 2023-2030 ($)

Table 28: Carbon Capture and Storage (CCS) Market By Capture Technology, Revenue & Volume, By Oxyfuel technology, 2023-2030 ($)

Table 29: Carbon Capture and Storage (CCS) Market By Capture Technology, Revenue & Volume, By Chemical Looping Combustion, 2023-2030 ($)

Table 30: Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Storage Technology, 2023-2030 ($)

Table 31: Carbon Capture and Storage (CCS) Market By Storage Technology, Revenue & Volume, By Geological Storage, 2023-2030 ($)

Table 32: Carbon Capture and Storage (CCS) Market By Storage Technology, Revenue & Volume, By Deep Ocean Storage, 2023-2030 ($)

Table 33: Carbon Capture and Storage (CCS) Market By Storage Technology, Revenue & Volume, By Enhanced Oil Recovery (EOR), 2023-2030 ($)

Table 34: Carbon Capture and Storage (CCS) Market, Revenue & Volume, By End user industry, 2023-2030 ($)

Table 35: Carbon Capture and Storage (CCS) Market By End user industry, Revenue & Volume, By Introduction, 2023-2030 ($)

Table 36: Carbon Capture and Storage (CCS) Market By End user industry, Revenue & Volume, By Biofuels, 2023-2030 ($)

Table 37: Carbon Capture and Storage (CCS) Market By End user industry, Revenue & Volume, By Food and Beverage, 2023-2030 ($)

Table 38: Carbon Capture and Storage (CCS) Market By End user industry, Revenue & Volume, By Pulp and Paper, 2023-2030 ($)

Table 39: Carbon Capture and Storage (CCS) Market By End user industry, Revenue & Volume, By Cement and Concrete, 2023-2030 ($)

Table 40: North America Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Capture Technology, 2023-2030 ($)

Table 41: North America Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Storage Technology, 2023-2030 ($)

Table 42: North America Carbon Capture and Storage (CCS) Market, Revenue & Volume, By End user industry, 2023-2030 ($)

Table 43: South america Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Capture Technology, 2023-2030 ($)

Table 44: South america Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Storage Technology, 2023-2030 ($)

Table 45: South america Carbon Capture and Storage (CCS) Market, Revenue & Volume, By End user industry, 2023-2030 ($)

Table 46: Europe Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Capture Technology, 2023-2030 ($)

Table 47: Europe Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Storage Technology, 2023-2030 ($)

Table 48: Europe Carbon Capture and Storage (CCS) Market, Revenue & Volume, By End user industry, 2023-2030 ($)

Table 49: APAC Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Capture Technology, 2023-2030 ($)

Table 50: APAC Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Storage Technology, 2023-2030 ($)

Table 51: APAC Carbon Capture and Storage (CCS) Market, Revenue & Volume, By End user industry, 2023-2030 ($)

Table 52: Middle East & Africa Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Capture Technology, 2023-2030 ($)

Table 53: Middle East & Africa Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Storage Technology, 2023-2030 ($)

Table 54: Middle East & Africa Carbon Capture and Storage (CCS) Market, Revenue & Volume, By End user industry, 2023-2030 ($)

Table 55: Russia Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Capture Technology, 2023-2030 ($)

Table 56: Russia Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Storage Technology, 2023-2030 ($)

Table 57: Russia Carbon Capture and Storage (CCS) Market, Revenue & Volume, By End user industry, 2023-2030 ($)

Table 58: Israel Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Capture Technology, 2023-2030 ($)

Table 59: Israel Carbon Capture and Storage (CCS) Market, Revenue & Volume, By Storage Technology, 2023-2030 ($)

Table 60: Israel Carbon Capture and Storage (CCS) Market, Revenue & Volume, By End user industry, 2023-2030 ($)

Table 61: Top Companies 2023 (US$)Carbon Capture and Storage (CCS) Market, Revenue & Volume

Table 62: Product Launch 2023-2024Carbon Capture and Storage (CCS) Market, Revenue & Volume

