Email

Email Print

Print

Fuel cell Market - By Usage , By Type , By Region - Forecast(2024 - 2030)

Fuel Cells Market Overview:

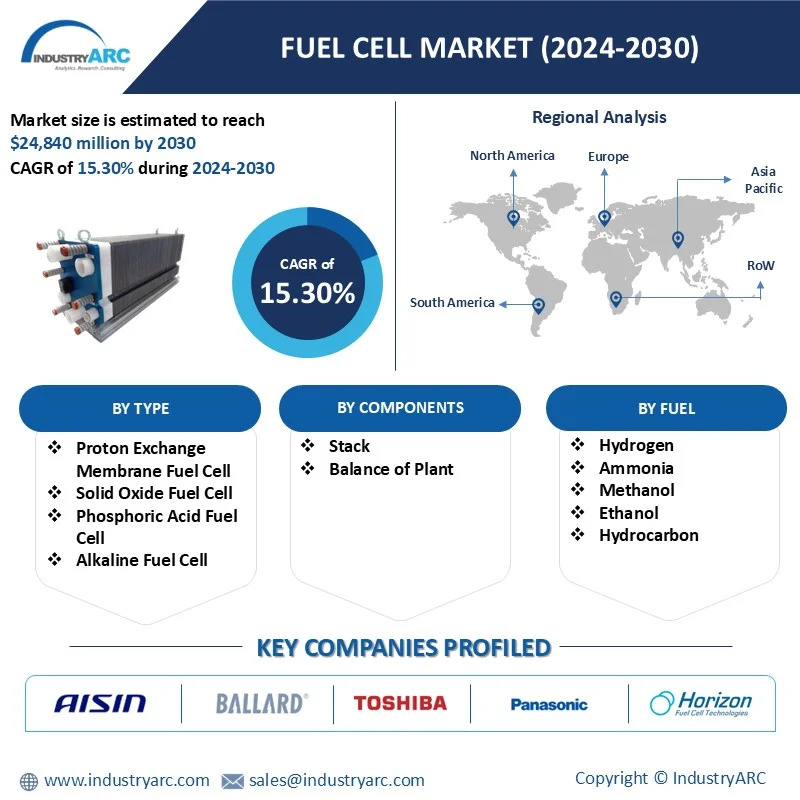

Fuel Cells Market Size is valued at $24,840 Million by 2030, and is anticipated to grow at a CAGR of 15.30% during the forecast period 2024 -2030. The global fuel cells market is experiencing rapid growth driven by the increasing demand for clean energy solutions, advancements in hydrogen infrastructure, and government policies promoting decarbonization. Fuel cells are electrochemical devices that convert chemical energy, primarily from hydrogen, into electricity with minimal environmental impact, emitting only water and heat as byproducts. Their versatility allows them to be used across various applications, including transportation, stationary power generation, and portable power solutions.

Adoption is particularly strong in the transportation sector, with fuel cell electric vehicles (FCEVs) gaining traction as a sustainable alternative to conventional internal combustion engines. Similarly, stationary fuel cells are widely used for backup power, grid support, and combined heat and power (CHP) applications. Countries worldwide are investing in hydrogen infrastructure and fuel cell technology to achieve their carbon neutrality goals.

Market Snapshot:

Fuel Cells Market - Report Coverage:

The “Fuel Cells Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Fuel Cells Market.

|

Attribute |

Segment |

|

By Type |

|

|

By Components |

|

|

By Fuel |

|

|

By Size |

|

|

By Application |

|

|

By End User |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

• The COVID-19 pandemic had a mixed impact on the growth of the fuel cells market. Initially, the market experienced disruptions due to global supply chain interruptions, delayed projects, and reduced manufacturing activities. Key components for fuel cells, such as membranes and catalysts, faced production slowdowns, impacting delivery timelines and increasing costs. However, the pandemic also highlighted the importance of sustainable and resilient energy systems, accelerating investments in green technologies, including fuel cells. Governments worldwide integrated hydrogen and fuel cell development into their economic recovery plans, with substantial funding allocated to clean energy initiatives. Furthermore, the crisis reinforced the need for decentralized and backup power solutions, increasing demand for stationary fuel cells. While the transportation sector faced setbacks due to reduced vehicle production and sales, the long-term outlook for fuel cells remains positive, driven by renewed focus on sustainability and decarbonization goals post-pandemic.

