Email

Email Print

Print

Cling Film Market – By Material , By Length , By End Use Industry , By Distribution Channel , and By Geography Analysis - Global Opportunity Analysis & Industry Forecast, 2025-2031

Cling Film Market Overview

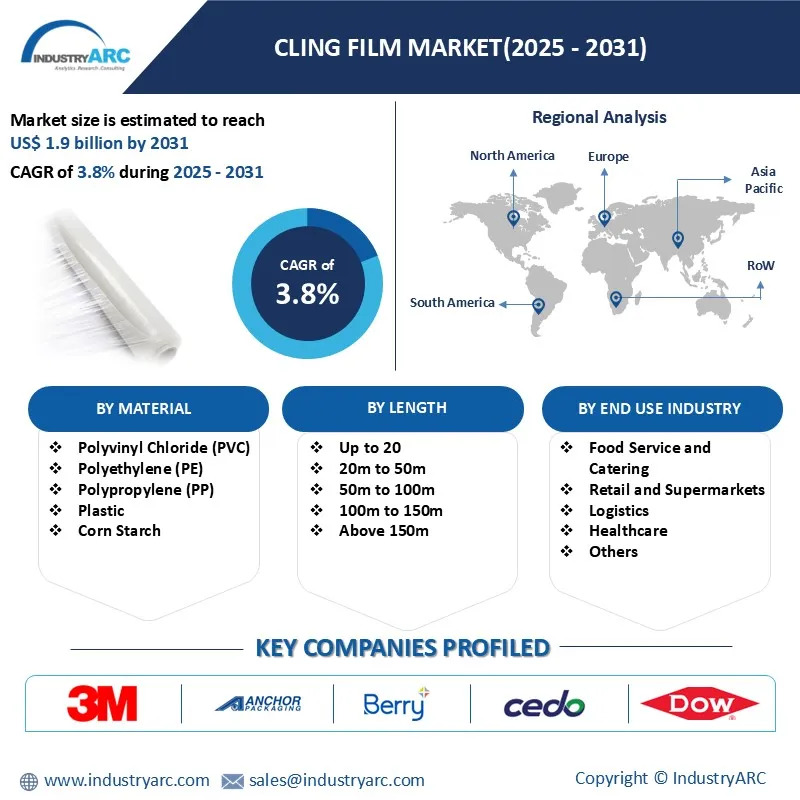

The Cling Film market is estimated to reach US$1.9 billion by 2031, growing at a CAGR of 3.8% from 2025 to 2031. Cling Film, also known as plastic wrap, food wrap, or saran wrap, is a thin, transparent plastic film used to seal and secure food items to keep them fresh. The growth of the food packaging industry, shifting lifestyles that increase the frequent use of Cling Films, advancements in sustainable and biodegradable packaging technologies, rising demand for food storage solutions driven by a growing population, product versatility, and cost efficiency are key drivers of the Cling Film market.

Recent trends in the Cling Film market highlight the increasing demand for customized and specialized Cling Films and the growing preference for convenient food packaging solutions. In January 2024, Berry Global introduced an enhanced version of its Omni Xtra polyethylene Cling Film. Designed for fresh food packaging, this upgraded product is a certified recyclable alternative to traditional PVC films, offering improved resistance, elasticity, strength, and puncture resistance.

Market Snapshot:

Cling Film Market - Report Coverage:

The report: “Cling Film Market – Forecast (2025-2031)”, by IndustryARC, covers an in-depth analysis of the following segments of the Cling Film Industry.

| Attribute | Segment |

|---|---|

|

By Material |

|

|

By Length |

|

|

By End Use Industry |

|

|

By Distribution Channel |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic had a notable effect on the Cling Film market, supply chains and manufacturing operations were disrupted. Lockdowns and restrictions caused raw material shortages, reducing production capabilities and slowing market growth. At the same time, the pandemic increased demand for Cling Film, driven by a heightened focus on hygiene and food safety. This shift also sparked a growing interest in sustainable alternatives like recyclable Cling Films. Despite production challenges, the market saw an increasing demand for innovations that address both convenience and environmental concerns, balancing the need for hygiene with eco-friendly solutions.

- The Russia-Ukraine war has had a notable impact on the Cling Film market, mainly due to disruptions in the supply of raw materials and higher production costs. Ukraine is an important supplier of various plastic materials, and the ongoing conflict has caused shortages of key polymers like polyethylene and PVC, which are essential for Cling Film production. Moreover, escalating energy costs and inflation have added pressure on manufacturing, leading to increased prices for both raw materials and finished products. The war has also introduced significant uncertainty in global supply chains, resulting in delays and logistical challenges that have further strained the market.