Table 63: Mergers & Acquistions 2023-2024Carbon Capture and Storage (CCS) Market, Revenue & Volume

List of Figures

Figure 1: Overview of Carbon Capture and Storage (CCS) Market 2023-2030

Figure 2: Market Share Analysis for Carbon Capture and Storage (CCS) Market 2023 (US$)

Figure 3: Product Comparison in Carbon Capture and Storage (CCS) Market 2023-2024 (US$)

Figure 4: End User Profile for Carbon Capture and Storage (CCS) Market 2023-2024 (US$)

Figure 5: Patent Application and Grant in Carbon Capture and Storage (CCS) Market 2021-2023* (US$)

Figure 6: Top 5 Companies Financial Analysis in Carbon Capture and Storage (CCS) Market 2023-2024 (US$)

Figure 7: Market Entry Strategy in Carbon Capture and Storage (CCS) Market 2023-2024

Figure 8: Ecosystem Analysis in Carbon Capture and Storage (CCS) Market 2023

Figure 9: Average Selling Price in Carbon Capture and Storage (CCS) Market 2023-2030

Figure 10: Top Opportunites in Carbon Capture and Storage (CCS) Market 2023-2024

Figure 11: Market Life Cycle Analysis in Carbon Capture and Storage (CCS) Market

Figure 12: GlobalBy Capture TechnologyCarbon Capture and Storage (CCS) Market Revenue, 2023-2030 ($)

Figure 13: GlobalBy Storage TechnologyCarbon Capture and Storage (CCS) Market Revenue, 2023-2030 ($)

Figure 14: GlobalBy End user industryCarbon Capture and Storage (CCS) Market Revenue, 2023-2030 ($)

Figure 15: Global Carbon Capture and Storage (CCS) Market - By Geography

Figure 16: Global Carbon Capture and Storage (CCS) Market Value & Volume, By Geography, 2023-2030 ($)

Figure 17: Global Carbon Capture and Storage (CCS) Market CAGR, By Geography, 2023-2030 (%)

Figure 18: North America Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 19: US Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 20: US GDP and Population, 2023-2024 ($)

Figure 21: US GDP – Composition of 2023, By Sector of Origin

Figure 22: US Export and Import Value & Volume, 2023-2024 ($)

Figure 23: Canada Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 24: Canada GDP and Population, 2023-2024 ($)

Figure 25: Canada GDP – Composition of 2023, By Sector of Origin

Figure 26: Canada Export and Import Value & Volume, 2023-2024 ($)

Figure 27: Mexico Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 28: Mexico GDP and Population, 2023-2024 ($)

Figure 29: Mexico GDP – Composition of 2023, By Sector of Origin

Figure 30: Mexico Export and Import Value & Volume, 2023-2024 ($)

Figure 31: South America Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 32: Brazil Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 33: Brazil GDP and Population, 2023-2024 ($)

Figure 34: Brazil GDP – Composition of 2023, By Sector of Origin

Figure 35: Brazil Export and Import Value & Volume, 2023-2024 ($)

Figure 36: Venezuela Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 37: Venezuela GDP and Population, 2023-2024 ($)

Figure 38: Venezuela GDP – Composition of 2023, By Sector of Origin

Figure 39: Venezuela Export and Import Value & Volume, 2023-2024 ($)

Figure 40: Argentina Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 41: Argentina GDP and Population, 2023-2024 ($)

Figure 42: Argentina GDP – Composition of 2023, By Sector of Origin

Figure 43: Argentina Export and Import Value & Volume, 2023-2024 ($)

Figure 44: Ecuador Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 45: Ecuador GDP and Population, 2023-2024 ($)

Figure 46: Ecuador GDP – Composition of 2023, By Sector of Origin

Figure 47: Ecuador Export and Import Value & Volume, 2023-2024 ($)

Figure 48: Peru Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 49: Peru GDP and Population, 2023-2024 ($)

