Email

Email Print

Print

Aircraft Engine Nacelle Market - By Engine Type , By Material , By Product , By Application , By End-User and By Geography - Opportunity Analysis & Industry Forecast, 2024-2030”.

Aircraft Engine Nacelle Market Overview:

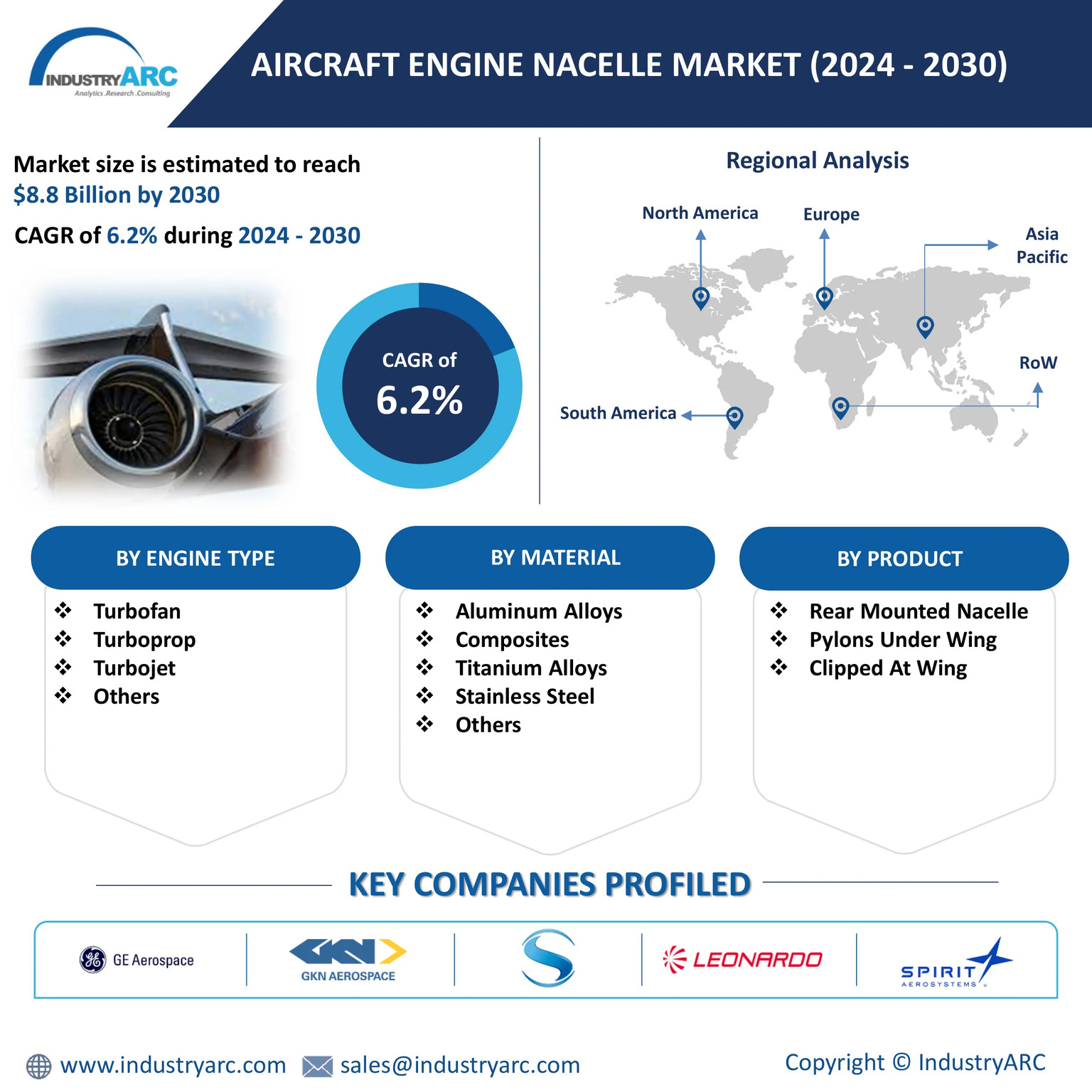

The Aircraft Engine Nacelle Market size is estimated to reach $8.8 Billion by 2030, growing at a CAGR of 6.2% during the forecast period 2024-2030. Nacelles are essential components of aircraft engines that provide protection, streamline airflow and house critical systems. The market growth is driven by the increasing demand for fuel-efficient and quieter engines, the growing air passenger traffic, and the continuous development of advanced materials and technologies. As the aviation industry experiences steady growth, the demand for innovative nacelle solutions is expected to rise, further propelling market expansion. Advancements in engine technology and the growing need for aftermarket services further contribute to the growth of aircraft engine nacelle market.