• The Russia-Ukraine war significantly influenced the growth of the fuel cells market by intensifying the global energy crisis and accelerating the shift toward energy independence and clean energy solutions. The conflict disrupted natural gas supplies, particularly in Europe, highlighting the vulnerability of reliance on fossil fuel imports. This situation spurred investments in alternative energy sources, including hydrogen and fuel cell technologies, as nations sought to diversify their energy mix and enhance energy security. Governments, especially in Europe, fast-tracked green hydrogen projects and infrastructure development, seeing fuel cells as a key component of a sustainable and resilient energy future. However, the war also caused supply chain challenges and increased raw material costs, impacting the production and affordability of fuel cells. Despite these challenges, the geopolitical tension has underscored the strategic importance of hydrogen and fuel cells, accelerating their adoption across transportation, power generation, and industrial applications.

Key Takeaways:

• Growing Demand for Proton Exchange Membrane Fuel Cell

On the basis of Type, Proton Exchange Membrane Fuel Cell held the highest segmental market share of 64% in 2023 due to their versatile applications, high efficiency, and technological advancements. PEMFCs are widely adopted in transportation, including fuel cell electric vehicles (FCEVs) like cars, buses, and trucks, owing to their compact size, quick start-up, and ability to deliver high power density. Their low operating temperature makes them suitable for portable and residential applications, while their capability to run on pure hydrogen aligns with the growing emphasis on green hydrogen production. Continuous innovations in membrane technology and cost reductions in platinum catalysts have enhanced the commercial viability of PEMFCs. Through initiatives like the Solid Oxide Fuel Cell (SOFC) program and the Fuel Cell Technologies Office (FCTO), the Department of Energy (DOE) has funded fuel cell development in the United States. Over the course of the forecast year, the solid oxide fuel cell (SOFC) is anticipated to increase at the quickest rate among all product categories. Furthermore, government policies promoting zero-emission vehicles and investments in hydrogen infrastructure have bolstered the adoption of PEMFCs, establishing them as the dominant technology in the fuel cells market.

• Stack Dominated the Fuel Cells Market

On the basis of component, stack held the highest segmental market share of around 63.3% in 2023 due to its critical role as the core component of fuel cell systems, where the electrochemical reactions occur to generate electricity. Comprising multiple interconnected cells, the stack significantly influences the overall performance, efficiency, and cost of fuel cells. Increasing investments in research and development have led to advancements in stack materials, designs, and manufacturing processes, improving durability and reducing costs. The growing adoption of fuel cells across transportation, stationary power, and portable applications has driven demand for high-performance stacks. Additionally, as governments and industries prioritize clean energy transitions and expand hydrogen infrastructure, the stack segment's centrality in driving fuel cell functionality ensures its dominance in the market.

• Hydrocarbon Leads the Fuel Cells Market

On the basis of fuel, hydrocarbon held the highest segmental market share of 91.3% in 2023 due to their widespread availability, established infrastructure, and compatibility with existing fuel cell technologies like Solid Oxide Fuel Cells (SOFCs) and Molten Carbonate Fuel Cells (MCFCs). These fuels, including natural gas, methanol, and biogas, are commonly used as primary energy sources in fuel cells due to their ability to be reformed into hydrogen on-site. This flexibility reduces the immediate dependency on pure hydrogen, which is still developing in terms of production and distribution infrastructure. Additionally, the use of hydrocarbons enables cost-effective deployment of fuel cells for stationary power generation and industrial applications. The reliability and scalability of hydrocarbon-based systems have solidified their dominance in the market while serving as a transitional solution towards a hydrogen-focused energy future.

• Large Scale Dominates the Fuel Cells Market

On the basis of size, large scale held the highest segmental market share of around 76.4% in 2023, due to its extensive use in industrial and commercial applications, such as power generation for factories, data centers, and grid backup systems. Large-scale fuel cell systems offer high efficiency, scalability, and reliability, making them ideal for meeting the growing energy demands of these sectors. Technologies like Solid Oxide Fuel Cells (SOFCs) and Molten Carbonate Fuel Cells (MCFCs) are particularly suited for large-scale installations, providing consistent power output and the ability to use multiple fuel sources, including natural gas and biogas. For instance, Kohler Energy introduced a 100kW hydrogen fuel cell power system in November 2023 that can be used for prime and standby power applications for residential and commercial applications, as well as off-highway machinery. Furthermore, increased investments in renewable energy and decarbonization efforts have driven the adoption of large-scale fuel cell projects, especially in regions focusing on sustainable energy infrastructure. These advantages position the large-scale segment as a critical driver of market growth.

