Email

Email Print

Print

Canada Plastics Market – By Polymer Type , By Process, By Type , By End-Use Industry Opportunity Analysis & Industry Forecast, 2024-2030

Canada Plastics Market Overview:

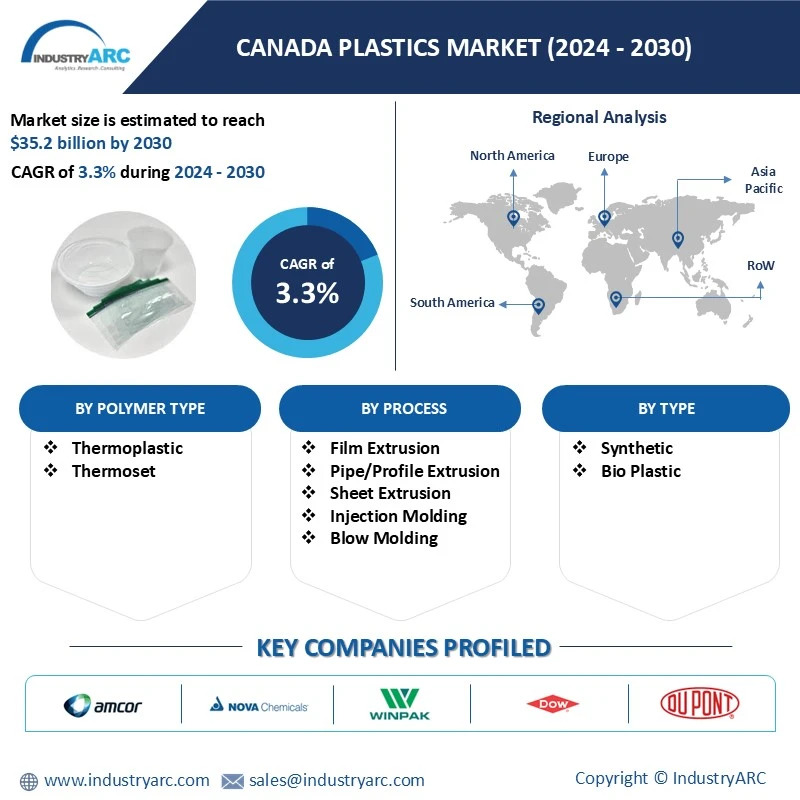

Canada Plastics Market size is estimated to reach US$35.2 Billion by 2030, growing at a CAGR of 3.3% during the forecast period 2024-2030. The rise in usage of plastics and demand of plastics from several industries have led to rapid growth in the plastics market in Canada. Increasing use of plastics in the packaging of food, beverages and personal care products are propelling the growth of plastics market in Canada. Additionally, the rising demand for bio degradable and high-performance plastics are also fueling the growth of the Canada Plastics industry. A major trend in the market is the growing demand for recycled plastic materials. Bottles made with 100% recycled plastic create and sustain a circular economy for plastic packaging. Once the material (PET) is recycled, it is cleaned, sorted and ground into small flakes that become raw material for more new bottles. For instance, the Coca-Cola Company announced that all 500-mL sparkling beverage bottles sold in Canada would transition to being made from 100% recycled plastic (excluding caps and labels) by early 2024. The goal is to boost the availability of high-quality, food-grade recycled plastic in Canada and expand the use of sustainable packaging across more Coca-Cola brands. Additionally, the trend of incorporating more plastics and chemistry products into vehicles is propelling the market growth. For instance, according to U.S. Department of Energy, replacing heavy steel components with materials such as aluminum, or glass fiber-reinforced polymer composites can decrease component weight by 10-60%. Plastics and the products of chemistry in vehicles do more than just improve fuel efficiency and range, they also support vehicle safety. In addition to seatbelts and airbags, which depend on plastics and chemistry, fiber-reinforced polymer composites can absorb four times the crush energy of steel while foams and polymer composites also help provide impact protection. Such trends are propelling the growth of Canada Plastics market.