The market for aircraft engine nacelle is changing because of the increased demand for lighter aircraft, lower emissions, and fuel economy, which is driving the usage of innovative materials. New materials that are lighter, more durable, and support better thermal and acoustic management are advantageous for nacelles, which house the engine and act as an aerodynamic contact between the engine and wing. Tenax prepreg, a specialized material designed for aircraft applications, incorporates a high-performance, rapid-curing epoxy resin system. This advanced prepreg formulation allows for efficient processing at reduced temperatures and cycle times, providing significant advantages over conventional aerospace prepregs. Another trend is additive manufacturing or 3D printing. This innovative technology offers unparalleled design freedom and manufacturing flexibility, enabling the creation of complex, lightweight, and high-performance components that were previously unattainable with traditional manufacturing methods.

Market Snapshot:

Aircraft Engine Nacelle Market - Report Coverage:

The “Aircraft Engine Nacelle Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Aircraft Engine Nacelle Market.

| Attribute | Segment |

|---|---|

|

By Engine Type |

|

|

By Material |

|

|

|

|

By Application

|

|

|

By End-User

|

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic had a profound impact on the global aviation industry, significantly affecting the aircraft engine nacelle market. The sudden decline in air travel resulted in a sharp reduction in demand for new aircraft, maintenance, repair, and overhaul (MRO) services, and spare parts. Flights being grounded reduced airline demand forced manufacturers to delay deliveries of new aircraft and reduce production rates, consequently impacting the demand for new engine nacelles.

- The Russia-Ukraine war had a profound impact on the global aviation industry, particularly affecting the aircraft engine nacelle market. Russia, a major supplier of titanium, a crucial material for nacelle manufacturing, has seen disrupted supply chains, leading to potential shortages and increased costs. The conflict has also disrupted the supply of other critical raw materials like nickel and aluminium, further impacting nacelle production.

Key Takeaways:

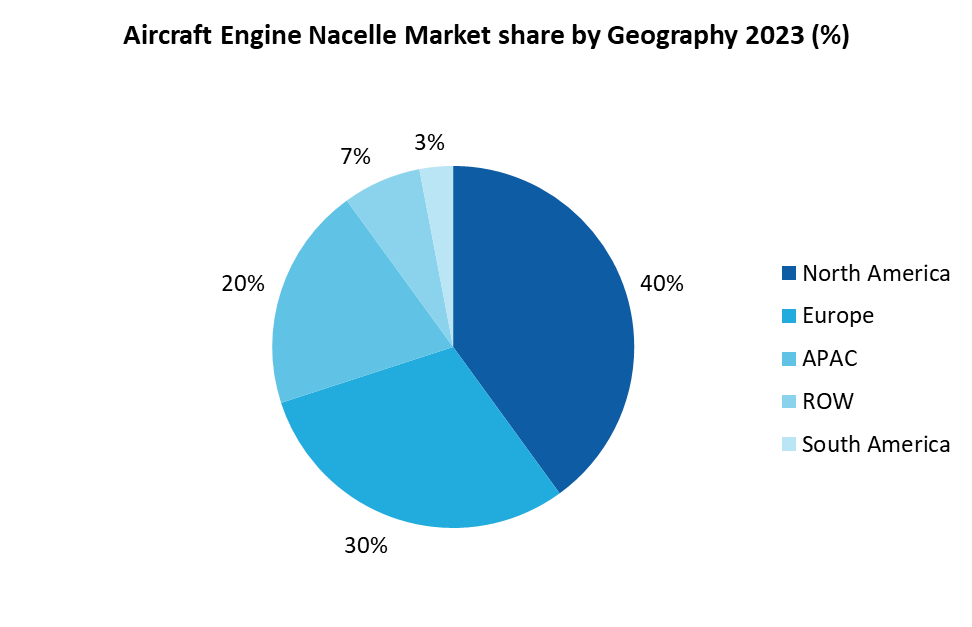

North America Leads the Market

North America dominates in the aircraft engine nacelle market with a market share of 40%. North America, particularly the United States, is home to major aerospace companies like Boeing and key nacelle manufacturers such as RTX. These companies have substantial engineering expertise and manufacturing capabilities that position North America as a central hub for nacelle production. Additionally, stringent safety standards set by the Federal Aviation Administration (FAA) and other regulatory bodies investment from government boost the aviation industry. 14 CFR Part 33 outlines the FAA's airworthiness standards for aircraft engines including the design, construction and performance. This regulation ensures the safety and reliability of aircraft engines and their components such as engine nacelles. Safety standards for aircraft nacelles are crucial, as nacelles house the engine and play a vital role in protecting it from external elements. Therefore, these factors collectively make North America as the dominant region in the aircraft engine nacelle market, ensuring it remains a global leader in advanced nacelle technology and production.