Key Takeaways:

-

Rice Starch Cling Film is the Fastest Growing Type in the Cling Film Market

In the Cling Film Market segmented by material, the Rice Starch segment is experiencing the fastest growth with a CAGR of 4.8% in the forecast period of 2025 to 2031. The growth is driven by the rising demand for sustainable, biodegradable packaging solutions. Unlike traditional PVC and polyethylene films, rice starch-based Cling Films are derived from renewable resources, making them a preferred choice among environmentally conscious consumers. Rice starch Cling Films offer comparable elasticity and durability while significantly reducing environmental impact. With stricter regulations on single-use plastics and an increasing shift toward sustainable alternatives, these films are rapidly gaining market share. Advances in production technology are further enhancing their cost-effectiveness and scalability, accelerating their adoption across industries. A 2024 study conducted by Udayana University in Indonesia highlights the pressing issue of conventional plastic waste, emphasizing its lengthy decomposition process. The research advocates for biodegradable bioplastics made from plant-derived materials like starch, cellulose, and lignin. Rice starch Cling Films stand out as a promising alternative, offering an eco-friendly solution to synthetic packaging challenges. Additionally, the Indian Food and Beverage Packaging Industry is experiencing robust growth. According to the All-India Food Processors Association, the industry is expanding at an annual rate of 14.8% and is projected to reach USD 86 billion by 2029. This growth is fuelled by rapid urbanization, rising disposable incomes, and evolving consumption patterns, creating significant opportunities for rice starch-based packaging solutions. As consumers and industries continue to prioritize sustainability, rice starch Cling Film is poised to lead the way in the transition to greener packaging practices.

Food Service and Catering is the Largest End-Use type in the Cling Film Market

The Food Service and Catering segment is experiencing the fastest growth with a CAGR of 4.6% in the forecast period of 2025 to 2031. The food service and catering industry represents the largest end-use segment in the Cling Film market, primarily due to its critical role in food preservation, storage, and packaging. Cling Film is widely used in restaurants, cafeterias, and catering services to maintain freshness and prevent contamination of prepared meals. Its ability to tightly seal food items makes it ideal for short-term storage and transportation, ensuring quality and hygiene. In December 2023, Berry Global introduced an updated version of its Omni Xtra polyethylene Cling Film, designed for fresh food applications. This new Omni® Xtra+ film offers improved elasticity, uniform stretching, and enhanced impact resistance, providing a high-performance alternative to traditional PVC films. While Omni® Xtra has been used for packaging fruit, vegetables, meat, poultry, and deli products, the enhanced version further boosts its versatility. As the food industry increasingly demands convenience and efficiency, Cling Film’s adaptability ensures its continued dominance in food service operations. The increasing popularity of food delivery services and the growing importance of food safety are key factors driving the adoption of Cling Film as a preferred packaging solution.

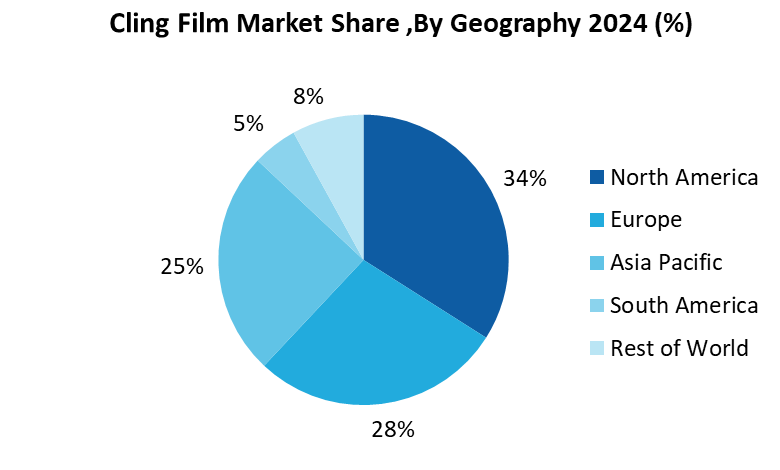

North America is the Largest Geography in the Cling Film Market

North America leads the Cling Film market driven by strong demand for food packaging solutions. The United States plays a key role, supported by the growth of the food service industry, including restaurants, food trucks, and catering services. Cling Film is essential in these sectors for preserving food freshness, maintaining hygiene, and offering convenience. In August 2023, Treplar, a company specializing in eco-friendly food packaging, announced plans to open a new plant in Martinsburg. The facility, equipped with advanced technology and employing over 100 workers (projected to grow to 600 within three years), will produce a new generation of 100% home-compostable food packaging materials. North America's increasing emphasis on sustainability and adopting eco-friendly packaging alternatives, including biodegradable Cling Films, significantly influence market trends. The expanding food delivery sector and growing awareness of food safety further strengthen the region’s position as the largest market for Cling Film.

