Email

Email Print

Print

Electrosurgical Devices Market - Product Type ; Application; End User ; Global Industry Analysis, Size, Share, Growth, Trends, and Forecast 2024 - 2030

Electrosurgical Devices Market Overview:

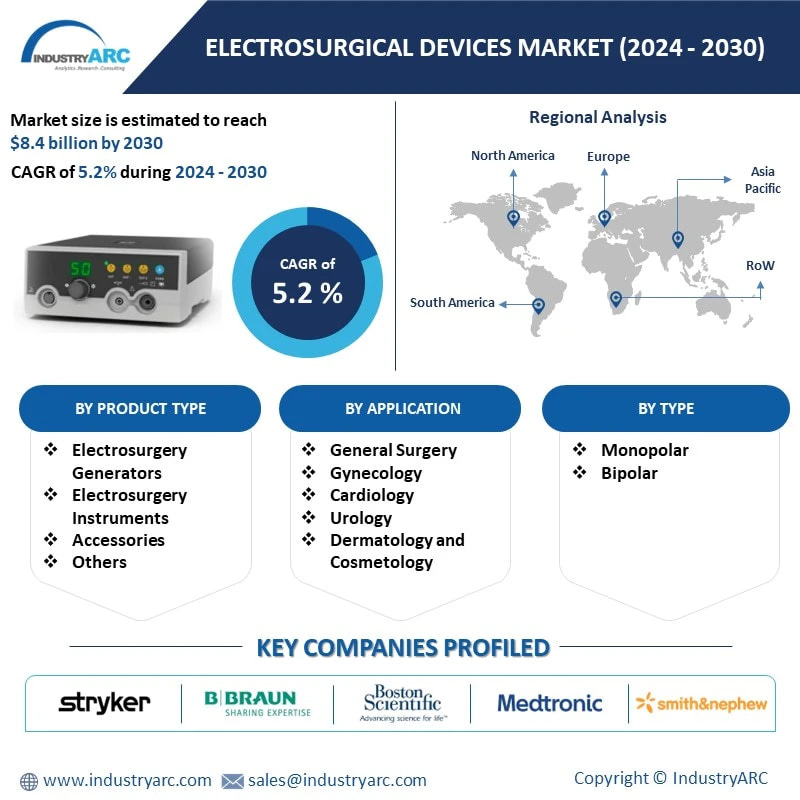

Electrosurgical Devices Market size is estimated to reach $8.4 billion by 2030, growing at a CAGR of 5.2% during the forecast period 2024-2030. Electrosurgical devices are used in a variety of surgical procedures to cut, coagulate, desiccate, and fulgurate tissues. They work by applying high-frequency electrical current to the tissue, which causes the tissue to heat up and denature. This can be used to cut through tissue, seal blood vessels, and destroy tumors. The rising prevalence of chronic diseases, growing number of surgical procedures, and the increasing investment in advanced healthcare facilities in developing countries are set to drive the growth of the global Electrosurgical Devices Market during the forecast period 2024-2030.

One of the major trends in the market is the integration of artificial intelligence (AI) and robotics. The use of robotics surgery allows for improved control, precision, and safety resulting in better outcomes even in complex procedures. Another trend in the market is the increasing preference for Minimally Invasive Surgery (MIS) procedures. The Australian Institute of Health and Welfare estimates that approximately 100,000 gynecological laparoscopic procedures are performed annually in Australia and are attributed to decreased morbidity and faster recovery. MIS procedures are gaining popularity due to faster recovery times and less pain. This, in turn, is driving demand for specialized electrosurgical devices that are smaller, more precise, and offer superior visualization for surgeons.

Market Snapshot:

Electrosurgical Devices Market- Report Coverage:

The “Electrosurgical Devices Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Electrosurgical Device Market.

| Attribute | Segment |

|---|---|

|

By Product Type |

|

|

By Type |

|

|

By Application |

|

|

By End-Use Industry |

|

|

By Geography |

|

COVID-19/ Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic led to increased attention being paid to safety during surgical procedures to minimize potential infections. As a result, innovative single-use technologies for complex surgical procedures became more widely used. This trend has been most apparent in the number of major medical device companies rapidly adopting the single-use model during the pandemic. In September 2020, Boston Scientific revealed its commitment to growing the sterile, single-use medical device market through single-use scopes.

