Email

Email Print

Print

3D Semiconductor Packaging Market – By Packaging Method, By Material, By Device Type, By Type, By Application, By Geography - Opportunity Analysis & Industry Forecast, 2024-2030

3D Semiconductor Packaging Market Overview:

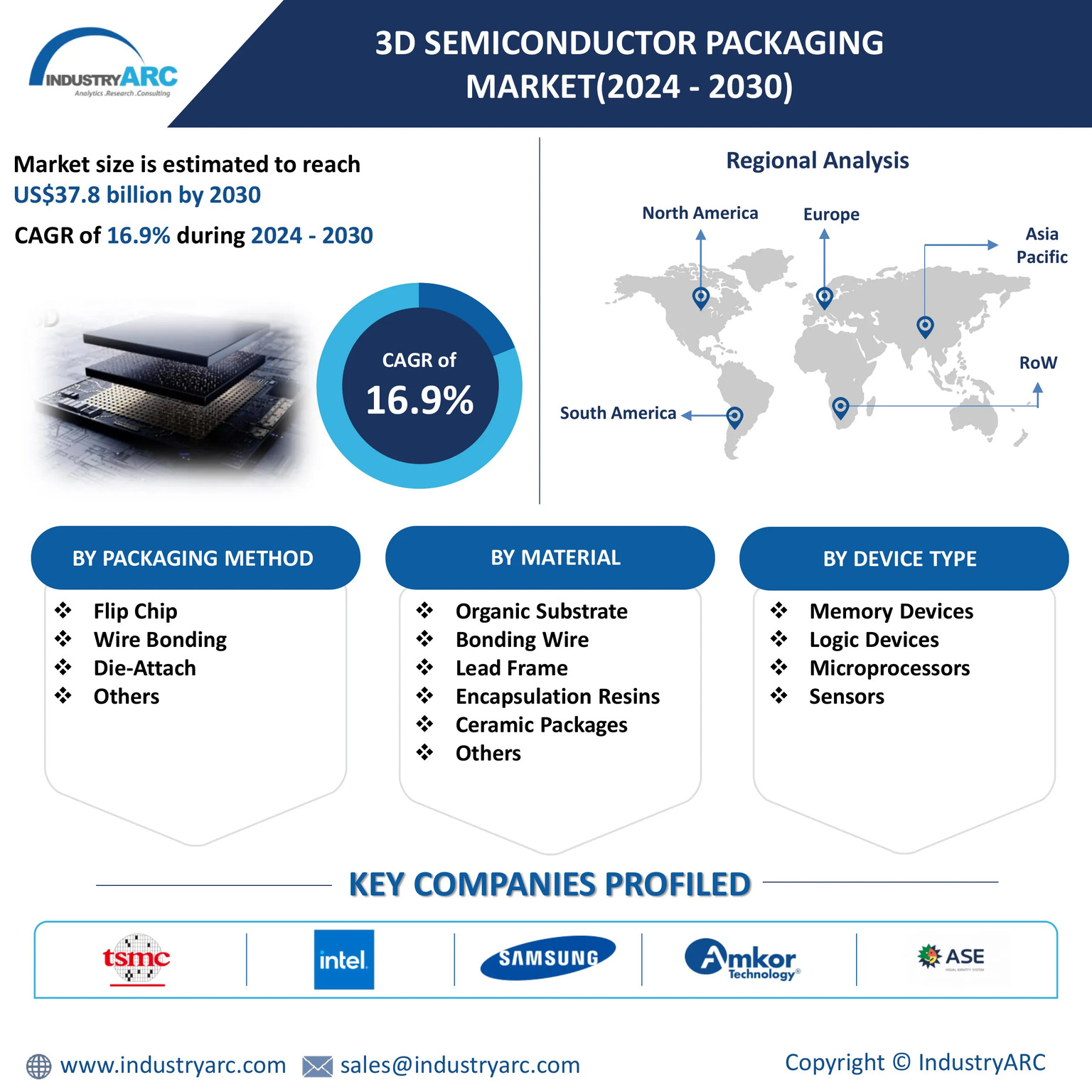

3D Semiconductor Packaging market size is forecast to reach US$37.8 billion by 2030, after growing at a CAGR of 16.9% during 2024-2030. 3D semiconductor packaging involves stacking and interconnecting multiple layers of chips to create more compact, powerful, and efficient electronic devices. The growing demand for miniaturized electronics such as smartphones and wearables are a key driver of this market. Additionally, the rising number of IoT devices has increased the need for high-performance, high-density chips. Automotive electronics and the expansion of data centers also contribute to market growth as they require advanced packaging solutions for better power efficiency and thermal management.