Figure 50: Peru GDP – Composition of 2023, By Sector of Origin

Figure 51: Peru Export and Import Value & Volume, 2023-2024 ($)

Figure 52: Colombia Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 53: Colombia GDP and Population, 2023-2024 ($)

Figure 54: Colombia GDP – Composition of 2023, By Sector of Origin

Figure 55: Colombia Export and Import Value & Volume, 2023-2024 ($)

Figure 56: Costa Rica Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 57: Costa Rica GDP and Population, 2023-2024 ($)

Figure 58: Costa Rica GDP – Composition of 2023, By Sector of Origin

Figure 59: Costa Rica Export and Import Value & Volume, 2023-2024 ($)

Figure 60: Europe Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 61: U.K Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 62: U.K GDP and Population, 2023-2024 ($)

Figure 63: U.K GDP – Composition of 2023, By Sector of Origin

Figure 64: U.K Export and Import Value & Volume, 2023-2024 ($)

Figure 65: Germany Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 66: Germany GDP and Population, 2023-2024 ($)

Figure 67: Germany GDP – Composition of 2023, By Sector of Origin

Figure 68: Germany Export and Import Value & Volume, 2023-2024 ($)

Figure 69: Italy Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 70: Italy GDP and Population, 2023-2024 ($)

Figure 71: Italy GDP – Composition of 2023, By Sector of Origin

Figure 72: Italy Export and Import Value & Volume, 2023-2024 ($)

Figure 73: France Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 74: France GDP and Population, 2023-2024 ($)

Figure 75: France GDP – Composition of 2023, By Sector of Origin

Figure 76: France Export and Import Value & Volume, 2023-2024 ($)

Figure 77: Netherlands Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 78: Netherlands GDP and Population, 2023-2024 ($)

Figure 79: Netherlands GDP – Composition of 2023, By Sector of Origin

Figure 80: Netherlands Export and Import Value & Volume, 2023-2024 ($)

Figure 81: Belgium Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 82: Belgium GDP and Population, 2023-2024 ($)

Figure 83: Belgium GDP – Composition of 2023, By Sector of Origin

Figure 84: Belgium Export and Import Value & Volume, 2023-2024 ($)

Figure 85: Spain Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 86: Spain GDP and Population, 2023-2024 ($)

Figure 87: Spain GDP – Composition of 2023, By Sector of Origin

Figure 88: Spain Export and Import Value & Volume, 2023-2024 ($)

Figure 89: Denmark Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 90: Denmark GDP and Population, 2023-2024 ($)

Figure 91: Denmark GDP – Composition of 2023, By Sector of Origin

Figure 92: Denmark Export and Import Value & Volume, 2023-2024 ($)

Figure 93: APAC Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 94: China Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030

Figure 95: China GDP and Population, 2023-2024 ($)

Figure 96: China GDP – Composition of 2023, By Sector of Origin

Figure 97: China Export and Import Value & Volume, 2023-2024 ($)Carbon Capture and Storage (CCS) Market China Export and Import Value & Volume, 2023-2024 ($)

Figure 98: Australia Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 99: Australia GDP and Population, 2023-2024 ($)

Figure 100: Australia GDP – Composition of 2023, By Sector of Origin

Figure 101: Australia Export and Import Value & Volume, 2023-2024 ($)

Figure 102: South Korea Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 103: South Korea GDP and Population, 2023-2024 ($)

Figure 104: South Korea GDP – Composition of 2023, By Sector of Origin

Figure 105: South Korea Export and Import Value & Volume, 2023-2024 ($)

Figure 106: India Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 107: India GDP and Population, 2023-2024 ($)

Figure 108: India GDP – Composition of 2023, By Sector of Origin

Figure 109: India Export and Import Value & Volume, 2023-2024 ($)

Figure 110: Taiwan Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 111: Taiwan GDP and Population, 2023-2024 ($)