- The conflict between Russia and Ukraine will result in long-term supply chain disruptions that could affect the electrosurgical device market, either through delays of shipments from closed airspace and expensive fuel or cyberattacks on healthcare systems. In times of war, countries usually prioritize defense spending over healthcare spending which might also affect the market.

Key Takeaways:

-

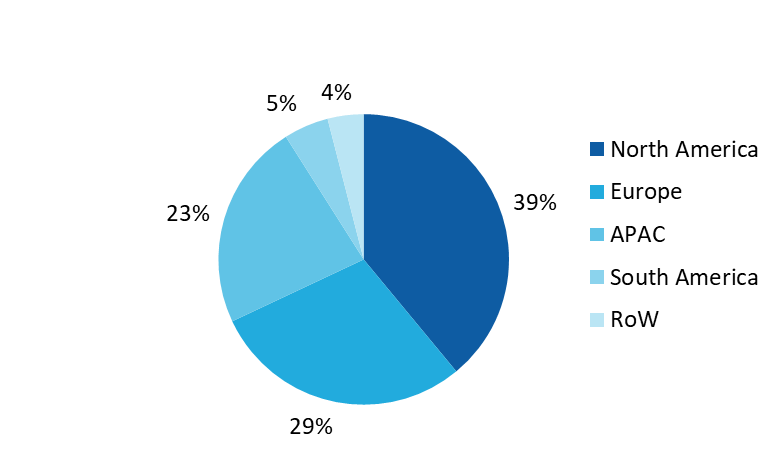

Dominance of North America

Geographically, North America held the largest share with 39% of the overall market in 2023. North America boasts of well-developed hospitals and surgical centers equipped with sophisticated surgical suites and staffed by highly skilled surgeons who actively utilize advanced electrosurgical technology. North America has a well-established regulatory framework for medical devices, ensuring a certain level of quality and safety for electrosurgical devices. In April 2022, J&J launched an electrosurgical generator for use in a wide range of open and laparoscopic operations. It is a microprocessor-controlled, isolated output, high-frequency generator that can perform monopolar cutting and coagulation as well as bipolar coagulation through an auxiliary electrode.

-

Electrosurgical Instruments holds the largest market share

Based on type, the Electrosurgical Instruments held the largest market share owing to the availability of a wide range of electrosurgical instruments, each designed for specific applications. This variety caters to the diverse needs of different surgeries, ensuring there's an instrument suited for each task. This breadth of options contributes to the overall market share of instruments. In electrosurgery, devices include electrosurgical units, bipolar and monopolar forceps, electrodes, diathermy instruments and other machines. They utilize high-frequency energy to create thermal effects for cutting and coagulating tissue.

-

By Application, General Surgery is the largest market

General surgery encompasses a vast array of procedures, from minimally invasive laparoscopic surgeries to open abdominal procedures. This versatility necessitates a diverse set of electrosurgical instruments for cutting, grasping, dissecting, and coagulating tissues. The increasing prevalence of chronic diseases like obesity, gastrointestinal disorders, and colorectal cancer necessitates more general surgical procedures, driving the demand for electrosurgical devices. According to the American Society for Metabolic and Bariatric Surgery (ASMBS), the total bariatric procedures in 2022 reached 279,967 an increase of 6.5% from 262,893 procedures performed in 2021. Such factors make general surgery a significant application area for electrosurgical devices, leading to its large share in the market.

-

Rise in the Chronic Diseases Drives the Market

Chronic diseases are a major health concern worldwide, and their prevalence is steadily rising. Environmental factors like air and water pollution, along with climate change, also contribute to the rise of chronic diseases. Socioeconomic factors such as poverty and stress can further elevate the risk. As per the WHO, the increasing toll of non-communicable diseases meant that if the trend were to continue, by 2050, chronic diseases such as cardiovascular diseases, cancer, diabetes and respiratory illnesses, will account for 86% of the 90 million deaths each year. Rise in these diseases often necessitate surgical intervention. Electrosurgical devices offer a minimally invasive and precise way to perform these procedures, leading to higher demand for these tools.