The growth of AI and machine learning coupled with the deployment of 5G are pivotal trends driving the 3D Semiconductor Packaging Market. According to Forbes Advisory, 64% of business owners believe AI will enhance customer relationships and productivity, while 60% expect AI to boost sales growth. These advancements demand higher processing power and efficiency, which 3D packaging can deliver. Additionally, according to a survey by Ericsson, a Swedish multinational networking and telecommunications company, 5G is set to dominate mobile technology, with global subscriptions forecasted to reach 5.6 billion by 2029 accounting for 60% of all mobile subscriptions. The need for faster data processing and lower latency in 5G networks further fuels the demand for advanced 3D semiconductor packaging solutions. Another significant trend is the rise of System-in-Package (SiP) technology which integrates multiple chips within a single package allowing for compact design and improved performance making it ideal for 5G devices and AI applications that require high bandwidth and low power consumption.

Market Snapshot:

3D Semiconductor Packaging Market - Report Coverage:

The “3D Semiconductor Packaging Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the 3D Semiconductor Packaging Market.

| Attribute | Segment |

|---|---|

|

By Packaging Method

|

· Flip Chip · Wire Bonding · Die-Attach · Others |

|

By Material |

· Organic Substrate · Bonding Wire · Lead Frame · Encapsulation Resins · Ceramic Packages · Others |

|

By Device Type |

· Memory Devices · Logic Devices · Microprocessors · Sensors |

|

By Type |

· Through-Silicon Via (TSV) · Package on Package (PoP) · Fan-Out Wafer Level Packaging (FOWLP) · 3D Wafer-Level Chip-Scale Packaging (3D WLCSP) · 3D System-on-Chip (SoC) |

|

By Application |

· Consumer Electronics · Automotive · Industrial · Healthcare · IT & Telecommunications · Aerospace & Defense · Others |

|

By Geography |

· North America (U.S., Canada and Mexico) · Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), · Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), · South America (Brazil, Argentina, Chile, Colombia and Rest of South America) · Rest of the World (Middle East and Africa). |

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic disrupted the 3D semiconductor packaging market, particularly by delaying the development of advanced packaging solutions like Through-Silicon Via (TSV) and fan-out wafer-level packaging. With semiconductor fabs facing temporary closures, there was a sharp decline in production capacity, delaying key projects in sectors like consumer electronics and automotive. However, the rising demand for AI-driven devices during remote work periods accelerated investments in 3D packaging innovations.

- The Russia-Ukraine war affected the 3D semiconductor packaging market by causing a shortage of crucial raw materials like neon and palladium, essential for semiconductor production. Ukraine, a major supplier of high-purity neon used in lithography, saw its export channels disrupted, directly impacting the production timelines for 3D integrated circuits. This geopolitical tension forced semiconductor manufacturers to seek alternative sources and pushed costs higher, further complicating the market's growth trajectory.

Key Takeaways:

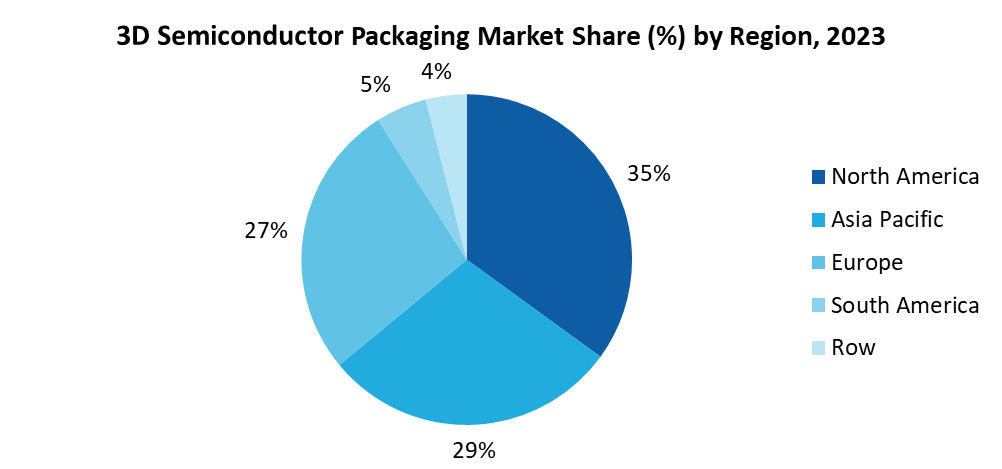

North America is the Leading Region

North America is the largest region for the 3D Semiconductor Packaging Market, driven by the dominance of U.S.-based semiconductor companies in the global industry. According to the Semiconductor Industry Association (SIA), U.S. semiconductor firms hold a commanding 50.2% share of the global market. This dominance is reflected in the significant revenue growth of U.S. semiconductor companies which surged from $71.1 billion in 2001 to $264.6 billion in 2023. The region's leadership in advanced semiconductor technologies and its strong presence in key industries such as artificial intelligence, automotive and telecommunications are crucial factors supporting the adoption of 3D packaging solutions. Additionally, the U.S. is home to some of the world’s largest tech companies and research institutions driving innovation in semiconductor design and packaging. These factors combined with increasing investments in 5G infrastructure and AI development position North America as a key market for 3D semiconductor packaging.