Turbofan engine type dominates the market.

The turbofan engine type dominates the aircraft engine nacelle market, primarily due to its widespread use in commercial aviation, where high passenger and cargo demand necessitates efficient, quieter, and fuel-effective propulsion systems. These engines are the preferred choice for most commercial aircraft, from single-aisle models like the Airbus A320 and Boeing 737 to wide-body aircraft such as the Boeing 777 and Airbus A350. This is due to the high bypass ratios of turbofans, which provide efficient thrust and better fuel economy. High-bypass turbofan engines inherently produce less noise compared to other engines due to their design, which incorporates large fans that move air efficiently while reducing noise levels. Nacelles for these engines are equipped with advanced acoustic liners to further decrease noise emissions. Therefore, majority of the global passenger and cargo fleet uses turbofan engines, creating substantial demand for compatible nacelles that enhance aerodynamics and noise reduction.

Composite materials dominate the market

Composites have revolutionized the aviation industry, offering a unique combination of strength, durability and lightweight properties. Composite materials used in aviation are typically made of a combination of different materials primarily reinforcing fibers such as carbon fiber, fiberglass, or aramid fibers and a matrix material such as epoxy resin. These materials are combined to create composites that offer superior strength-to-weight ratios compared to traditional materials like aluminium or steel. One of the most significant advantages of composites in aviation is their exceptional strength-to-weight ratio. Composites allow designers to achieve the same level of strength with significantly less weight, contributing to improved fuel efficiency and overall performance. The Boeing 787 is a shining example of composite innovation. Approximately 50% of the Dreamliner’s structural weight is made up of composites, contributing to its fuel efficiency and long-haul capabilities. Therefore, these materials are best suited for meeting the aviation industry's increasing demands for efficiency, sustainability and cost-effectiveness positioning them as the preferred choice over alloys, titanium, and other emerging materials.

Fuel-Efficient Nacelles drives the market

The demand for fuel efficiency is a key driver in the aircraft engine nacelle market, driven by rising fuel costs and the aviation industry’s commitment to sustainability. According to Investopedia, fuel costs account for about 22% of operating expenses. As of 2023, Jet A-1 fuel costs about $3.86 per gallon ($1.40 per liter). This equals to between $5 to $20 per mile, and anywhere between $500 to $2,000 per hour. The use of composite materials like carbon fiber-reinforced polymer (CFRP) in nacelles not only reduces weight but also contributes to sustainability by lowering the embodied energy and emissions involved in aircraft production and maintenance. These nacelles, lighter and more durable than traditional materials, reduce fuel consumption over the aircraft's lifespan, enhancing both operational efficiency and emissions reduction. Airbus A350 XWB also utilizes composite materials extensively making it a fuel-efficient and environmentally friendly option. Therefore, driven by the need to reduce operational costs and meet environmental regulations, the aircraft engine nacelle market is prioritizing fuel efficiency and emissions reduction.

Stringent Regulatory Standards

Stringent regulatory standards are a significant challenge for the aircraft engine nacelle market, driven by international and regional policies that enforce strict requirements on noise reduction, emissions control, and environmental sustainability. According to The European Green Deal, The European Commission has adopted a set of proposals to make the EU's climate, energy, transport and taxation policies fit for reducing net greenhouse gas emissions by at least 55% by 2030. Aircraft operating within the EU are subject to stringent environmental policies, and airlines are under pressure to adopt nacelle technologies that minimize emissions. This push toward ultra-efficient nacelles demands continuous R&D and advanced materials, often increasing the overall cost and challenging manufacturers’ ability to maintain profit margins. The requirements for compliance demand continuous innovation, material advancements, and complex design adjustments, which increase costs and complicate production. As the aviation industry aims for greener and quieter skies, nacelle manufacturers must navigate these regulatory pressures to develop high-performance, compliant nacelles without compromising profitability.

For more details on this report - Request for Sample

Key Market Players:

The top 10 companies in this industry are listed below:

- GE Aerospace

- Safran

- Leonardo SpA

- GKN Aerospace Services Limited

- Spirit AeroSystems Inc.