• Stationery fuel cells Dominates the Fuel Cells Market

On the basis of application, stationery fuel cells held the highest segmental market share of more than 68.37% in 2023, due to their widespread use in power generation for residential, commercial, and industrial applications. These fuel cells provide reliable and efficient energy solutions, often combined with heat generation in combined heat and power (CHP) systems, making them ideal for decentralized energy systems. Technologies such as Solid Oxide Fuel Cells (SOFCs) and Molten Carbonate Fuel Cells (MCFCs) are commonly used in stationary applications due to their high efficiency and ability to operate on multiple fuels, including natural gas and biogas. The increasing focus on reducing carbon footprints and enhancing energy resilience has further driven the adoption of stationary fuel cells, particularly for backup power and grid stabilization. Governments and industries investing in renewable energy infrastructure and sustainability initiatives have solidified the dominant position of stationary fuel cells in the market.

• Transportation Dominates the Fuel Cells Market

On the basis of end-user, transportation held the highest segmental market share of 52% in 2023 due to the rapid adoption of fuel cell technologies in vehicles, such as fuel cell electric vehicles (FCEVs), buses, trucks, and trains. Fuel cells, particularly Proton Exchange Membrane Fuel Cells (PEMFCs), are well-suited for transportation due to their high-power density, quick start-up times, and zero-emission operation. Governments worldwide are promoting hydrogen-powered transportation through incentives and investments in hydrogen refueling infrastructure to meet stringent emission targets and reduce reliance on fossil fuels. For instance, Weichai Power and technology partner Ceres introduced stationary solid oxide fuel cells in China in February 2023. Over 30,000 hours of combined operation have been accomplished by the fuel cell. Additionally, the system has a 60% efficiency rate and can start and stop up to four times during the generation process. Leading automotive manufacturers, including Toyota, Hyundai, and Honda, are driving the development of FCEVs, while the demand for clean energy solutions in heavy-duty transport and maritime sectors further accelerates growth. These factors collectively position the transportation segment as a major contributor to the fuel cells market's expansion.

• Growing Demand for Fuel Cells Market Due to Growing Adoption of Fuel Cell Electric Vehicles (FCEVs)

The transportation sector is emerging as a major growth driver for the fuel cell market, with FCEVs leading the way. Governments and automotive manufacturers are increasingly focusing on hydrogen-powered vehicles to meet stringent emission standards and reduce dependency on fossil fuels. Fuel cells offer longer ranges, faster refueling times, and higher energy densities compared to battery electric vehicles (BEVs), making them ideal for heavy-duty applications such as trucks, buses, and maritime transport. Countries like Japan and South Korea are heavily investing in hydrogen refueling infrastructure to support the growth of FCEVs, while major automakers like Toyota, Hyundai, and Honda are expanding their fuel cell vehicle portfolios. This trend is expected to drive significant demand for fuel cells in the coming years. Over 15% of global greenhouse gas emissions are caused by vehicles. Governments everywhere are therefore searching for alternate energy sources to use in the transportation sector. Due to the low CO2 emissions during vehicle operation, the adoption rate of fuel cell vehicles (FCVs) is anticipated to rise during the projection period. As a result, a lot of important players are concentrating on fuel cell research and development and investment. By 2030, the EV30@30 initiative hopes to increase sales of new electric vehicles by at least 30%.

• Negative Impact on the Fuel Cells Market Due to High Production Costs and Scalability Issues

One of the primary challenges facing the fuel cell market is the high production costs associated with manufacturing fuel cells, particularly Proton Exchange Membrane Fuel Cells (PEMFCs). Fuel cells often require expensive materials, such as platinum, as catalysts, which significantly raise their production costs. While research has led to advancements in reducing the reliance on platinum, alternatives still face scalability challenges. Additionally, the manufacturing processes for fuel cells are not yet fully optimized, leading to higher costs when compared to conventional energy solutions. This issue is especially problematic in the transportation sector, where cost efficiency is a critical factor for mass adoption of fuel cell electric vehicles (FCEVs). Until these costs can be significantly reduced through advances in technology and manufacturing efficiency, widespread adoption of fuel cells, particularly in the automotive and large-scale applications, will remain limited. As a result, fuel cells still face competition from other energy solutions, such as battery-electric vehicles (BEVs) and traditional combustion engines.

Key Market Players:

Product launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Fuel Cells Market. The top 10 companies in this industry are listed below:

1. Horizon Fuel Cell Technologies

2. Panasonic Holdings Corporation

3. Toshiba Corporation

4. Ballard Power Systems Inc.

5. Aisin Seiki Co., Ltd.

6. Doosan Fuel Cell America

7. Nuvera Fuel Cells

8. SFC Group

9. Bloom Energy

10. Nedstack Fuel Cell Technology B.V.

Scope of the Report:

|

Report Metric |

Details |

|

Base Year Considered |

2023 |

|

Forecast Period |

2024-2030 |

|

CAGR |

15.30% |

|

Market Size in 2030 |

$ 1.17 billion |

|

Segments Covered |

By Type, By Component, By Fuel, By Size, By Application, By End-use, and By Region |

|

Regions Covered |

North America (USA, Canada, and Mexico), Europe (UK, Germany, France, Italy, Netherlands, Spain, Russia, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia, Indonesia, Malaysia, and Rest of APAC), South America (Brazil, Argentina, Colombia, Chile, and Rest of South America), and Rest of the World (Middle East, and Africa). |

|

Key Market Players |

|

Relevant Reports:

Hydrogen Fuel Cell Market Share, Size and Industry Growth Analysis 2020 - 2025

Report Code: AM 47068

Report Code: ESR 0027

For more Electronics related reports, please click here

1. Fuel Cell – Market Overview

2. Executive summary

3. Fuel Cell – Market Landscape

3.1. Market Share Analysis

3.2. Comparative Analysis

3.2.1. Product Benchmarking

3.2.2. End user profiling

3.2.3. Patent Analysis

3.2.4. Top 5 Financials Analysis

4. Fuel Cell – Market Forces

4.1. Market Drivers

4.2. Market Constraints

4.3. Market Challenges

4.4. Attractiveness of the Image Sensor Industry

4.4.1. Bargaining Power of Suppliers

4.4.2. Bargaining power of buyers

4.4.3. Threat of New Entrants

4.4.4. Threat of substitution

4.4.5. Rivalry among competitors

5. Fuel Cell Market – Strategic Analysis

5.1. Value Chain Analysis

5.2. Pricing Analysis

5.3. Opportunities Analysis

5.4. Product/Market Life Cycle Analysis

5.5. Supplier and Distributor Analysis

6. Fuel Cell Market - By Usage

6.1. Primary and backup power for commercial,Industial and residential buildings

6.2. Electronics

6.3. Automobiles

6.4. Power Fuel-Cell vehicles

6.5. Lifts

6.6. Boats

6.7. Submarines

6.8. Hybrid Vehicles

6.9. Small heating appliances

6.10. Food preservation

6.11. Fueling stations

7. Fuel-Cell Market - By Type

7.1. Metal hydride fuel cell

7.2. Direct formic acid fuel cell (DFAFC)

7.3. Up flow microbial fuel cell (UMFC)

7.4. Electro-galvanic fuel cell

7.5. Zinc-air battery

7.6. Microbial fuel cell

7.7. Regenerative fuel cell

7.8. Direct borohydride fuel cell

7.9. Alkaline fuel cell

7.10. Direct methanol fuel cell

7.11. Reformed methanol fuel cell

7.12. Direct-ethanol fuel cell

7.13. Proton exchange membrane fuel cell

7.14. RFC – Redox

7.15. Phosphoric acid fuel cell

7.16. Solid acid fuel cell

7.17. Molten carbonate fuel cell

7.18. Tubular solid oxide fuel cell (TSOFC)

7.19. Protonic ceramic fuel cell

7.20. Direct carbon fuel cell

7.21. Planar Solid oxide fuel cell

7.22. Enzymatic Biofuel Cells

7.23. Magnesium-Air Fuel Cell

8. Fuel Cell Market - By Geography

8.1. Americas

8.1.1. U.S.

8.1.2. Canada

8.1.3. Brazil

8.1.4. Others

8.2. Europe

8.2.1. U.K.

8.2.2. France

8.2.3. Germany

8.2.4. Others

8.3. Asia- Pacific

8.3.1. China

8.3.2. Japan

8.3.3. India

8.3.4. Australia

8.3.5. Others

8.4. ROW

9. Market Entropy

9.1. Preferred Strategy

9.2. New Product Launches

9.3. Mergers & Acquisitions

9.4. Product Developments

9.5. Ventures & Partnerships

9.6. R&D and Business Expansions

10. Company Profiles

10.1. Ballard Power Systems Inc

10.2. Horizon Fuel Cell Technologies

10.3. Fuel Cell Energy, Inc

10.4. Doosan Fuel Cell

10.5. SFC Group

*More than 10 Companies are profiled in this Research Report*

"*Financials would be provided on a best efforts basis for private companies"

11. Appendix

11.1. Abbreviations

11.2. Sources

11.3. Research Methodology

11.4. Disclaimer

List of Tables

Table 1 Fuel cell Market Overview 2023-2030

Table 2 Fuel cell Market Leader Analysis 2023-2030 (US$)

Table 3 Fuel cell MarketProduct Analysis 2023-2030 (US$)

Table 4 Fuel cell MarketEnd User Analysis 2023-2030 (US$)

Table 5 Fuel cell MarketPatent Analysis 2013-2023* (US$)

Table 6 Fuel cell MarketFinancial Analysis 2023-2030 (US$)