Figure 112: Taiwan GDP – Composition of 2023, By Sector of Origin

Figure 113: Taiwan Export and Import Value & Volume, 2023-2024 ($)

Figure 114: Malaysia Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 115: Malaysia GDP and Population, 2023-2024 ($)

Figure 116: Malaysia GDP – Composition of 2023, By Sector of Origin

Figure 117: Malaysia Export and Import Value & Volume, 2023-2024 ($)

Figure 118: Hong Kong Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 119: Hong Kong GDP and Population, 2023-2024 ($)

Figure 120: Hong Kong GDP – Composition of 2023, By Sector of Origin

Figure 121: Hong Kong Export and Import Value & Volume, 2023-2024 ($)

Figure 122: Middle East & Africa Carbon Capture and Storage (CCS) Market Middle East & Africa 3D Printing Market Value & Volume, 2023-2030 ($)

Figure 123: Russia Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 124: Russia GDP and Population, 2023-2024 ($)

Figure 125: Russia GDP – Composition of 2023, By Sector of Origin

Figure 126: Russia Export and Import Value & Volume, 2023-2024 ($)

Figure 127: Israel Carbon Capture and Storage (CCS) Market Value & Volume, 2023-2030 ($)

Figure 128: Israel GDP and Population, 2023-2024 ($)

Figure 129: Israel GDP – Composition of 2023, By Sector of Origin

Figure 130: Israel Export and Import Value & Volume, 2023-2024 ($)

Figure 131: Entropy Share, By Strategies, 2023-2024* (%)Carbon Capture and Storage (CCS) Market

Figure 132: Developments, 2023-2024*Carbon Capture and Storage (CCS) Market

Figure 133: Company 1 Carbon Capture and Storage (CCS) Market Net Revenue, By Years, 2023-2024* ($)

Figure 134: Company 1 Carbon Capture and Storage (CCS) Market Net Revenue Share, By Business segments, 2023 (%)

Figure 135: Company 1 Carbon Capture and Storage (CCS) Market Net Sales Share, By Geography, 2023 (%)

Figure 136: Company 2 Carbon Capture and Storage (CCS) Market Net Revenue, By Years, 2023-2024* ($)

Figure 137: Company 2 Carbon Capture and Storage (CCS) Market Net Revenue Share, By Business segments, 2023 (%)

Figure 138: Company 2 Carbon Capture and Storage (CCS) Market Net Sales Share, By Geography, 2023 (%)

Figure 139: Company 3 Carbon Capture and Storage (CCS) Market Net Revenue, By Years, 2023-2024* ($)

Figure 140: Company 3 Carbon Capture and Storage (CCS) Market Net Revenue Share, By Business segments, 2023 (%)

Figure 141: Company 3 Carbon Capture and Storage (CCS) Market Net Sales Share, By Geography, 2023 (%)

Figure 142: Company 4 Carbon Capture and Storage (CCS) Market Net Revenue, By Years, 2023-2024* ($)

Figure 143: Company 4 Carbon Capture and Storage (CCS) Market Net Revenue Share, By Business segments, 2023 (%)

Figure 144: Company 4 Carbon Capture and Storage (CCS) Market Net Sales Share, By Geography, 2023 (%)

Figure 145: Company 5 Carbon Capture and Storage (CCS) Market Net Revenue, By Years, 2023-2024* ($)

Figure 146: Company 5 Carbon Capture and Storage (CCS) Market Net Revenue Share, By Business segments, 2023 (%)

Figure 147: Company 5 Carbon Capture and Storage (CCS) Market Net Sales Share, By Geography, 2023 (%)

Figure 148: Company 6 Carbon Capture and Storage (CCS) Market Net Revenue, By Years, 2023-2024* ($)

Figure 149: Company 6 Carbon Capture and Storage (CCS) Market Net Revenue Share, By Business segments, 2023 (%)

Figure 150: Company 6 Carbon Capture and Storage (CCS) Market Net Sales Share, By Geography, 2023 (%)