-

Increasing Investment in Advanced Healthcare Facilities

The healthcare industry is witnessing a surge in investment in advanced medical facilities. For instant, as per the 2024 India Private Equity Report, healthcare investments in India hit a record high of $5.5 billion in 2023, driven by a threefold increase compared to 2022. Manipal Hospitals, one of India’s largest multi-specialty hospitals, invested approximately $370 million in the Columbia Asia acquisition and $45 million to acquire Vikram Hospital, during FY21-23. Modern hospitals and surgical centers are increasingly equipping themselves with sophisticated electrosurgical units. These advanced devices offer surgeons greater precision, improved cutting and coagulation capabilities, and enhanced safety features. Additionally, the integration of robotics and computer-aided surgery with electrosurgical tools is creating a new wave of minimally invasive procedures. This focus on advanced technology ensures faster patient recovery times, reduced hospital stays, and improved overall surgical outcomes.

-

Risks Associated with Electrosurgery to Hamper the Market

While electrosurgery offers several benefits, inherent risks associated with the electrosurgery can act as a restraint. The primary concern lies in the generation of heat during procedures. This heat can lead to thermal injuries like burns on surrounding tissues. Additionally, electrosurgical smoke produced during tissue manipulation poses health risks to both patients and medical personnel. The smoke can contain harmful gases, cellular debris, and even viruses. Furthermore, the potential for electrical shocks and inadvertent ignition of flammable materials during surgery are additional safety considerations. Such risks might hamper the growth of electrosurgical devices market.

Electrosurgical Devices Market: Market Share (%) by Region, 2023

Electrosurgical Devices Market: Market Share (%) by Region, 2023

For more details on this report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Propionic Acid Market. The top 10 companies in the Electrosurgical Devices Market are:

- Stryker. Corporation

- B. Brawn Melsungen AG.

- Boston Scientific Corporation

- Medtronic Plc

- Smith & Nephew

- Erbe Elektromedizin GmbH

- Johnson & Johnson

- Angio Dynamics Inc.

- Olympus Corporation

- CONMED Corporation

Scope of Report:

| Report Metric | Details |

|---|---|

|

Market size available for years |

2024–2030 |

|

Base year considered |

2023 |

|

Forecast period |

2024–2030 |

|

Forecast units |

Value (USD) |

|

Segments covered |

Product Type, Type, Application, End-Use Industry and Region |

|

Geographies covered |

North America (US, Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Netherlands, Belgium and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Indonesia, Thailand, Malaysia and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America) & Rest of the World (Middle East and Africa) |

|

Companies covered |

Key 10 players covered include Stryker. Corporation, B. Brawn Melsungen AG., Boston Scientific Corporation, Medtronic Plc, Smith & Nephew, Erbe Elektromedizin GmbH, Johnson & Johnson, Angio Dynamics Inc., Olympus Corporation, CONMED Corporation |