Table 7 Fuel cell Market Driver Analysis 2023-2030 (US$)

Table 8 Fuel cell MarketChallenges Analysis 2023-2030 (US$)

Table 9 Fuel cell MarketConstraint Analysis 2023-2030 (US$)

Table 10 Fuel cell Market Supplier Bargaining Power Analysis 2023-2030 (US$)

Table 11 Fuel cell Market Buyer Bargaining Power Analysis 2023-2030 (US$)

Table 12 Fuel cell Market Threat of Substitutes Analysis 2023-2030 (US$)

Table 13 Fuel cell Market Threat of New Entrants Analysis 2023-2030 (US$)

Table 14 Fuel cell Market Degree of Competition Analysis 2023-2030 (US$)

Table 15 Fuel cell MarketValue Chain Analysis 2023-2030 (US$)

Table 16 Fuel cell MarketPricing Analysis 2023-2030 (US$)

Table 17 Fuel cell MarketOpportunities Analysis 2023-2030 (US$)

Table 18 Fuel cell MarketProduct Life Cycle Analysis 2023-2030 (US$)

Table 19 Fuel cell MarketSupplier Analysis 2023-2030 (US$)

Table 20 Fuel cell MarketDistributor Analysis 2023-2030 (US$)

Table 21 Fuel cell Market Trend Analysis 2023-2030 (US$)

Table 22 Fuel cell Market Size 2023 (US$)

Table 23 Fuel cell Market Forecast Analysis 2023-2030 (US$)

Table 24 Fuel cell Market Sales Forecast Analysis 2023-2030 (Units)

Table 25 Fuel cell Market, Revenue & Volume,By Type, 2023-2030 ($)

Table 26 Fuel cell MarketBy Type, Revenue & Volume,By Metal hydride fuel cell, 2023-2030 ($)

Table 27 Fuel cell MarketBy Type, Revenue & Volume,By Direct formic acid fuel cell (DFAFC), 2023-2030 ($)

Table 28 Fuel cell MarketBy Type, Revenue & Volume,By Up flow microbial fuel cell (UMFC), 2023-2030 ($)

Table 29 Fuel cell MarketBy Type, Revenue & Volume,By Electro-galvanic fuel cell, 2023-2030 ($)

Table 30 Fuel cell MarketBy Type, Revenue & Volume,By Zinc-air battery, 2023-2030 ($)

Table 31 Fuel cell Market, Revenue & Volume,By Usage, 2023-2030 ($)

Table 32 Fuel cell MarketBy Usage, Revenue & Volume,By Electronics, 2023-2030 ($)

Table 33 Fuel cell MarketBy Usage, Revenue & Volume,By Automobiles, 2023-2030 ($)

Table 34 Fuel cell MarketBy Usage, Revenue & Volume,By Lifts, 2023-2030 ($)

Table 35 Fuel cell MarketBy Usage, Revenue & Volume,By Boats, 2023-2030 ($)

Table 36 Fuel cell MarketBy Usage, Revenue & Volume,By Food preservation, 2023-2030 ($)

Table 37 North America Fuel cell Market, Revenue & Volume,By Type, 2023-2030 ($)

Table 38 North America Fuel cell Market, Revenue & Volume,By Usage, 2023-2030 ($)

Table 39 South america Fuel cell Market, Revenue & Volume,By Type, 2023-2030 ($)

Table 40 South america Fuel cell Market, Revenue & Volume,By Usage, 2023-2030 ($)

Table 41 Europe Fuel cell Market, Revenue & Volume,By Type, 2023-2030 ($)

Table 42 Europe Fuel cell Market, Revenue & Volume,By Usage, 2023-2030 ($)

Table 43 APAC Fuel cell Market, Revenue & Volume,By Type, 2023-2030 ($)

Table 44 APAC Fuel cell Market, Revenue & Volume,By Usage, 2023-2030 ($)

Table 45 Middle East & Africa Fuel cell Market, Revenue & Volume,By Type, 2023-2030 ($)

Table 46 Middle East & Africa Fuel cell Market, Revenue & Volume,By Usage, 2023-2030 ($)

Table 47 Russia Fuel cell Market, Revenue & Volume,By Type, 2023-2030 ($)

Table 48 Russia Fuel cell Market, Revenue & Volume,By Usage, 2023-2030 ($)

Table 49 Israel Fuel cell Market, Revenue & Volume,By Type, 2023-2030 ($)

Table 50 Israel Fuel cell Market, Revenue & Volume,By Usage, 2023-2030 ($)