Figure 151: Company 7 Carbon Capture and Storage (CCS) Market Net Revenue, By Years, 2023-2024* ($)

Figure 152: Company 7 Carbon Capture and Storage (CCS) Market Net Revenue Share, By Business segments, 2023 (%)

Figure 153: Company 7 Carbon Capture and Storage (CCS) Market Net Sales Share, By Geography, 2023 (%)

Figure 154: Company 8 Carbon Capture and Storage (CCS) Market Net Revenue, By Years, 2023-2024* ($)

Figure 155: Company 8 Carbon Capture and Storage (CCS) Market Net Revenue Share, By Business segments, 2023 (%)

Figure 156: Company 8 Carbon Capture and Storage (CCS) Market Net Sales Share, By Geography, 2023 (%)

Figure 157: Company 9 Carbon Capture and Storage (CCS) Market Net Revenue, By Years, 2023-2024* ($)

Figure 158: Company 9 Carbon Capture and Storage (CCS) Market Net Revenue Share, By Business segments, 2023 (%)

Figure 159: Company 9 Carbon Capture and Storage (CCS) Market Net Sales Share, By Geography, 2023 (%)

Figure 160: Company 10 Carbon Capture and Storage (CCS) Market Net Revenue, By Years, 2023-2024* ($)

Figure 161: Company 10 Carbon Capture and Storage (CCS) Market Net Revenue Share, By Business segments, 2023 (%)

Figure 162: Company 10 Carbon Capture and Storage (CCS) Market Net Sales Share, By Geography, 2023 (%)

Figure 163: Company 11 Carbon Capture and Storage (CCS) Market Net Revenue, By Years, 2023-2024* ($)

Figure 164: Company 11 Carbon Capture and Storage (CCS) Market Net Revenue Share, By Business segments, 2023 (%)

Figure 165: Company 11 Carbon Capture and Storage (CCS) Market Net Sales Share, By Geography, 2023 (%)

Figure 166: Company 12 Carbon Capture and Storage (CCS) Market Net Revenue, By Years, 2023-2024* ($)

Figure 167: Company 12 Carbon Capture and Storage (CCS) Market Net Revenue Share, By Business segments, 2023 (%)

Figure 168: Company 12 Carbon Capture and Storage (CCS) Market Net Sales Share, By Geography, 2023 (%)

Figure 169: Company 13 Carbon Capture and Storage (CCS) Market Net Revenue, By Years, 2023-2024* ($)

Figure 170: Company 13 Carbon Capture and Storage (CCS) Market Net Revenue Share, By Business segments, 2023 (%)

Figure 171: Company 13 Carbon Capture and Storage (CCS) Market Net Sales Share, By Geography, 2023 (%)

Figure 172: Company 14 Carbon Capture and Storage (CCS) Market Net Revenue, By Years, 2023-2024* ($)

Figure 173: Company 14 Carbon Capture and Storage (CCS) Market Net Revenue Share, By Business segments, 2023 (%)

Figure 174: Company 14 Carbon Capture and Storage (CCS) Market Net Sales Share, By Geography, 2023 (%)

Figure 175: Company 15 Carbon Capture and Storage (CCS) Market Net Revenue, By Years, 2023-2024* ($)

Figure 176: Company 15 Carbon Capture and Storage (CCS) Market Net Revenue Share, By Business segments, 2023 (%)

Figure 177: Company 15 Carbon Capture and Storage (CCS) Market Net Sales Share, By Geography, 2023 (%)

The Carbon Capture and Storage (CCS) Market is projected to grow at 25.1% CAGR during the forecast period 2024-2030.

The Carbon Capture and Storage (CCS) Market size is estimated to be $3.2 billion in 2023 and is projected to reach $15.3 billion by 2030

The leading players in the Carbon Capture and Storage (CCS) Market are Royal Dutch Shell PLC, Exxon Mobil Corporation, General Electric Company, Siemens AG and Others.