Rising demand for sustainable and biodegradable solutions drives the Cling Film market

The increasing importance of environmental sustainability is a key factor driving the growth of the Cling Film market, as both consumers and businesses actively seek eco-friendly alternatives to conventional plastic packaging. Biodegradable Cling Films, made from materials like rice starch, plant-based polymers, and compostable bioplastics, are gaining widespread acceptance due to their lower environmental impact. These advancements align with global efforts to reduce plastic waste and adhere to stricter single-use plastic regulations. For example, a July 2023 survey conducted by Pro Carton, the European Association of Carton and Cartonboard Manufacturers, revealed that 63% of over 5,000 consumers across the UK, France, Germany, Spain, and Italy are committed to leading more sustainable lifestyles. Moreover, 58% identified recycling as their top priority in combating climate change. This growing commitment to sustainability underscores the rising demand for innovative and biodegradable packaging solutions, positioning the Cling Film market for significant growth in the years ahead.

Environmental Concerns pose challenges to the growth of the Cling Film market

Environmental concerns are increasingly challenging the Cling Film market as traditional plastics, primarily made from PVC and polyethylene, contribute to widespread plastic waste. Over 460 million metric tons of plastic are produced annually for use in various applications, with an estimated 20 million metric tons of plastic litter ending up in the environment annually. This amount is expected to rise significantly by 2040, exacerbating environmental damage. These issues have led to stricter regulations on single-use plastics and a push for more sustainable packaging solutions. While biodegradable alternatives and recycling initiatives are gaining traction, high production costs, and limited infrastructure remain barriers. As manufacturers seek to balance sustainability with cost-efficiency, addressing these environmental challenges is essential for the long-term growth of the Cling Film market.

For More Details on This Report - Request for Sample

Cling Film Market Key Players

The top 10 players in the Cling Film Market are:

- 3M

- Anchor Packaging LLC

- Berry Global Inc.

- CeDo

- Dow Inc.

- Reynolds Consumer Products

- AEP Industries Inc.

- Jindal Poly Films Ltd.

- Anchor Packaging Inc.

- Intertape Polymer Group Inc.

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2024 |

|

Forecast Period |

2025–2031 |

|

CAGR |

3.8% |

|

Market Size in 2031 |

$1.9 Billion |

|

Segments Covered |

By Material, By Length, By End Use Industry, By Distribution Channel, By Geography |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

1.3M 2. Anchor Packaging LLC 3. Berry Global Inc. 4. CeDo 5. Dow Inc. 6. Reynolds Consumer Products 7. AEP Industries Inc. 8. Jindal Poly Films Ltd. 9. Anchor Packaging Inc. 10. Intertape Polymer Group Inc. |

For more Chemicals and Materials Market reports, please click here

The Cling Film Market is projected to grow at 3.8% CAGR during the forecast period 2025-2031.

The Cling Film Market size is estimated to be $1.5 billion in 2024 and is projected to reach $1.9 billion by 2031.

The leading players in the Cling Film Market are 3M, Anchor Packaging LLC, Berry Global Inc, CeDo, and Dow Inc.

The market is being shaped by key trends such as the growing emphasis on sustainability and eco-friendly materials, the rising demand for food and pharmaceutical packaging, and the expansion into new geographical markets.

The Cling Film market is driven by growing demand for food and pharmaceutical packaging, fuelled by rising ready-to-eat meal consumption and food safety concerns. Advancements in multi-layered and bio-based materials enhance performance and sustainability, while eco-friendly solutions meet regulatory and consumer demands. Emerging markets in Asia-Pacific, Africa, and Latin America present growth opportunities due to urbanization and higher incomes. Specialty films with anti-microbial and shelf-life-extending properties cater to niche needs and innovations in manufacturing and supply chain collaboration to support market expansion.