Table 51 Top Companies 2023 (US$)Fuel cell Market, Revenue & Volume,,

Table 52 Product Launch 2023-2030Fuel cell Market, Revenue & Volume,,

Table 53 Mergers & Acquistions 2023-2030Fuel cell Market, Revenue & Volume,,

List of Figures

Figure 1 Overview of Fuel cell Market 2023-2030

Figure 2 Market Share Analysis for Fuel cell Market 2023 (US$)

Figure 3 Product Comparison in Fuel cell Market 2023-2030 (US$)

Figure 4 End User Profile for Fuel cell Market 2023-2030 (US$)

Figure 5 Patent Application and Grant in Fuel cell Market 2013-2023* (US$)

Figure 6 Top 5 Companies Financial Analysis in Fuel cell Market 2023-2030 (US$)

Figure 7 Market Entry Strategy in Fuel cell Market 2023-2030

Figure 8 Ecosystem Analysis in Fuel cell Market2023

Figure 9 Average Selling Price in Fuel cell Market 2023-2030

Figure 10 Top Opportunites in Fuel cell Market 2023-2030

Figure 11 Market Life Cycle Analysis in Fuel cell Market

Figure 12 GlobalBy TypeFuel cell Market Revenue, 2023-2030 ($)

Figure 13 GlobalBy UsageFuel cell Market Revenue, 2023-2030 ($)

Figure 14 Global Fuel cell Market - By Geography

Figure 15 Global Fuel cell Market Value & Volume, By Geography, 2023-2030 ($)

Figure 16 Global Fuel cell Market CAGR, By Geography, 2023-2030 (%)

Figure 17 North America Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 18 US Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 19 US GDP and Population, 2023-2030 ($)

Figure 20 US GDP – Composition of 2023, By Sector of Origin

Figure 21 US Export and Import Value & Volume, 2023-2030 ($)

Figure 22 Canada Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 23 Canada GDP and Population, 2023-2030 ($)

Figure 24 Canada GDP – Composition of 2023, By Sector of Origin

Figure 25 Canada Export and Import Value & Volume, 2023-2030 ($)

Figure 26 Mexico Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 27 Mexico GDP and Population, 2023-2030 ($)

Figure 28 Mexico GDP – Composition of 2023, By Sector of Origin

Figure 29 Mexico Export and Import Value & Volume, 2023-2030 ($)

Figure 30 South America Fuel cell MarketSouth America 3D Printing Market Value & Volume, 2023-2030 ($)

Figure 31 Brazil Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 32 Brazil GDP and Population, 2023-2030 ($)

Figure 33 Brazil GDP – Composition of 2023, By Sector of Origin

Figure 34 Brazil Export and Import Value & Volume, 2023-2030 ($)

Figure 35 Venezuela Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 36 Venezuela GDP and Population, 2023-2030 ($)

Figure 37 Venezuela GDP – Composition of 2023, By Sector of Origin

Figure 38 Venezuela Export and Import Value & Volume, 2023-2030 ($)

Figure 39 Argentina Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 40 Argentina GDP and Population, 2023-2030 ($)

Figure 41 Argentina GDP – Composition of 2023, By Sector of Origin

Figure 42 Argentina Export and Import Value & Volume, 2023-2030 ($)

Figure 43 Ecuador Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 44 Ecuador GDP and Population, 2023-2030 ($)

Figure 45 Ecuador GDP – Composition of 2023, By Sector of Origin

Figure 46 Ecuador Export and Import Value & Volume, 2023-2030 ($)

Figure 47 Peru Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 48 Peru GDP and Population, 2023-2030 ($)

Figure 49 Peru GDP – Composition of 2023, By Sector of Origin

Figure 50 Peru Export and Import Value & Volume, 2023-2030 ($)

Figure 51 Colombia Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 52 Colombia GDP and Population, 2023-2030 ($)

Figure 53 Colombia GDP – Composition of 2023, By Sector of Origin

Figure 54 Colombia Export and Import Value & Volume, 2023-2030 ($)

Figure 55 Costa Rica Fuel cell MarketCosta Rica 3D Printing Market Value & Volume, 2023-2030 ($)

Figure 56 Costa Rica GDP and Population, 2023-2030 ($)

Figure 57 Costa Rica GDP – Composition of 2023, By Sector of Origin

Figure 58 Costa Rica Export and Import Value & Volume, 2023-2030 ($)

Figure 59 Europe Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 60 U.K Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 61 U.K GDP and Population, 2023-2030 ($)

Figure 62 U.K GDP – Composition of 2023, By Sector of Origin

Figure 63 U.K Export and Import Value & Volume, 2023-2030 ($)

Figure 64 Germany Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 65 Germany GDP and Population, 2023-2030 ($)

Figure 66 Germany GDP – Composition of 2023, By Sector of Origin

Figure 67 Germany Export and Import Value & Volume, 2023-2030 ($)