Market Snapshot :

Canada Plastics Market - Report Coverage:

The “Canada Plastics Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Canada Plastics Market.

| Attribute | Segment |

|---|---|

|

By Polymer Type |

|

|

By Process |

|

|

By Type |

|

|

By End-Use Industry |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic had a mixed impact on Canada’s plastics market. Disposable medical devices and components like syringes, vials and diagnostic kits increased in production. Manufacturing processes and raw material supply chains faced delays and shortages due to global lockdowns and restrictions. This disrupted production schedules and increased costs.

- The Russia-Ukraine crisis significantly influenced Canada’s Plastics market. Both Ukraine and Russia are major suppliers of raw materials such as crude oil derivatives, used in the manufacturing of plastics. Higher energy costs and supply chain interruptions brought on by the conflict have raised costs for Canadian plastics manufacturers.

Key Takeaways

Thermoplastics Dominated the Market

The thermoplastics segment dominates the Canada Plastics Market, driven by usage in automotive and aerospace sectors due to their lightweight nature, which supports fuel efficiency and emission reduction goals. In May 2024, the governments of Canada and Québec are providing a total of $2,895,150 to Exxel Polymers, located in Bromont in the Estrie region. This support will enable the business to acquire equipment to increase its productivity and production capacity in order to sustain its growth. The aim of this investment project, valued at over $4 million, is to enable Exxel Polymers Inc., a business specializing in the formulation and production of 100% recycled plastics, to meet the demand and pursue its growth and efforts to export. Additionally, the usage of thermoplastics like polyethylene terephthalate (PET) is growing in Canada's packaging sector, particularly for food and beverage applications. These materials are renowned for their transparency and durability, which are essential for both product safety and customer appeal. Such factors are propelling the growth of thermoplastics in Canada Plastic Market.

Film Extrusion the Largest Segment

Film extrusion is largest segment in the Canada Plastics Market, in terms of process. Canada's strong food and beverage industry, coupled with increasing consumer preference for convenient packaging, has driven demand for flexible packaging materials like polyethylene and polypropylene films. As per Statistics Canada, FCC Economics’ Food and Beverage Report, sales increased 1.5% for food manufacturing in H1 2024. In the first half of 2024, food manufacturing sales were up across several food product categories including bakery and tortilla products, dairy, fruit and vegetable preserving and specialty food, meat products, seafood preparation, and notably, sugar and confectionery. As consumer demand for packaged food and beverages continues to rise, so does the need for reliable and efficient packaging solutions.

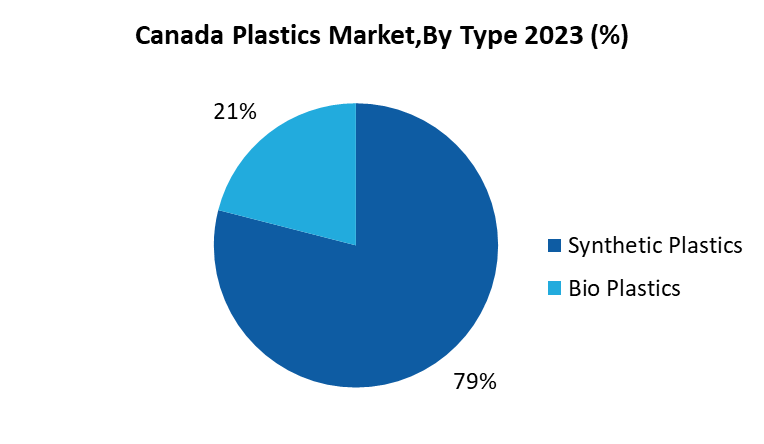

Synthetic Plastics are the Largest Segment

Synthetic Plastics represent the largest segment in the Canada Plastics Market, in terms of type due to its versatile applications. Synthetic plastics offer a wide range of properties, making them suitable for numerous applications across various industries. For instance, In October 2024, Lane Enterprises LLC expanded its operations in Western Canada by opening a new plastic pipe production facility in Longview, Washington. This 38-acre site, with 19 acres in active use serves as a manufacturing hub and distribution yard for the company’s drainage products, including corrugated HDPE pipes, steel pipes, and stormwater chambers. It also houses the regional sales and engineering support teams. Currently, the facility operates two production lines for corrugated HDPE pipes ranging from 4 to 60 inches in diameter and plans to add a third line. Lane uses both recycled and virgin HDPE and aims to include polypropylene pipe manufacturing in the future. Such factors are propelling the growth of plastics market in Canada.