Through-Silicon Via (TSV) is the Largest Segment

The most common type of packaging in the 3D Semiconductor Packaging Market is Through-Silicon Via (TSV) technology. Thermo Fisher Scientific, a global leader in scientific research services and solutions, highlights the complexity of 3D packaging, which involves multiple steps like wafer fabrication, thinning, and bonding. TSV technology has become essential in connecting multiple dies and wafers stacked on top of each other, enabling significant performance gains without relying on traditional wire-bond assembly. The advantages of TSVs include a smaller layout space, higher signal performance, and reduced power consumption. Modern semiconductor packaging structures now incorporate thousands of TSVs to connect multiple chips, such as in High Bandwidth Memory (HBM) technology. For instance, the HBM2 utilizes 60,000 TSVs to achieve the heterogeneous integration of 12 stacked memory chips illustrating the critical role TSV plays in advancing 3D semiconductor packaging.

Consumer Electronics Leads the Market

The largest segment in the 3D Semiconductor Packaging Market by application is Consumer Electronics and this is strongly supported by data from the International Trade Administration (ITA). In 2023, the total revenue from Consumer Electronics reached $768.7 billion accounting for about 21.1% of the total global eCommerce revenue of $3,640.2 billion. This makes Consumer Electronics the second-largest segment in eCommerce after Fashion. The substantial share of Consumer Electronics in global sales highlights the significant demand for advanced electronic devices such as smartphones, tablets and wearables, which are increasingly integral to consumers' daily lives. To meet this demand, manufacturers rely on sophisticated semiconductor technologies like 3D semiconductor packaging which enables the production of compact, high-performance and energy-efficient devices. As the demand for cutting-edge consumer electronics continues to rise, this segment remains the largest in the 3D Semiconductor Packaging Market driving innovation and investment in advanced packaging solutions to support the evolving needs of the consumer electronics industry.

Increasing Demand for Miniaturized Electronic Devices to Drive the Market Growth

The increasing demand for miniaturized electronic devices is a significant driver in the 3D Semiconductor Packaging Market due to the growing consumer preference for smaller and more powerful gadgets. According to the United Nations Conference on Trade and Development (UNCTAD), annual smartphone shipments reached 1.2 billion in 2023. This surge highlights the need for compact, high-performance semiconductor solutions. Moreover, the Internet of Things (IoT) is expected to grow quickly with the number of connected devices projected to increase 2.5 times from 2023, reaching 39 billion by 2029. As these devices become more prevalent the demand for advanced packaging technologies that enable the integration of more functionality into smaller footprints intensifies. 3D semiconductor packaging offers the perfect solution by allowing multiple layers of chips to be stacked vertically improving performance and reducing space making it essential for meeting the evolving requirements of miniaturized electronic devices.

Growing Electronic Waste to Hamper the Growth

The growing issue of electronic waste (e-waste) presents a significant challenge in the 3D Semiconductor Packaging Market as the increasing demand for advanced electronics leads to higher production and, consequently more waste. According to the United Nations Conference on Trade and Development (UNCTAD), digital waste is growing faster than collection rates, with waste from screens and small IT equipment rising by 30% between 2010 and 2022 reaching 10.5 million tons. This surge in e-waste driven by the rapid turnover of electronic devices including those using 3D semiconductor packaging creates serious environmental and health hazards when improperly disposed of. Toxic substances like lead, mercury and cadmium can leach into the soil and water causing long-term ecological damage and posing significant health risks. As 3D packaging technology advances and becomes more widespread the industry faces the challenge of managing the lifecycle of its products responsibly.

For more details on this report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the 3D Semiconductor Packaging Market. The top 10 companies in this industry are listed below:

- TSMC

- Intel Corporation

- Samsung Electronics

- Amkor Technology

- ASE Group

- Texas Instruments

- STMicroelectronics

- Broadcom

- IBM

- SK Hynix

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

16.9% |

|

Market Size in 2030 |

$37.8 Billion |

|

Segments Covered |

By Packaging Method, By Material, By Device Type, By Type, By Application and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

1. TSMC 5. ASE Group 8. Broadcom 9. IBM 10. SK Hynix |

For more Electronics Market reports, please click here

The 3D Semiconductor Packaging Market is projected to grow at 16.9% CAGR during the forecast period 2024-2030.

The 3D Semiconductor Packaging Market size is estimated to be $12.7 billion in 2023 and is projected to reach $37.8 billion by 2030

The leading players in the 3D Semiconductor Packaging Market are TSMC, Intel Corporation, Samsung Electronics, Amkor Technology, ASE Group and Others.

Growth of AI and ML and ise of System-in-Package (SiP) are some of the major 3D Semiconductor Packaging Market trends in the industry which will create growth opportunities for the market during the forecast period.

Rise in the number of IoT devices, growing demand for automotive electronics and increased data center and cloud computing demand are the driving factors of the 3D Semiconductor Packaging market.