Figure 68 Italy Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 69 Italy GDP and Population, 2023-2030 ($)

Figure 70 Italy GDP – Composition of 2023, By Sector of Origin

Figure 71 Italy Export and Import Value & Volume, 2023-2030 ($)

Figure 72 France Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 73 France GDP and Population, 2023-2030 ($)

Figure 74 France GDP – Composition of 2023, By Sector of Origin

Figure 75 France Export and Import Value & Volume, 2023-2030 ($)

Figure 76 Netherlands Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 77 Netherlands GDP and Population, 2023-2030 ($)

Figure 78 Netherlands GDP – Composition of 2023, By Sector of Origin

Figure 79 Netherlands Export and Import Value & Volume, 2023-2030 ($)

Figure 80 Belgium Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 81 Belgium GDP and Population, 2023-2030 ($)

Figure 82 Belgium GDP – Composition of 2023, By Sector of Origin

Figure 83 Belgium Export and Import Value & Volume, 2023-2030 ($)

Figure 84 Spain Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 85 Spain GDP and Population, 2023-2030 ($)

Figure 86 Spain GDP – Composition of 2023, By Sector of Origin

Figure 87 Spain Export and Import Value & Volume, 2023-2030 ($)

Figure 88 Denmark Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 89 Denmark GDP and Population, 2023-2030 ($)

Figure 90 Denmark GDP – Composition of 2023, By Sector of Origin

Figure 91 Denmark Export and Import Value & Volume, 2023-2030 ($)

Figure 92 APAC Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 93 China Fuel cell MarketValue & Volume, 2023-2030

Figure 94 China GDP and Population, 2023-2030 ($)

Figure 95 China GDP – Composition of 2023, By Sector of Origin

Figure 96 China Export and Import Value & Volume, 2023-2030 ($)Fuel cell MarketChina Export and Import Value & Volume, 2023-2030 ($)

Figure 97 Australia Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 98 Australia GDP and Population, 2023-2030 ($)

Figure 99 Australia GDP – Composition of 2023, By Sector of Origin

Figure 100 Australia Export and Import Value & Volume, 2023-2030 ($)

Figure 101 South Korea Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 102 South Korea GDP and Population, 2023-2030 ($)

Figure 103 South Korea GDP – Composition of 2023, By Sector of Origin

Figure 104 South Korea Export and Import Value & Volume, 2023-2030 ($)

Figure 105 India Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 106 India GDP and Population, 2023-2030 ($)

Figure 107 India GDP – Composition of 2023, By Sector of Origin

Figure 108 India Export and Import Value & Volume, 2023-2030 ($)

Figure 109 Taiwan Fuel cell MarketTaiwan 3D Printing Market Value & Volume, 2023-2030 ($)

Figure 110 Taiwan GDP and Population, 2023-2030 ($)

Figure 111 Taiwan GDP – Composition of 2023, By Sector of Origin

Figure 112 Taiwan Export and Import Value & Volume, 2023-2030 ($)

Figure 113 Malaysia Fuel cell MarketMalaysia 3D Printing Market Value & Volume, 2023-2030 ($)

Figure 114 Malaysia GDP and Population, 2023-2030 ($)

Figure 115 Malaysia GDP – Composition of 2023, By Sector of Origin

Figure 116 Malaysia Export and Import Value & Volume, 2023-2030 ($)

Figure 117 Hong Kong Fuel cell MarketHong Kong 3D Printing Market Value & Volume, 2023-2030 ($)

Figure 118 Hong Kong GDP and Population, 2023-2030 ($)

Figure 119 Hong Kong GDP – Composition of 2023, By Sector of Origin

Figure 120 Hong Kong Export and Import Value & Volume, 2023-2030 ($)

Figure 121 Middle East & Africa Fuel cell MarketMiddle East & Africa 3D Printing Market Value & Volume, 2023-2030 ($)

Figure 122 Russia Fuel cell MarketRussia 3D Printing Market Value & Volume, 2023-2030 ($)

Figure 123 Russia GDP and Population, 2023-2030 ($)

Figure 124 Russia GDP – Composition of 2023, By Sector of Origin

Figure 125 Russia Export and Import Value & Volume, 2023-2030 ($)

Figure 126 Israel Fuel cell Market Value & Volume, 2023-2030 ($)

Figure 127 Israel GDP and Population, 2023-2030 ($)

Figure 128 Israel GDP – Composition of 2023, By Sector of Origin

Figure 129 Israel Export and Import Value & Volume, 2023-2030 ($)