For more Lifesciences and Healthcare Market reports, please click here

1. Electrosurgical Devices Market- Market Overview

1.1 Definitions and Scope

2. Electrosurgical Devices Market - Executive Summary

2.1 Key Trends by Product Type

2.2 Key Trends by Type

2.3 Key Trends by Application

2.4 Key Trends by End Use Industry

2.5 Key Trends by Geography

3. Electrosurgical Devices Market – Comparative analysis

3.1 Market Share Analysis- Major Companies

3.2 Product Benchmarking- Major Companies

3.3 Top 5 Financials Analysis

3.4 Patent Analysis- Major Companies

3.5 Pricing Analysis (ASPs will be provided)

4. Electrosurgical Devices Market - Startup companies Scenario Premium

4.1 Major startup company analysis:

4.1.1 Investment

4.1.2 Revenue

4.1.3 Product portfolio

4.1.4 Venture Capital and Funding Scenario

5. Electrosurgical Devices Market – Industry Market Entry Scenario Premium

5.1 Regulatory Framework Overview

5.2 New Business and Ease of Doing Business Index

5.3 Successful Venture Profiles

5.4 Customer Analysis – Major companies

6. Electrosurgical Devices Market - Market Forces

6.1 Market Drivers

6.2 Market Constraints

6.3 Porters Five Force Model

6.3.1 Bargaining Power of Suppliers

6.3.2 Bargaining Powers of Buyers

6.3.3 Threat of New Entrants

6.3.4 Competitive Rivalry

6.3.5 Threat of Substitutes

7. Electrosurgical Devices Market – Strategic Analysis

7.1 Value/Supply Chain Analysis

7.2 Opportunity Analysis

7.3 Product/Market Life Cycle

7.4 Distributor Analysis – Major Companies

8. Electrosurgical Devices Market – By Type (Market Size –$Million/$Billion)

8.1 Electrosurgery Generators

8.2 Electrosurgery Instruments

8.2.1 Electrosurgical Pencils/Handpieces

8.2.2 Electrosurgical Electrodes

8.2.2.1 Needles

8.2.2.2 Loops

8.2.2.3 Balls

8.2.2.4 Blades

8.2.2.5 Others

8.2.3 Forceps

8.2.4 Suction Coagulators

8.2.5 Others

8.3 Smoke Management Systems

8.3.1 Argon Beam Coagulators

8.3.2 Smoke Evacuators

8.3.3 Others

8.4 Accessories

8.5 Others

9. Electrosurgical Devices Market – By Type (Market Size –$Million/$Billion)

9.1 Monopolar

9.2 Bipolar

10. Electrosurgical Devices Market – By Application (Market Size –$Million/$Billion)

10.1 General Surgery

10.2 Gynecology

10.3 Cardiology

10.4 Urology

10.5 Dermatology and Cosmetology

10.6 Orthopedics

10.7 Neurology

10.8 Oncology

10.9 Dentistry

10.10 Gastrointestinal Surgery

10.11 Others

11. Electrosurgical Devices Market – By End Use Industry (Market Size –$Million/$Billion)

11.1 Hospitals

11.2 Ambulatory Surgery Centers

11.3 Specialized Clinics

12. Electrosurgical Devices Market - By Geography (Market Size -$Million/Billion)

12.1 North America

12.1.1 USA

12.1.2 Canada

12.1.3 Mexico

12.2 Europe

12.2.1 UK

12.2.2 Germany

12.2.3 France

12.2.4 Italy

12.2.5 Netherlands

12.2.6 Spain

12.2.7 Belgium

12.2.8 Rest of Europe

12.3 Asia-Pacific

12.3.1 China

12.3.2 Japan

12.3.3 India

12.3.4 South Korea

12.3.5 Australia

12.3.6 Indonesia

12.3.7 Thailand

12.3.8 Malaysia

12.3.9 Rest of APAC

12.4 South America

12.4.1 Brazil

12.4.2 Argentina

12.4.3 Colombia

12.4.4 Chile

12.4.5 Rest of South America

12.5 Rest of the World

12.5.1 Middle East

12.5.2 Africa

13. Electrosurgical Devices Market – Entropy

13.1 New Product Launches

13.2 M&As, Collaborations, JVs and Partnerships

14. Electrosurgical Devices Market – Industry/Segment Competition Analysis

14.1 Company Benchmarking Matrix – Major Companies

14.2 Market Share at Global Level - Major companies

14.3 Market Share by Key Region - Major companies

14.4 Market Share by Key Country - Major companies

14.5 Market Share by Key Application - Major companies

14.6 Market Share by Key Product Type/Product category - Major companies

15. Electrosurgical Devices Market – Key Company List by Country Premium

16. Electrosurgical Devices Market Company Analysis - Business Overview, Product Portfolio, Financials, and Developments

16.1 Stryker Corporation

16.2 B. Brawn Melsungen AG.

16.3 Boston Scientific Corporation

16.4 Medtronic Plc

16.5 Smith & Nephew

16.6 Erbe Elektromedizin GmbH

16.7 Johnson & Johnson

16.8 Angio Dynamics Inc.

16.9 Olympus Corporation

16.10 CONMED Corporation

"*Financials would be provided on a best-effort basis for private companies*”

Connect with our experts to get customized reports that best suit your requirements. Our

reports include global-level data, niche markets and competitive landscape.

The Electrosurgical Market is forecast to grow at 5.2% during the forecast period 2024-2030

Global Electrosurgical Devices Market size is estimated to be US$5.9 billion in 2023 and is projected to reach US$8.4 Billion by 2030

Stryker. Corporation, B. Brawn Melsungen AG., Boston Scientific Corporation, Medtronic Plc, Smith & Nephew and others.

Integration of artificial intelligence (AI) and robotics and the increasing preference for MIS procedures are some of the major trends in the market.

The rising prevalence of chronic diseases, growing number of surgical procedures, and the increasing investment in advanced healthcare facilities in developing countries are the driving factors of the market. Integration of robotics & AI and PFA are opportunities for the market