Rise in Demand for Bio-based and Biodegradable Plastics Boosts the Market

The rise in demand for bio-based and bio-degradable plastics is driving the growth of plastics market in Canada. Initiatives to increase recycling rates and adopt circular economy practices support innovation in recyclable plastic materials which in turn driving the plastics market growth in Canada. For instance, in February 2024, Canada’s government invested $1 million in compostable bioplastics through the Jobs and Growth Fund program. This financial assistance has been granted to SME BOSK Bioproducts under the Canada Economic Development for the Quebec Regions (CED) initiative. BOSK Bioproducts specializes in producing bioplastics by collecting industrial waste, such as bio-sludge from paper manufacturing, and transforming it into compostable alternatives. This 100% compostable solution aims to significantly reduce plastic waste in the environment. The funding will focus on the cost of acquiring equipment and installing, testing, and commissioning the unit. The new manufacturing unit will allow BOSK Bioplastics to enhance its production capacity and secure its supply chain. The company can now produce polyhydroxyalkanoate, a key component of REGEN, a bio-based bioplastics material developed for the Canadian market. Such initiatives towards the bio-based plastics are propelling the growth of plastic industry in Canada.

Stringent Regulations on Plastic Pollution

One of the key challenges in the Canada Plastics market is stringent regulations on plastic pollution. Canada’s government is imposing stricter regulations on plastic production, use, and disposal to address environmental concerns like plastic pollution. This includes bans on single-use plastics, extended producer responsibility programs, and recycling targets. For instance, The Government of Canada is implementing a comprehensive plan to reduce plastic pollution, improve how plastic is made, used, and managed across its life cycle, and move toward a circular economy. On April 22, 2024, the Government of Canada published an information-gathering notice under section 46 of the Canadian Environmental Protection Act, 1999 (CEPA) to collect data for the Federal Plastics Registry. A section 46 information-gathering notice is authorized under CEPA to allow the Minister to collect data for the purpose of conducting research, creating an inventory of data, formulating objectives and codes of practice, issuing guidelines or assessing or reporting on the state of the environment. The implementation of stricter regulations and the requirement to report data to the Federal Plastics Registry will increase compliance costs for plastics manufacturers.

For more details on this report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Canada Plastics Market. The top 10 companies in the Canada Plastics Market are:

- Amcor Plc

- NOVA Chemicals Corp

- Winpak Ltd.

- Dow Chemicals Canada Ltd.

- DuPont Canada

- Sonoco Products Company

- Mondi

- Merlin Plastics

- Transcontinental Inc.

- SABIC

Scope of Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

3.3% |

|

Market Size in 2030 |

$35.2 Billion |

|

Segments Covered |

By Polymer Type, By Process, By Type, By End-Use Industry |

|

Key Market Players |

|

For more Chemicals and Materials Market reports, please click here

The Canada Plastics Market is forecast to grow at 3.3% during the forecast period 2024-2030

The Canada Plastics Market size is projected to reach US $35.2 Billion by 2030

The leading players are Amcor Plc, Winpak Ltd., Dow Chemicals Canada Ltd., DuPont Canada, Sonoco Products Company, Mondi and Others.

Demand for recycled plastic materials and incorporating plastics in vehicles are some of the major trends in the market.

The growing usage of plastics in several industries, growing demand for biodegradable, bio-based plastics & high-performance plastics, technological advancements such as development of nanocomposites and hybrid materials and sustainable manufacturing processes are driving the Canada Plastics market growth.