Figure 130 Entropy Share, By Strategies, 2023-2030* (%)Fuel cell Market

Figure 131 Developments, 2023-2030*Fuel cell Market

Figure 132 Company 1 Fuel cell Market Net Revenue, By Years, 2023-2030* ($)

Figure 133 Company 1 Fuel cell Market Net Revenue Share, By Business segments, 2023 (%)

Figure 134 Company 1 Fuel cell Market Net Sales Share, By Geography, 2023 (%)

Figure 135 Company 2 Fuel cell Market Net Revenue, By Years, 2023-2030* ($)

Figure 136 Company 2 Fuel cell Market Net Revenue Share, By Business segments, 2023 (%)

Figure 137 Company 2 Fuel cell Market Net Sales Share, By Geography, 2023 (%)

Figure 138 Company 3Fuel cell Market Net Revenue, By Years, 2023-2030* ($)

Figure 139 Company 3Fuel cell Market Net Revenue Share, By Business segments, 2023 (%)

Figure 140 Company 3Fuel cell Market Net Sales Share, By Geography, 2023 (%)

Figure 141 Company 4 Fuel cell Market Net Revenue, By Years, 2023-2030* ($)

Figure 142 Company 4 Fuel cell Market Net Revenue Share, By Business segments, 2023 (%)

Figure 143 Company 4 Fuel cell Market Net Sales Share, By Geography, 2023 (%)

Figure 144 Company 5 Fuel cell Market Net Revenue, By Years, 2023-2030* ($)

Figure 145 Company 5 Fuel cell Market Net Revenue Share, By Business segments, 2023 (%)

Figure 146 Company 5 Fuel cell Market Net Sales Share, By Geography, 2023 (%)

Figure 147 Company 6 Fuel cell Market Net Revenue, By Years, 2023-2030* ($)

Figure 148 Company 6 Fuel cell Market Net Revenue Share, By Business segments, 2023 (%)

Figure 149 Company 6 Fuel cell Market Net Sales Share, By Geography, 2023 (%)

Figure 150 Company 7 Fuel cell Market Net Revenue, By Years, 2023-2030* ($)

Figure 151 Company 7 Fuel cell Market Net Revenue Share, By Business segments, 2023 (%)

Figure 152 Company 7 Fuel cell Market Net Sales Share, By Geography, 2023 (%)

Figure 153 Company 8 Fuel cell Market Net Revenue, By Years, 2023-2030* ($)

Figure 154 Company 8 Fuel cell Market Net Revenue Share, By Business segments, 2023 (%)

Figure 155 Company 8 Fuel cell Market Net Sales Share, By Geography, 2023 (%)

Figure 156 Company 9 Fuel cell Market Net Revenue, By Years, 2023-2030* ($)

Figure 157 Company 9 Fuel cell Market Net Revenue Share, By Business segments, 2023 (%)

Figure 158 Company 9 Fuel cell Market Net Sales Share, By Geography, 2023 (%)

Figure 159 Company 10 Fuel cell Market Net Revenue, By Years, 2023-2030* ($)

Figure 160 Company 10 Fuel cell Market Net Revenue Share, By Business segments, 2023 (%)

Figure 161 Company 10 Fuel cell Market Net Sales Share, By Geography, 2023 (%)

Figure 162 Company 11 Fuel cell Market Net Revenue, By Years, 2023-2030* ($)

Figure 163 Company 11 Fuel cell Market Net Revenue Share, By Business segments, 2023 (%)

Figure 164 Company 11 Fuel cell Market Net Sales Share, By Geography, 2023 (%)

Figure 165 Company 12 Fuel cell Market Net Revenue, By Years, 2023-2030* ($)

Figure 166 Company 12 Fuel cell Market Net Revenue Share, By Business segments, 2023 (%)

Figure 167 Company 12 Fuel cell Market Net Sales Share, By Geography, 2023 (%)

Figure 168 Company 13Fuel cell Market Net Revenue, By Years, 2023-2030* ($)

Figure 169 Company 13Fuel cell Market Net Revenue Share, By Business segments, 2023 (%)

Figure 170 Company 13Fuel cell Market Net Sales Share, By Geography, 2023 (%)

Figure 171 Company 14 Fuel cell Market Net Revenue, By Years, 2023-2030* ($)

Figure 172 Company 14 Fuel cell Market Net Revenue Share, By Business segments, 2023 (%)

Figure 173 Company 14 Fuel cell Market Net Sales Share, By Geography, 2023 (%)

Figure 174 Company 15 Fuel cell Market Net Revenue, By Years, 2023-2030* ($)

Figure 175 Company 15 Fuel cell Market Net Revenue Share, By Business segments, 2023 (%)

Figure 176 Company 15 Fuel cell Market Net Sales Share, By Geography, 2023 (%)