- RTX

- NORDAM Group LLC

- Aernnova Aerospace SA

- Magellan Aerospace Corporation

- FACC AG

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

6.2% |

|

Market Size in 2030 |

$8.8 Billion |

|

Segments Covered |

By Engine Type, By Material, By Product, By Application, By End-User and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Denmark, Netherlands and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Thailand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

For more Automotive Market reports, please click here

LIST OF TABLES

1.Global Aircraft Engine Nacelle MARKET, BY TYPE Market 2023-2030 ($M)

1.1 Rear Mounted Nacelle Market 2023-2030 ($M) - Global Industry Research

1.2 Pylons Under Wing Market 2023-2030 ($M) - Global Industry Research

1.3 Clipped At Wing Market 2023-2030 ($M) - Global Industry Research

2.Global Aircraft Engine Nacelle MARKET, BY TYPE Market 2023-2030 (Volume/Units)

2.1 Rear Mounted Nacelle Market 2023-2030 (Volume/Units) - Global Industry Research

2.2 Pylons Under Wing Market 2023-2030 (Volume/Units) - Global Industry Research

2.3 Clipped At Wing Market 2023-2030 (Volume/Units) - Global Industry Research

3.North America Aircraft Engine Nacelle MARKET, BY TYPE Market 2023-2030 ($M)

3.1 Rear Mounted Nacelle Market 2023-2030 ($M) - Regional Industry Research

3.2 Pylons Under Wing Market 2023-2030 ($M) - Regional Industry Research

3.3 Clipped At Wing Market 2023-2030 ($M) - Regional Industry Research

4.South America Aircraft Engine Nacelle MARKET, BY TYPE Market 2023-2030 ($M)

4.1 Rear Mounted Nacelle Market 2023-2030 ($M) - Regional Industry Research

4.2 Pylons Under Wing Market 2023-2030 ($M) - Regional Industry Research

4.3 Clipped At Wing Market 2023-2030 ($M) - Regional Industry Research

5.Europe Aircraft Engine Nacelle MARKET, BY TYPE Market 2023-2030 ($M)

5.1 Rear Mounted Nacelle Market 2023-2030 ($M) - Regional Industry Research

5.2 Pylons Under Wing Market 2023-2030 ($M) - Regional Industry Research

5.3 Clipped At Wing Market 2023-2030 ($M) - Regional Industry Research

6.APAC Aircraft Engine Nacelle MARKET, BY TYPE Market 2023-2030 ($M)

6.1 Rear Mounted Nacelle Market 2023-2030 ($M) - Regional Industry Research

6.2 Pylons Under Wing Market 2023-2030 ($M) - Regional Industry Research

6.3 Clipped At Wing Market 2023-2030 ($M) - Regional Industry Research

7.MENA Aircraft Engine Nacelle MARKET, BY TYPE Market 2023-2030 ($M)

7.1 Rear Mounted Nacelle Market 2023-2030 ($M) - Regional Industry Research

7.2 Pylons Under Wing Market 2023-2030 ($M) - Regional Industry Research

7.3 Clipped At Wing Market 2023-2030 ($M) - Regional Industry Research

LIST OF FIGURES

1.US Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

2.Canada Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

3.Mexico Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

4.Brazil Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

5.Argentina Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

6.Peru Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

7.Colombia Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

8.Chile Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

9.Rest of South America Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

10.UK Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

11.Germany Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

12.France Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

13.Italy Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

14.Spain Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

15.Rest of Europe Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

16.China Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

17.India Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

18.Japan Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

19.South Korea Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

20.South Africa Aircraft Engine Nacelle Global Market Revenue, 2023-2030 ($M)

21.North America Aircraft Engine Nacelle Global By Application

22.South America Aircraft Engine Nacelle Global By Application

23.Europe Aircraft Engine Nacelle Global By Application

24.APAC Aircraft Engine Nacelle Global By Application

25.MENA Aircraft Engine Nacelle Global By Application

The Aircraft Engine Nacelle Market is projected to grow at 6.2% CAGR during the forecast period 2024-2030.

The Aircraft Engine Nacelle Market size is estimated to be $5.1 billion in 2023 and is projected to reach $8.8 billion by 2030.

The leading players in the Aircraft Engine Nacelle Market are GE Aerospace, Safran, Leonardo SpA, GKN Aerospace Services Limited, Spirit AeroSystems Inc. and others.

The future of the aircraft engine nacelle market will be shaped by use of advanced materials and additive manufacturing in aircraft engine nacelle production.

The aircraft engine nacelle market is driven by increasing demand for fuel efficiency, growth in commercial aviation, stringent noise regulations, advancements in engine technology, and the need for aftermarket services.